Future of Claims

The $143 Billion Squeeze: Why Insurance Defense Needs a Strategic Plan for AI

In 2023, U.S. commercial casualty insurance losses hit $143 billion — comfortably exceeding the $108 billion cost of global natural catastrophes that same year [1]. The comparison is not rhetorical decoration. Nature, at least, has the courtesy of being random. What the insurance defense industry faces is something more deliberate: a coordinated, well-capitalized, technologically savvy assault on the economics of defending claims, arriving from both sides of the table simultaneously.

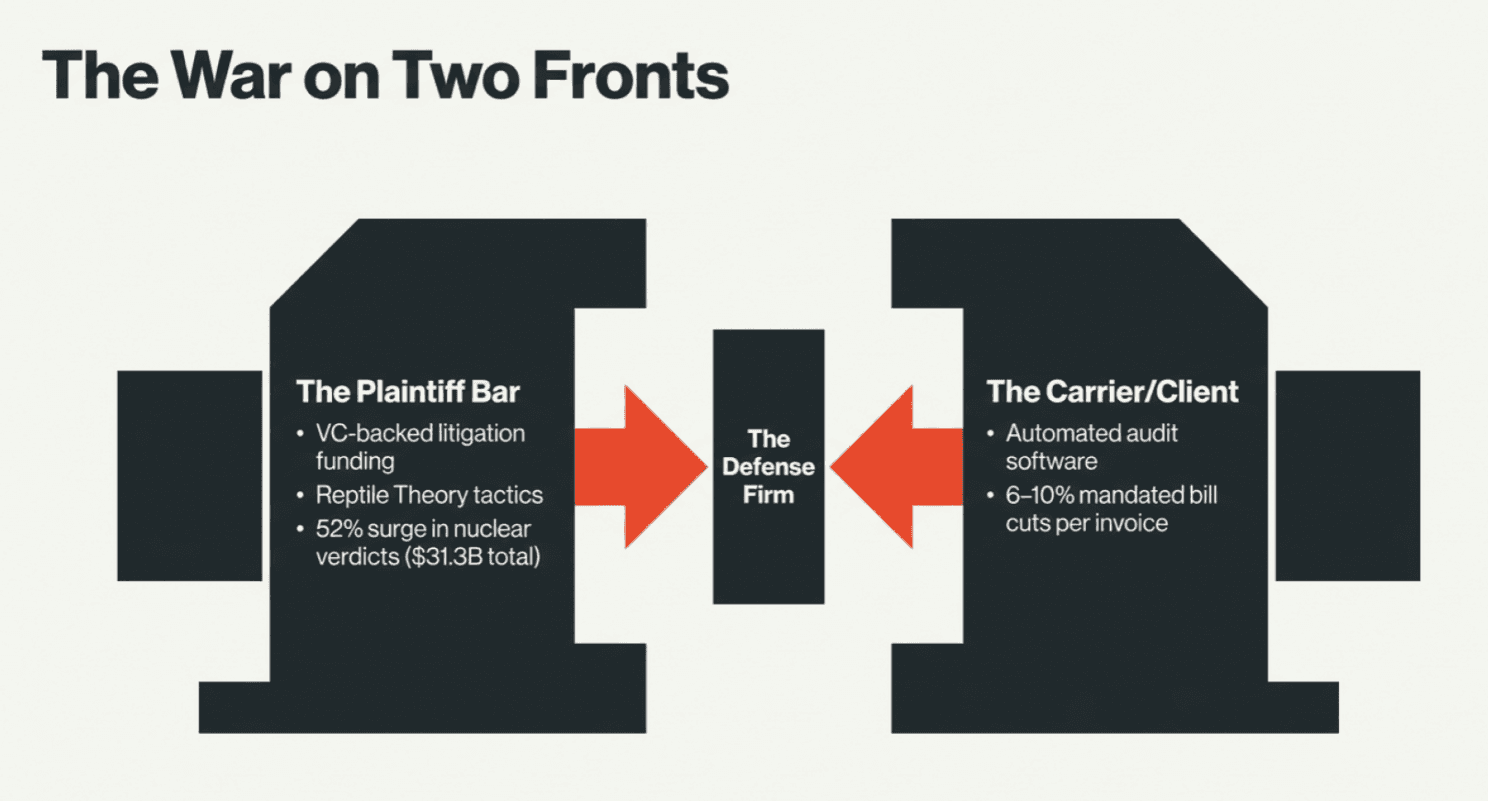

The plaintiff bar has discovered venture capital. Third-party litigation funding has swelled into a global market valued at roughly $20 billion and growing at double-digit rates [2]. Nuclear verdicts — jury awards exceeding $10 million — surged 52% in 2024 to 135 cases, with total payouts reaching a record $31.3 billion [3]. Thermonuclear verdicts above $100 million climbed 81.5% in the same period [4]. Plaintiff firms are deploying reptile theory, jury psychology, aggressive advertising (over $2 billion spent in 2023 alone), and increasingly sophisticated AI tools to drive up the cost of every contested claim [5].

Meanwhile, on the other side of the table, the very clients who need better defense are making it harder to deliver. Insurance carriers have built a half-billion-dollar legal bill review industry, deploying automated audit software and armies of attorney-auditors to scrutinize and cut defense bills by 6% to 10% per invoice [6]. The message is unmistakable: do more with less, or we’ll find someone who will.

Caught in this vice — between adversaries who are spending more and clients who are paying less — insurance defense firms face an existential question that no amount of billable-hour optimization can answer. The answer, such as it is, lies not in working harder but in redesigning how defense work gets done. AI provides the tools. What’s been missing is the plan.

Sadly the toughest battles are often fought against your own side

The War on Two Fronts

The numbers tell a story of acceleration. Between 2013 and 2022, the U.S. Chamber of Commerce’s Institute for Legal Reform documented 1,288 nuclear verdicts, with the median product liability nuclear verdict rising from $24 million to $36 million — a 50% increase [7]. The median nuclear verdict across all categories doubled from $21 million in 2020 to $44 million by 2023 [8]. And in 2024, the Marathon Strategies report found five verdicts exceeding $1 billion each [3].

Behind these figures stands a plaintiff ecosystem that has professionalized at every level. Litigation funders — hedge funds with portfolio theories of litigation and the patience of pension funds — are bankrolling cases that solo practitioners working on contingency from strip-mall offices once pursued alone. The Casualty Actuarial Society and the Insurance Information Institute estimate that legal system abuse added between $231.6 billion and $281.2 billion to liability insurance losses over the decade ending in 2024 [9]. This is not a blip. It is a structural shift in the economics of claiming.

Better money and less work is hard to resist over the long term

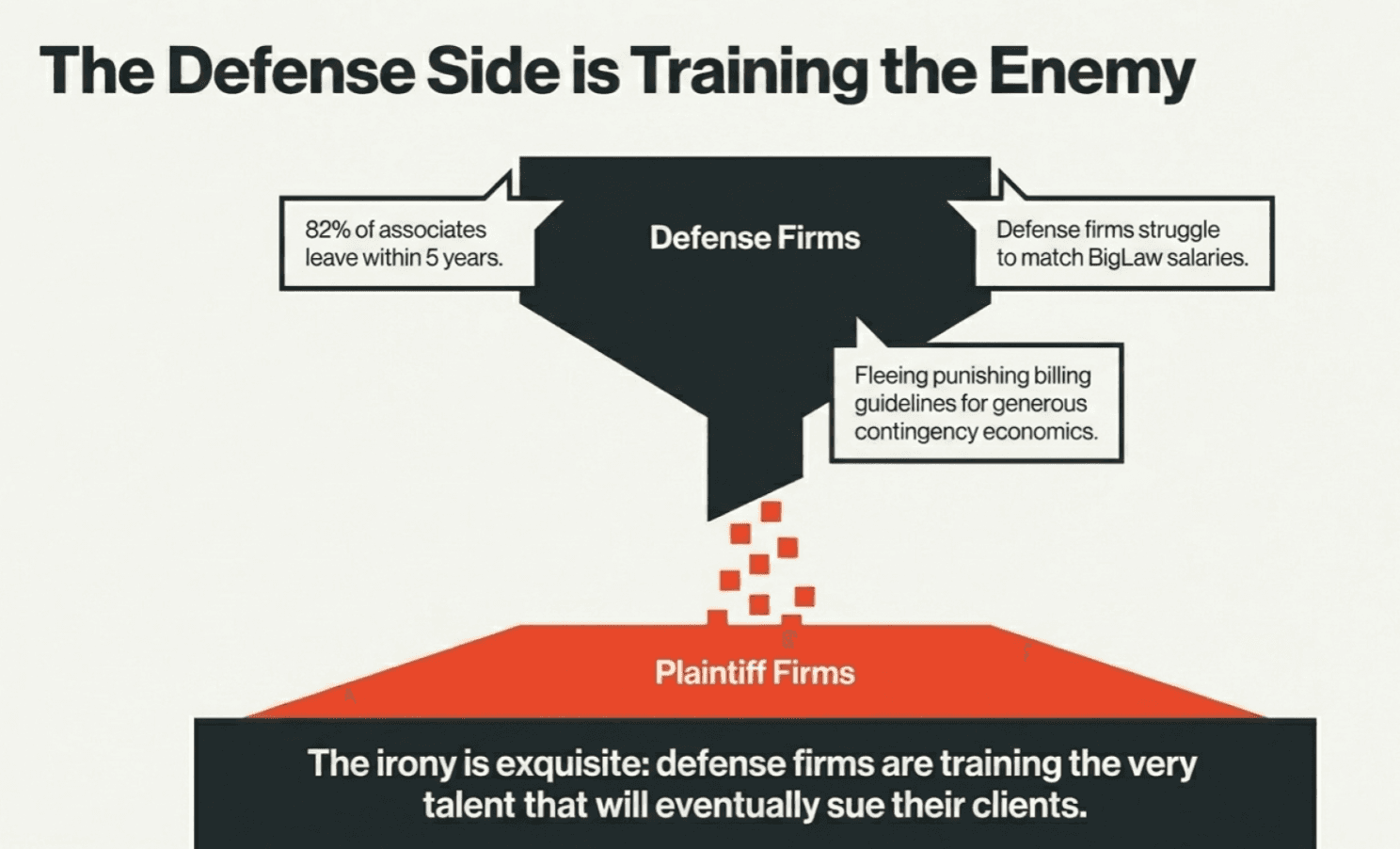

Defense firms, meanwhile, are bleeding talent. Insurance defense has long struggled to compete with BigLaw salaries, and the gap is widening. Midlevel associates — the engine room of any litigation practice — are the hardest to recruit and retain [10]. The NALP Foundation reports that 82% of associates who left their firms in 2023 did so within five years of hiring, departing roughly a year earlier than historical norms [11]. Many migrate to plaintiff firms, where the economics are more generous and the billing guidelines less punishing. The irony is exquisite: the defense side is training the people who will eventually sue its clients.

(One might call it an unfair fight, except that fairness was never quite the point.)

Robots plus humans beat either operating alone

Humans and Machines: A Symbiotic Intelligence

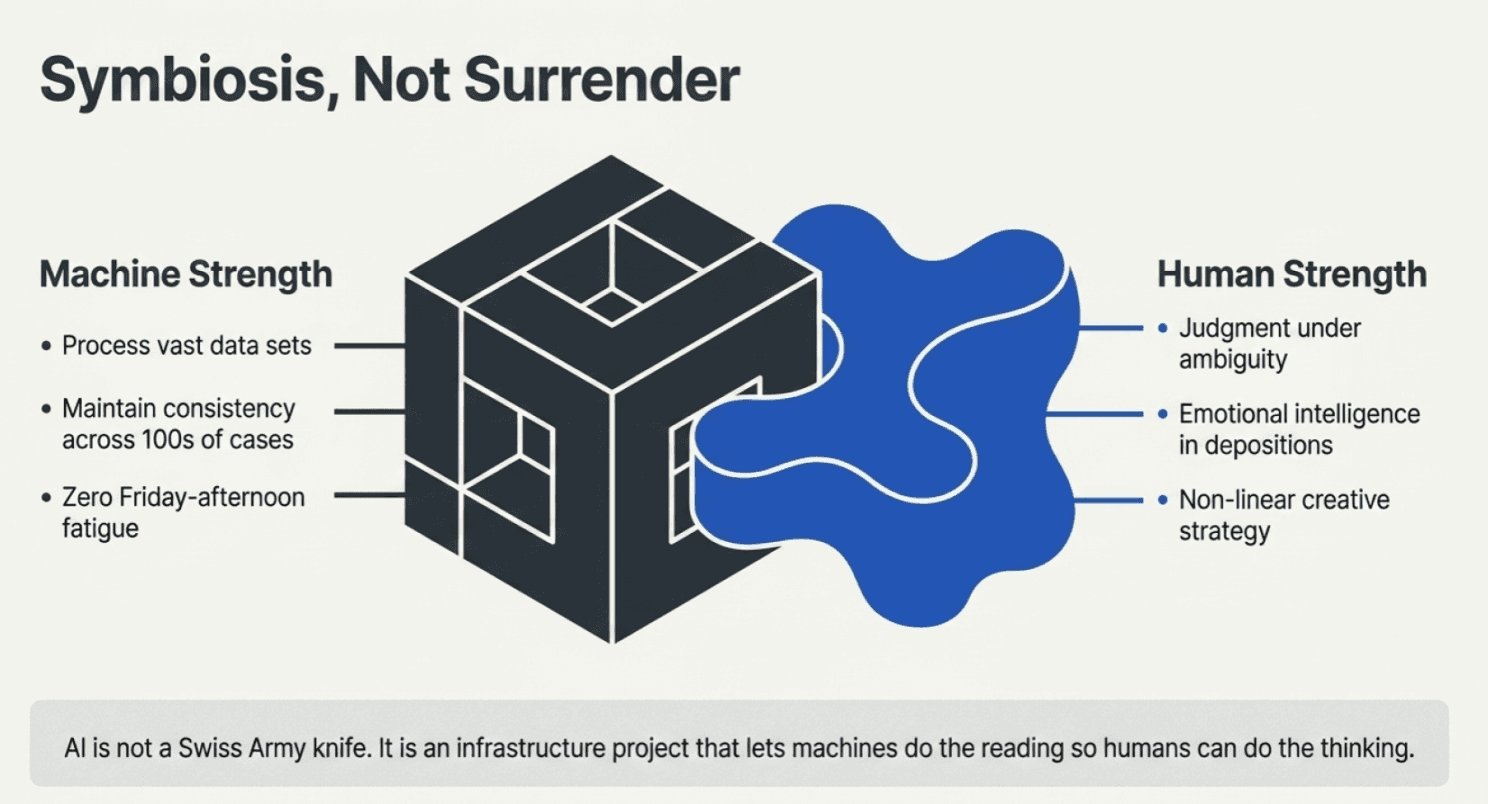

The instinct, when faced with existential pressure, is to reach for the nearest tool and start swinging. But AI in insurance defense is not a Swiss Army knife you pull from a drawer. It is an infrastructure project that requires rethinking the relationship between human judgment and machine capability.

The distinction matters. AI is exceptionally good at certain things: processing vast quantities of data at speed, maintaining consistency across hundreds of cases, identifying patterns in historical outcomes, and performing repetitive analytical tasks without fatigue or Friday-afternoon decline. Humans remain indispensable for different reasons: judgment under ambiguity, emotional intelligence in depositions and mediations, non-linear creative thinking, and the relationship capital that keeps clients loyal and juries attentive.

The strategic plan for AI in insurance defense is not about replacing one with the other. It is about designing workflows where each does what it does best, in sequence, so the whole is considerably greater than the sum of the parts. What follows are the key elements of that redesign.

Pick your battles is often the best strategy

Triage Early, Triage Often

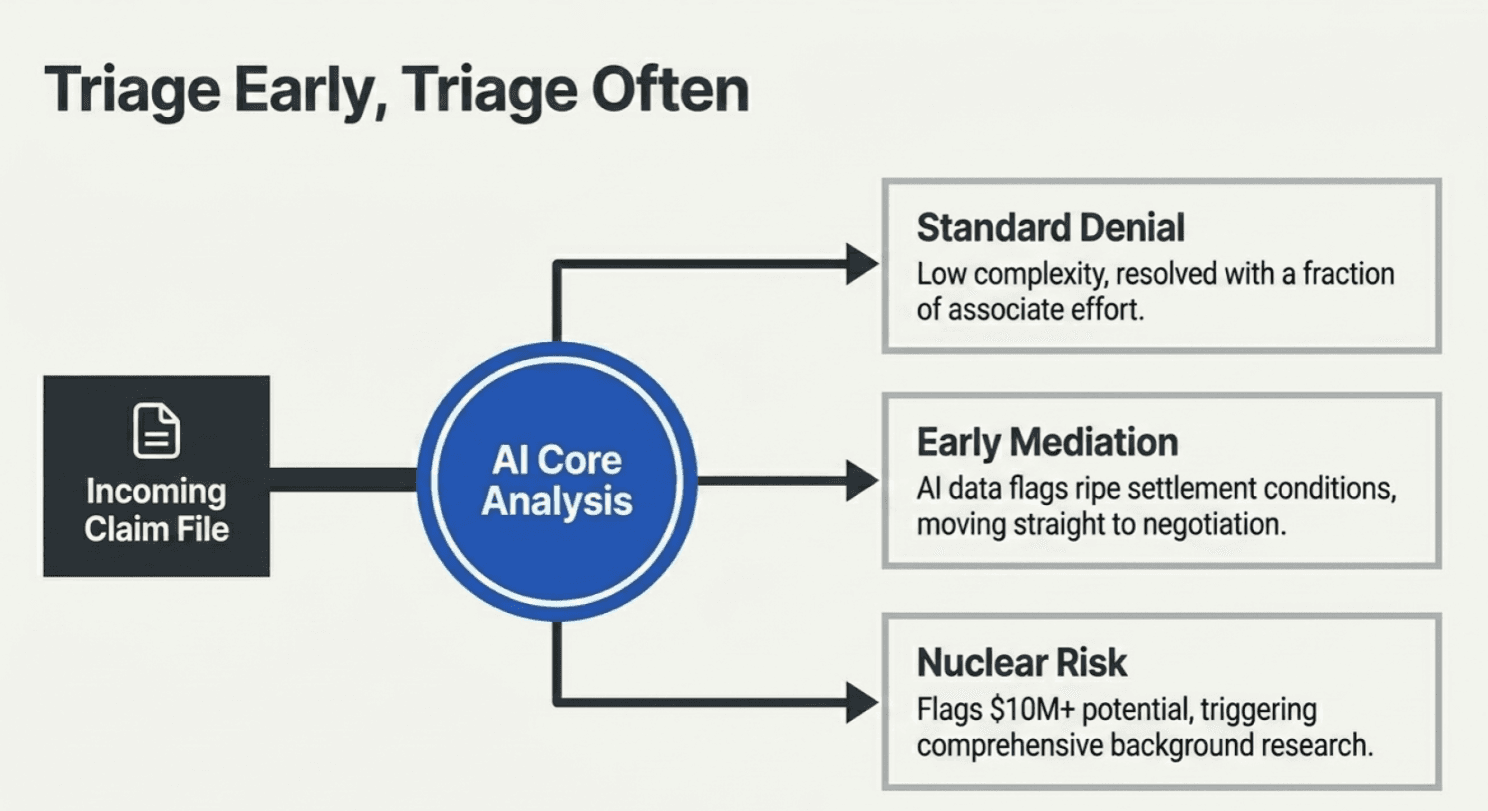

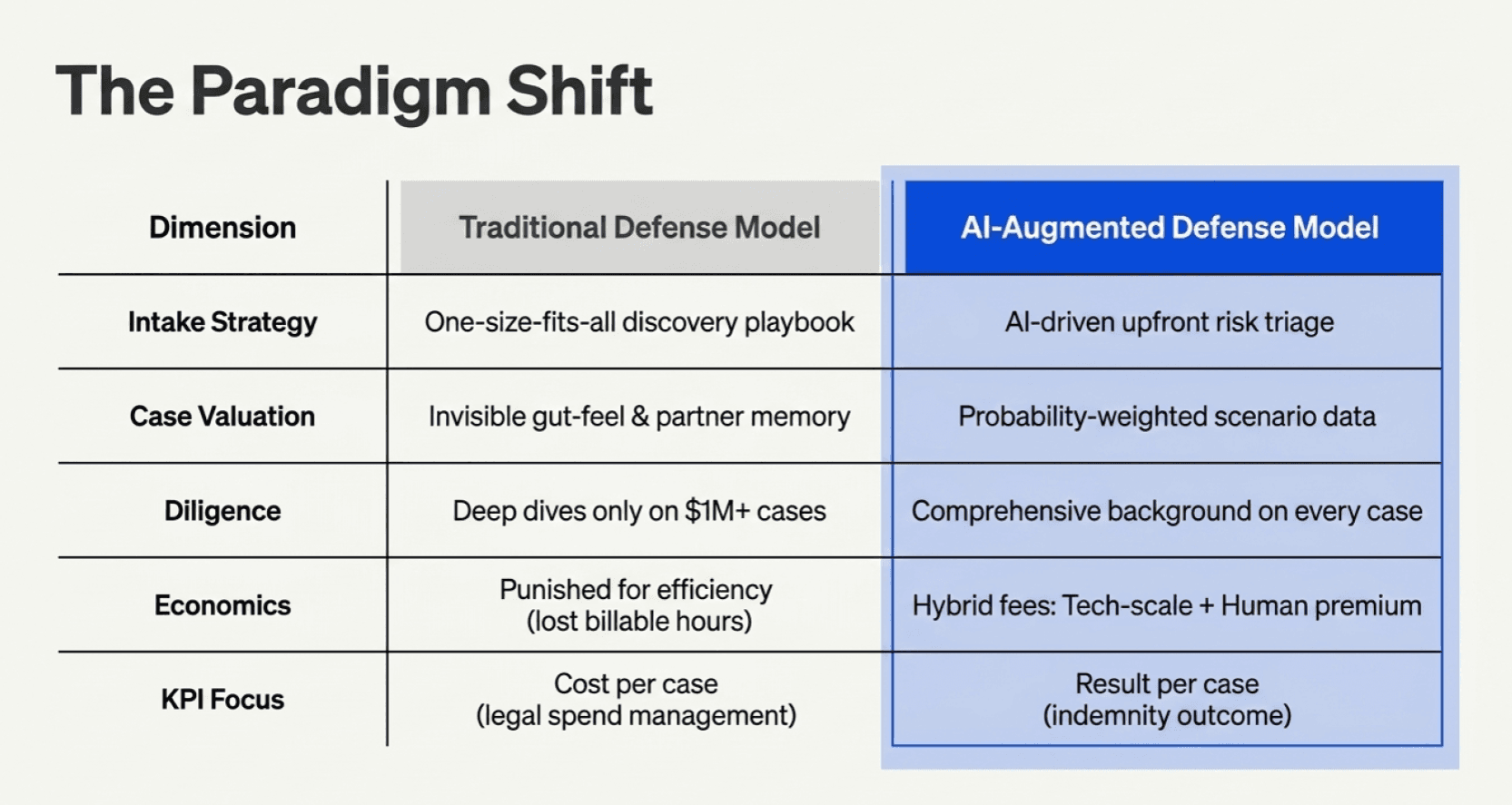

The single highest-leverage intervention AI enables is upfront case triage. Today, most defense firms treat incoming cases with a one-size-fits-all approach: open the file, assign it to the next available attorney, begin the standard discovery playbook. This is roughly as efficient as a hospital emergency room that gives every patient the same battery of tests regardless of whether they arrived with a paper cut or chest pains.

AI can ingest a new claim file — the complaint, medical records, policy documents, prior adjuster notes — and produce an initial risk assessment in minutes rather than the hours or days it currently takes an associate to get up to speed. More importantly, it can classify cases into meaningful tiers: straightforward coverage denials, cases ripe for early mediation, cases that will require deep expert discovery, cases that smell like nuclear verdict candidates.

Different classifications demand different strategies. The low-complexity case that currently absorbs 40 hours of associate time can be resolved with a fraction of that effort if the AI handles the initial factual analysis and drafts preliminary documents. The high-stakes case that might produce a $10 million verdict deserves the deep investigation that was previously uneconomical — hiring the best experts, running comprehensive background research, building a data-driven defense strategy. Triage makes both possible by directing resources where they generate the highest return.

Data-Driven Decisions, Not Gut-Feel Negotiations

Ask an experienced defense attorney how they assess a case’s settlement value and you will hear some version of “experience and instinct.” That instinct is real and valuable — it represents decades of pattern recognition. But it is also invisible, unreplicable, and walks out the door every time a senior partner retires or a midlevel associate decamps for a plaintiff firm.

AI transforms tacit knowledge into explicit, quantifiable intelligence. By analyzing historical case data — outcomes by venue, judge, opposing counsel, injury type, policy limits, demographic factors — it can build scenario-based decision trees that quantify the probable range of outcomes and the expected cost of each strategic path. Should we take this case to mediation now or invest in additional discovery? The answer need not be a guess. It can be a probability-weighted calculation with a clear return-on-investment framework.

This is not about removing human judgment from the equation. It is about giving human judgment better inputs. A managing partner who can walk into a mediation with data showing that cases with this fact pattern, in this venue, against this opposing counsel, settle within a specific range is a more effective advocate than one relying on memory alone. The data does not decide. It illuminates.

Getting a lot more for a little more is tough to resist

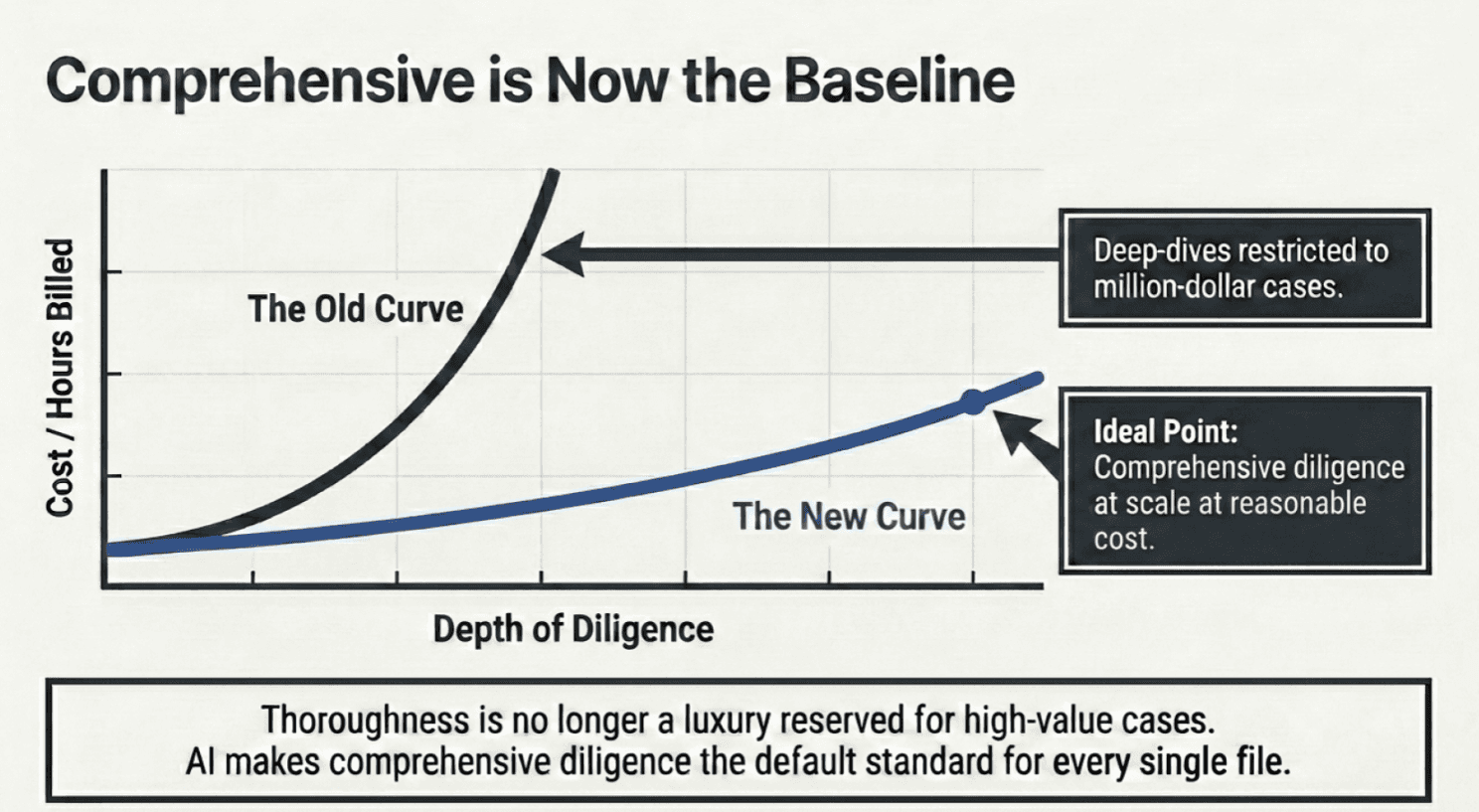

Comprehensive by Default, Not by Exception

There is a persistent myth in insurance defense that thoroughness is a luxury reserved for high-value cases. AI demolishes this assumption by changing the cost curve of analytical work. When a deep-dive analysis of expert credentials costs three hours of associate time, it only happens on million-dollar cases. When AI can perform the same analysis in minutes at negligible marginal cost, it can happen on every case.

This matters enormously for defense quality. Comprehensive case analysis — testing every element of the claim, investigating every potential affirmative defense, evaluating every expert’s track record — is not gold-plating. It is the baseline standard that protects carriers from bad-faith exposure and defense firms from malpractice risk. AI makes comprehensive the default rather than the exception, enabling firms to do more on almost every case while spending less per task.

The practical applications are diverse and immediate: automated analysis of medical records for inconsistencies, systematic background research on opposing experts, comprehensive review of comparable verdicts and settlements in the relevant venue, and real-time monitoring of case developments across a portfolio. Each of these tasks is currently either done inadequately (because there are not enough hours in the day) or not done at all (because no one can justify the cost). AI changes the arithmetic.

Share the Data, Share the Platform

One of the most underappreciated inefficiencies in insurance defense is the communication friction between carriers, counsel, and claims professionals. The state of the art in most defense practices is email — an asynchronous, unsearchable, attachment-heavy medium that was designed for interoffice memos, not for managing complex litigation portfolios.

A shared technology platform changes this dynamic fundamentally. Carriers get real-time visibility into case status, strategy decisions, and budget consumption without waiting for the quarterly status report that is already two weeks late. Defense counsel can access claim files, adjuster notes, and policy documents without the multi-day scavenger hunt that currently precedes every substantive analysis. All parties can see what information exists and what is missing, eliminating the duplication and delay that plague current workflows.

The result is not merely efficiency. It is shared understanding — the kind of alignment between carrier and counsel that produces better outcomes because everyone is working from the same facts, with the same strategic framework, at the same time.

A benefits of Ai Augmentation are hard to ignore

Rewarding the Right Behavior

Here is where most conversations about AI in insurance defense go quietly off the rails. The technology is ready. The workflows can be redesigned. But the incentive structures that govern the industry were built for a world without AI, and they actively punish firms that adopt it.

Consider the economics. A defense firm that uses AI to complete in two hours what previously took ten has just eliminated eight billable hours from its invoice. Under the traditional model, the firm’s reward for delivering better, faster work is an 80% reduction in revenue. The carrier’s bill review software, meanwhile, will flag the remaining two hours for audit anyway.

(The incentive to adopt AI, in other words, is roughly equivalent to the incentive to saw off the branch you’re sitting on.)

The solution is not to abandon the billable hour entirely — that cockroach of legal economics has survived every extinction event thrown at it, including the internet, alternative fee arrangements, and at least three McKinsey reports predicting its demise. Instead, the solution is to create a hybrid model: fixed fees for AI-augmented analytical work, where the firm captures the efficiency gain; billable hours for the high-judgment, high-skill work — depositions, mediations, trial preparation — where human expertise commands a premium; and shared-success arrangements tied to outcomes, where both carrier and counsel benefit when the defense strategy produces a better result than historical norms would predict.

Alternative fee arrangements are not new. But AI makes them workable at scale by providing the data infrastructure needed to price risk accurately and measure performance objectively. Without data, fixed fees are a guessing game that favors whichever party guesses better. With data, they become a rational allocation of risk and reward that aligns incentives for the first time in the industry’s history.

Working with both carriers and defense firms on this transition, what becomes clear is that the challenge is less technical than organizational. The technology to do all of this exists today. What’s scarce is the willingness to rethink workflows, billing structures, and roles that have calcified over decades. The firms and carriers who demonstrate that flexibility — who treat this as a strategic transformation rather than a software purchase — will capture disproportionate value. Litigation is, after all, one of the single largest cost centres on any carrier’s balance sheet. Even modest improvements in how it is managed compound into hundreds of millions of dollars.

Not all cost cutting is equal

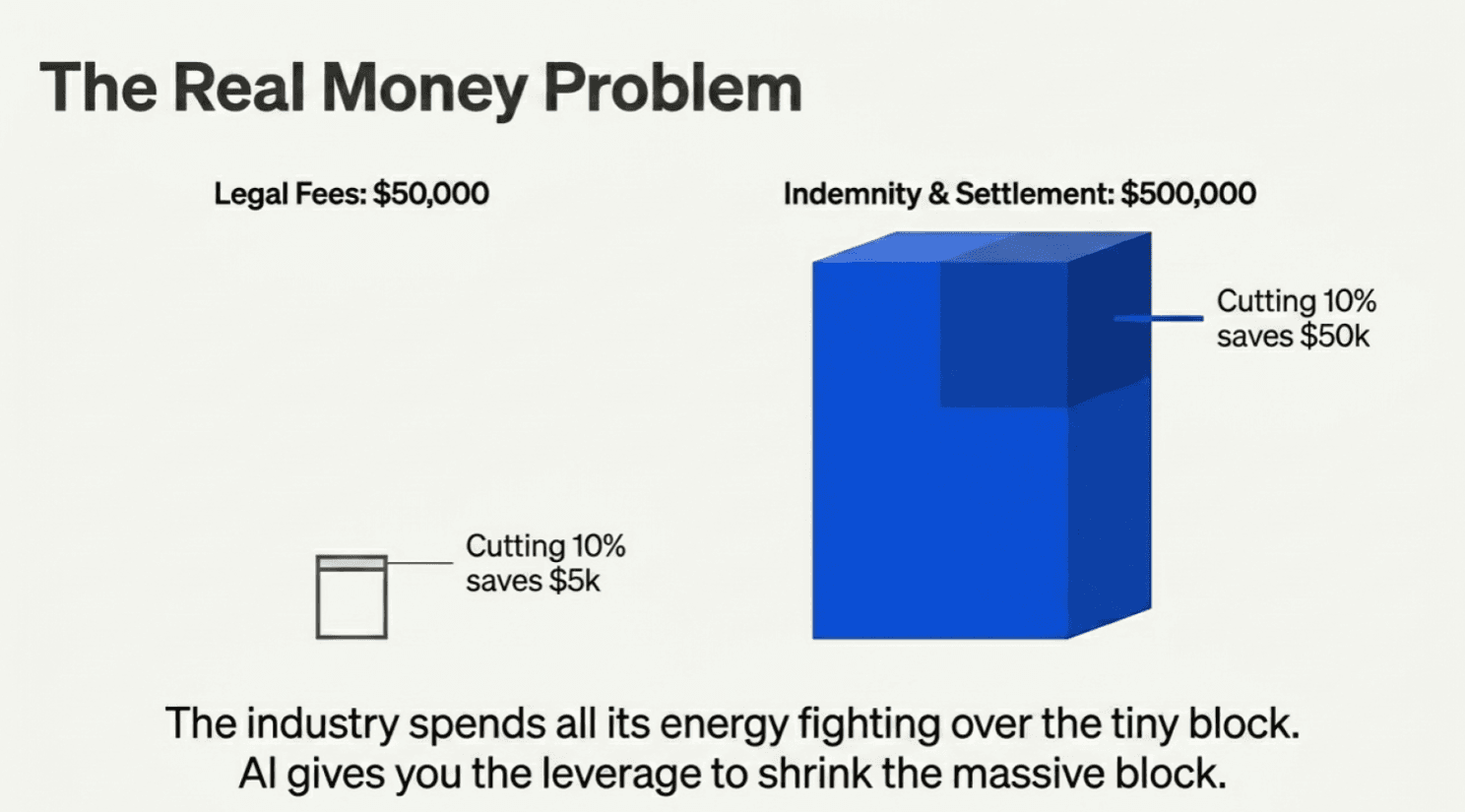

The Real Money Problem

Defense firms and carriers spend enormous energy fighting over legal fees — a battle over the cost to litigate. But the real money in insurance claims is not the cost to litigate. It is the indemnity payment: the settlement or verdict that resolves the claim.

Consider a case with $50,000 in legal fees and a $500,000 settlement. Reducing the legal fees by 10% saves $5,000. Reducing the settlement by 10% — through better case assessment, smarter negotiation, or more effective defense strategy — saves $50,000. The arithmetic is not subtle.

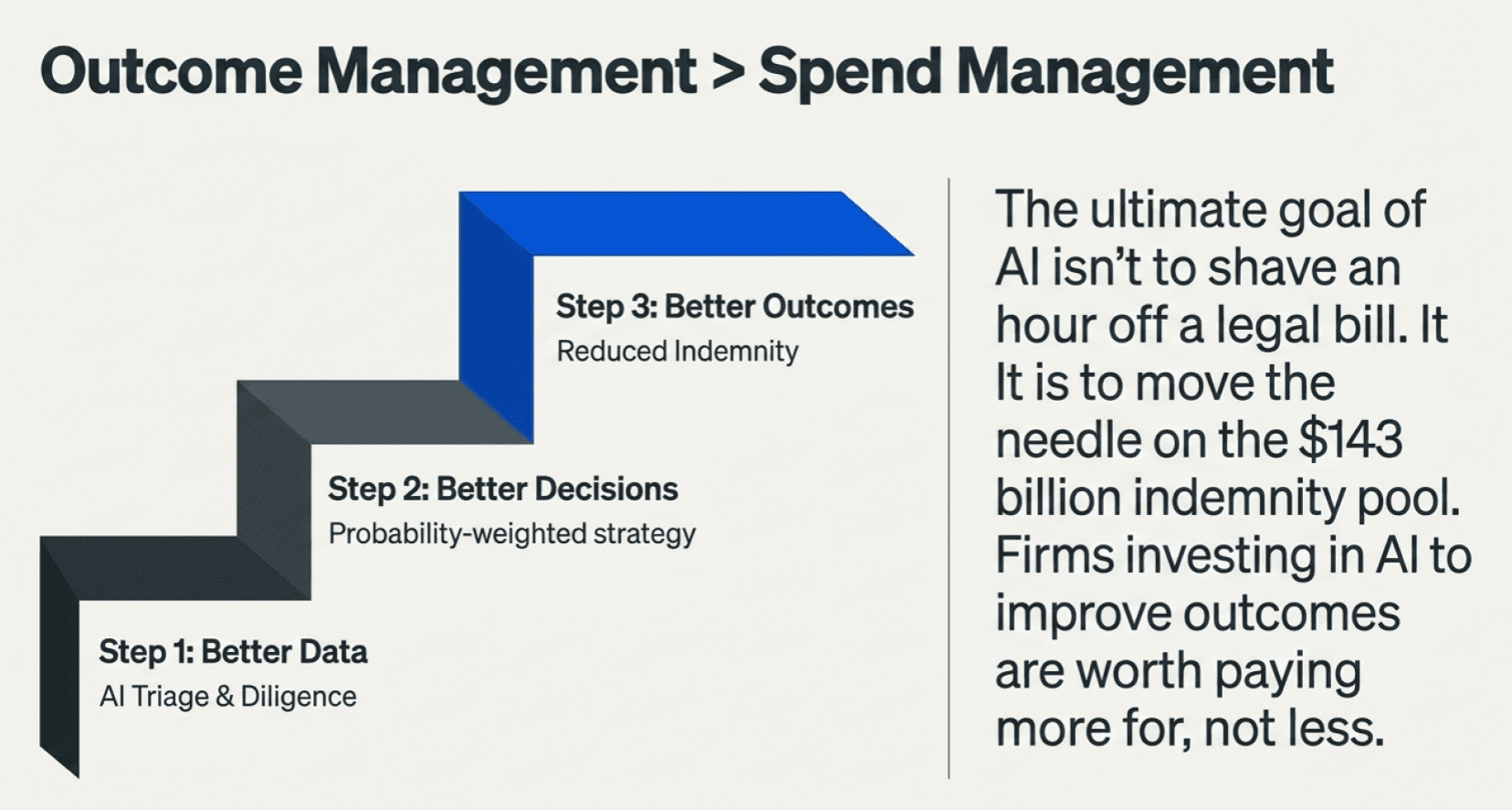

AI’s greatest potential in insurance defense is not cost reduction. It is outcome improvement. By providing data-driven case evaluation, identifying the cases that should be settled early versus those that should be defended aggressively, and enabling the comprehensive investigation that strengthens negotiating position, AI can move the needle on indemnity — which is where the vast majority of claims dollars actually sit.

Carriers who recognize this will shift their focus from legal spend management to outcome management. They will start measuring defense firms not by the cost per case but by the result per case. And they will discover that the firms investing in AI to improve outcomes are worth paying more, not less, for their services.

Step by Step the Industry is going to transform

Start with Process, Graduate to Outcomes

The measurement challenge is real. Defense outcomes are noisy, slow to materialize, and difficult to benchmark. A case that settles for $200,000 — was that a good result or a bad one? Without comparative data, it is impossible to say.

The practical path forward begins with process metrics — measurements that are immediately observable and directionally predictive of outcomes. Response time is the obvious starting point: carriers consistently rank responsiveness as their top criterion for selecting and retaining defense firms, and AI-augmented firms can deliver case assessments, strategy recommendations, and status updates dramatically faster than traditional practices. Comprehensiveness is another: are all aspects of the claim being investigated? Are all potential defenses being evaluated? Are expert analyzes being conducted where warranted?

Over time, as AI accumulates data across hundreds and then thousands of cases, process metrics can evolve into outcome metrics: average settlement relative to initial demand, verdict frequency, time to resolution, total cost of claim (indemnity plus expense). These metrics will, for the first time, allow carriers to identify which firms deliver outsized results and compensate them accordingly. The virtuous cycle — better data produces better decisions, better decisions produce better outcomes, better outcomes justify higher investment — begins with measurement.

The Human in the Loop

Nothing in this plan diminishes the role of the experienced defense attorney. If anything, it amplifies it. When AI handles the analytical grunt work — the document review, the case research, the initial risk assessment — it frees senior attorneys to do what they were trained for and what no machine can replicate: exercising expert judgment on strategy, reading the room in a deposition, persuading a jury, and building the relationships with claims professionals and opposing counsel that determine how cases actually get resolved.

The model is not attorney-or-AI. It is attorney-and-AI, with each contributing what it does best. The senior partner’s three decades of trial experience become more valuable, not less, when paired with a comprehensive data analysis of every comparable case in the jurisdiction. The associate’s sharp legal mind becomes more productive, not redundant, when freed from spending 60% of their time on tasks that a machine can perform faster and more consistently.

This has implications for the talent crisis too. A firm that offers associates the chance to work on substantive legal strategy from day one — rather than spending their first three years buried in document review — becomes a dramatically more attractive employer. AI does not replace the associate. It promotes them.

Two paths diverged in a yellow wood and I took the one less traveled by...and that has made all the difference

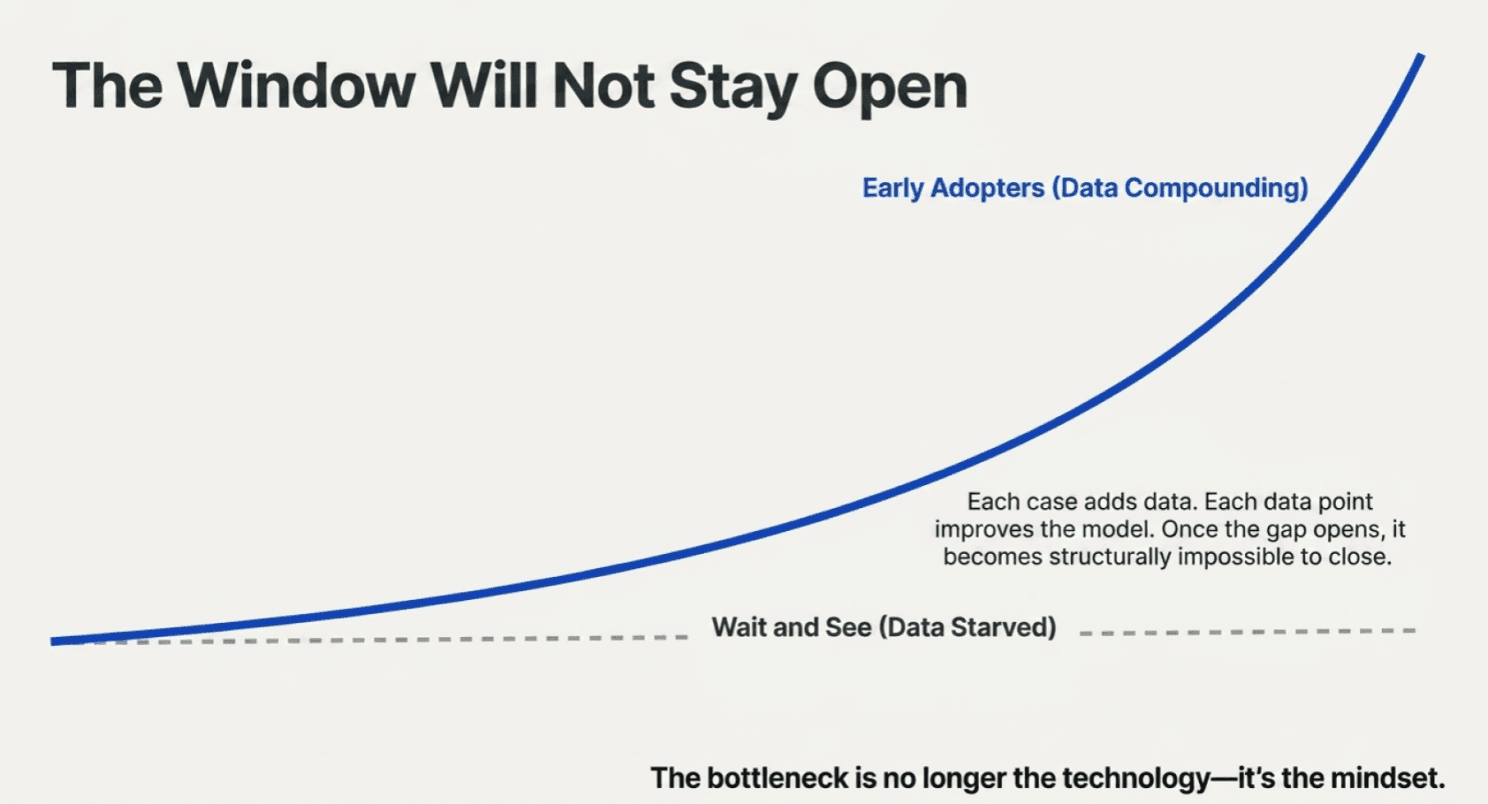

The Window Is Open. It Will Not Stay That Way.

The firms that build their AI capabilities now — investing in data infrastructure, redesigning workflows, developing the metrics that prove their value — will compound their advantages with every case they handle. Each case adds data. Each data point improves the model. Each improvement widens the gap between firms that adopted early and firms that waited.

The firms that wait will find themselves in a different kind of spiral. Without AI, they cannot match the comprehensiveness or speed of their competitors. Without competitive differentiation, they lose cases — and eventually clients. Without clients, they lose the data that could have powered their own AI adoption. The window of opportunity is not permanent. Once the gap opens, it becomes structurally difficult to close.

This is not technology for technology’s sake. It is a once-in-a-generation opportunity to redesign how insurance defense works — to deliver better outcomes for carriers, better economics for firms, and better justice for the policyholders who are, after all, the reason this entire industry exists. The plan is not complicated. The technology is not the bottleneck. The bottleneck is the mindset — the willingness of people who have built successful careers doing things one way to consider that there might be a better way. The firms and carriers who clear that hurdle will not merely survive what is coming. They will define it. And the rest will wonder why no one warned them. (Someone did.)

Andy Anderson is a former insurance analyst on Wall Street, a repeat founder in insurtech, and the co-founder of OraClaim — a platform built specifically to help defense attorneys and carriers manage their litigated claims.

Notes

[1] Allianz Commercial, "Five Key Liability Claim Trends," 2024. Cited in Risk & Insurance, November 2024. https://riskandinsurance.com/nuclear-verdicts-drive-rising-us-liability-claims/

[2] Chambers and Partners, "Litigation Funding 2025: Global Practice Guide," 2025. https://practiceguides.chambers.com/practice-guides/litigation-funding-2025

[3] Marathon Strategies, "Corporate Verdicts Go Thermonuclear: 2025 Edition," May 2025. Cited in Insurance Journal. https://www.insurancejournal.com/news/national/2025/05/22/824792.htm

[4] Sedgwick, "2025 Liability Litigation Commentary," 2025. https://www.sedgwick.com/blog/inside-the-verdict-what-is-driving-the-rise-in-nuclear-and-thermonuclear-awards/

[5] U.S. Chamber of Commerce, Institute for Legal Reform, "Nuclear Verdicts: An Update on Trends, Causes, and Solutions," May 2024. https://instituteforlegalreform.com/research/nuclear-verdicts-an-update-on-trends-causes-and-solutions/

[6] Bottomline Legal Spend Management, 2024; Bill ReviewIQ. Savings estimates of 6-10% per invoice are industry-standard benchmarks. https://www.billreviewiq.com/legal-bill-review/

[7] U.S. Chamber of Commerce, Institute for Legal Reform, "Nuclear Verdicts: An Update on Trends, Causes, and Solutions," May 2024. https://instituteforlegalreform.com/research/nuclear-verdicts-an-update-on-trends-causes-and-solutions/

[8] Insurance Business America, "Will Nuclear Verdicts Impact the Insurance Industry in 2025?" January 2025. https://www.insurancebusinessmag.com/us/news/breaking-news/will-nuclear-verdicts-impact-the-insurance-industry-in-2025-519537.aspx

[9] Casualty Actuarial Society and Insurance Information Institute, "Increasing Inflation on Liability Insurance," November 2025. https://www.casact.org/article/new-cas-and-triple-i-analysis-quantifies-impact-legal-system-abuse-liability-insurance

[10] The Legal Intelligencer, "Insurance Defense Firms Still Struggle to Recruit Despite Increased Demand," January 2026. https://www.law.com/thelegalintelligencer/2026/01/12/insurance-defense-firms-still-struggle-to-recruit-despite-increased-demand/

[11] DealCloser/NALP Foundation, "From Attrition to Retention: A New Playbook for Law Firms," February 2025. https://blog.dealcloser.com/blog/from-attrition-to-retention-a-new-playbook-for-law-firms