Future of Claims

The Rider, the Elephant, and the Path to AI Transforming Claims

There is a quiet contest underway in insurance defense, and the prize is the next decade. The contestants are managing partners and carrier executives. They are not competing on demos or contracts. They are competing on something less visible and much harder: how seriously they are taking the human side of AI adoption.

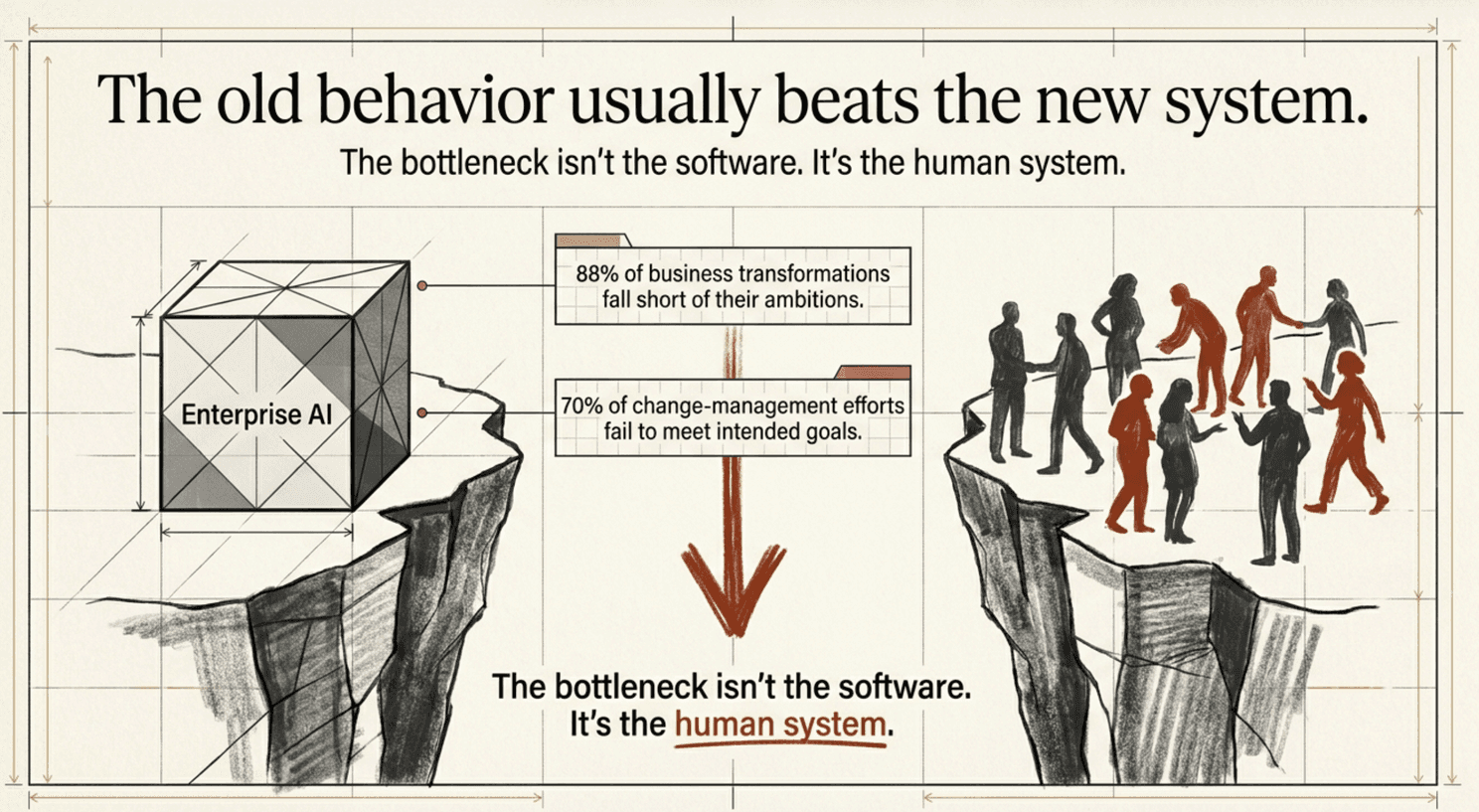

I say that as someone who co-founded an AI company for insurance defense and is therefore, in some professional sense, contractually obligated to believe in the technology. I do believe in it. But the bottleneck is not the software. The bottleneck is the human system around the software — and we now have a fairly clear picture of what separates the firms that capture value from the ones that capture press releases.

What the Winners Have in Common

Begin with the unflattering numbers, because they earn the rest. McKinsey has reported for years that roughly seventy percent of change efforts fail to meet their goals [1]. Bain's 2024 work found that 88% of business transformations fell short of their ambitions [2]. MIT's recent enterprise-AI study found that only about five percent of corporate AI projects deliver measurable ROI [3]. These are not new failure modes. The AI cycle has them on display in unusually high relief.

The five percent who succeed are not luckier or smarter or richer. They behave differently in identifiable, repeatable ways. McKinsey's 2025 review of more than two hundred at-scale AI transformations finds that high performers are nearly three times as likely as their peers to have fundamentally redesigned individual workflows around the new tools, rather than bolting AI onto whatever they were already doing [4]. Boston Consulting Group concludes that roughly 70% of the difficulties in AI projects stem from people and processes, not technology [5]. A Stanford study of fifty-one successful enterprise deployments puts it more bluntly: the technology is consistently described as the easiest part. Companies that win invest one dollar in the model and as much as ten dollars in the surrounding human and operational changes [6].

Three patterns recur in the success cases.

The winners redesign the work, not just the tool. They do not ask, "How do we add AI to what we already do?" They ask, "If AI were a quiet, fast, infinitely patient colleague who had already done the reading, what would the case file look like on day one?" — and then they build the answer.

The winners start small and ship visible wins. They do not announce a transformation. They find a single bottleneck — usually the most painful, repetitive, soul-deadening one — and fix it cleanly enough that the team starts asking what's next. Newton's first law applies to organizations as reliably as to objects: a body at rest stays at rest; a body in motion stays in motion. The whole job of the first six weeks is to get the thing moving.

The winners treat adoption as a leadership problem. McKinsey's most recent finding is that the largest single barrier to scaling AI is no longer employee resistance — it is leadership inertia [4]. The senior leaders who clear obstacles, communicate the why, and make AI adoption a measure of organizational success are the ones whose teams pull the technology toward themselves. The senior leaders who buy the software and then return to other priorities are the ones whose licenses are still sitting unused six quarters later.

None of this is mysterious. It is also, as a matter of historical record, not what most organizations do.

The Manual Island

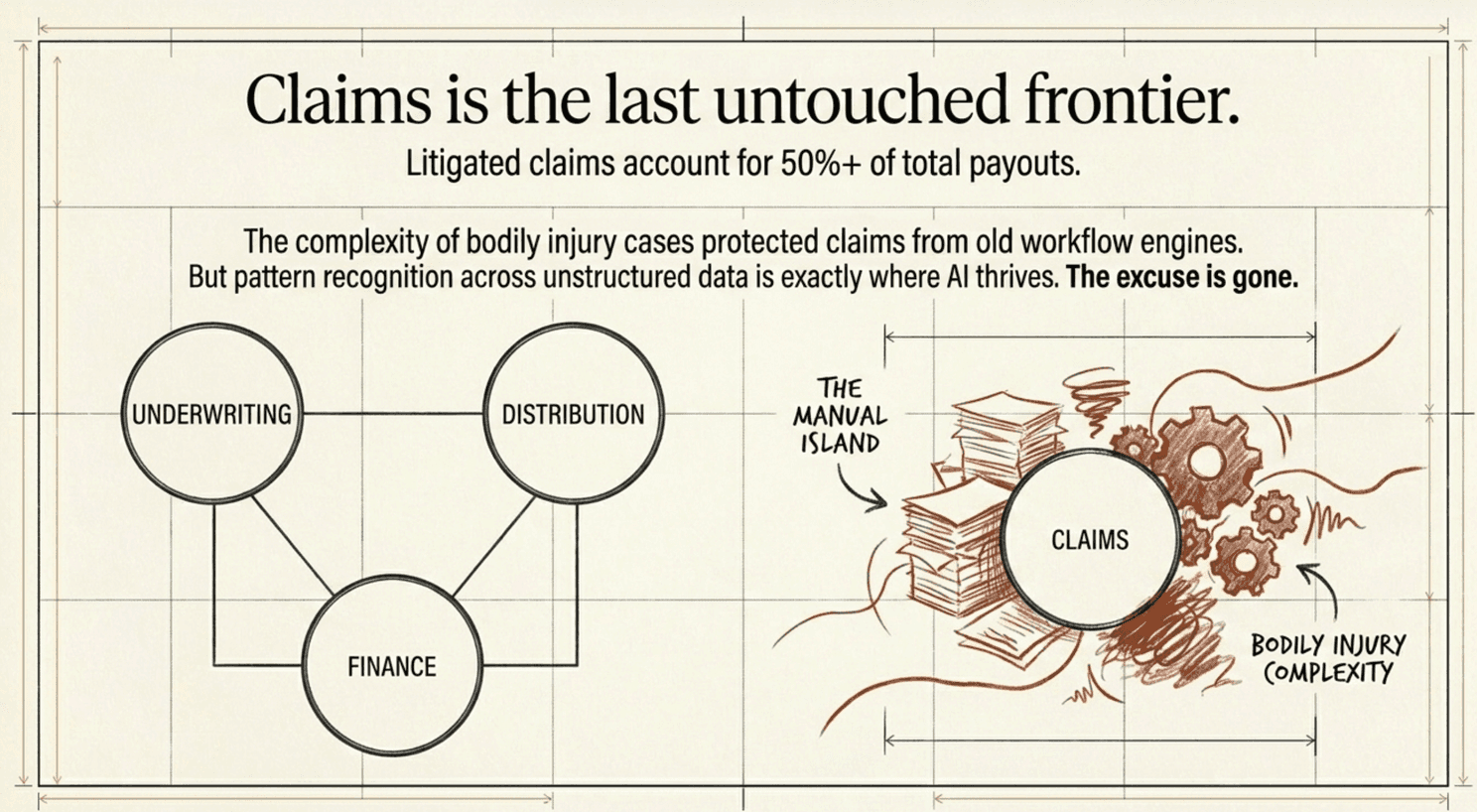

Begin where the industry actually is. Claims has been the least-invested part of the insurance value chain for as long as most of us have been in business. Underwriting has been transformed. Distribution has been transformed. Policy administration, finance, compliance — all substantially modernised. Claims, and especially the litigated claim, is still largely run on individual judgment, tribal knowledge, and documents nobody has time to read.

The defenders of this arrangement have always had a reasonable-sounding excuse. Claims is complex. Every file is different. You cannot stuff that into a workflow engine. They were right. Workflow engines were the wrong tool. But AI is precisely the technology that handles complexity — pattern recognition across unstructured data, reading medical records and demand letters at a scale and consistency no human team can match. The complexity that protected claims from technology for thirty years is now the domain where AI has its largest advantage. The excuse is gone.

There is a Pareto problem waiting at the end of this thought. Sedgwick's own book of business shows that litigated claims account for fifty percent or more of total claims payouts [7]. A small share of files drives most of the cost, and most of the existing technology investment in claims is pointed at the other ninety-nine and a half percent. Property claims, small auto files, things you can handle with a photo. Those automations are fine. They are the appetizer. The main course is the litigated file, and it is there that human judgment, combined with machine capability, produces the returns that actually matter.

The Squeeze, the Spread, and the Power Law

Readers of last week's piece in this newsletter will remember the shape of the larger problem. U.S. commercial casualty losses ran at roughly $143 billion in 2023, exceeding the cost of every natural catastrophe on Earth that year combined [8]. Nuclear verdicts hit a record $31.3 billion in 2024 [9]. Defense firms are caught between a plaintiff bar with hedge-fund money and clients with audit software. That is the squeeze.

The point worth restating is the one that determines who keeps practicing law: roughly eighty-five percent of total claims costs sit in indemnity, not in legal spend. Cutting a defense bill by ten percent saves a few thousand dollars on the kind of case where moving the settlement by ten percent would save tens or hundreds of thousands. Efficiency, on the legal-spend line, is a rounding error. Real leverage is in how cases are staffed, priced, and decided.

The implication people are not yet talking about loudly enough is that the benefits of this transition will not be evenly distributed. Technology, in industries with significant variance in execution, tends to amplify power laws rather than flatten them. Firms that adopt AI thoughtfully — that redesign workflows, train their people, and present a credible story to carriers about better outcomes at lower cost — will take share. They will raise rates while their less-organized peers cut them; we have watched defense firms negotiate forty-percent rate increases based on demonstrable, AI-enabled performance. They will move toward hybrid and outcome-linked fee structures, capturing margin rather than being commoditized under hourly billing. They will become the panel firms that carriers consolidate to. The carriers that move with them will see the matching benefit on the other side: lower indemnity through better triage and harder defense on the cases that deserve it. With combined ratios in commercial casualty under sustained pressure, even a few points of improvement on the loss line is the difference between a profitable year and an apologetic one.

The firms and carriers that hesitate, that pilot endlessly without committing, that buy software and never redesign workflow, will not lose all at once. They will lose slowly, in the form of clients quietly migrating, talented attorneys quietly leaving, and rate negotiations quietly going the other way. Some will not realize they have lost until the gap is permanent. This is what a power law looks like in real time.

The Rider, the Elephant, and the Path

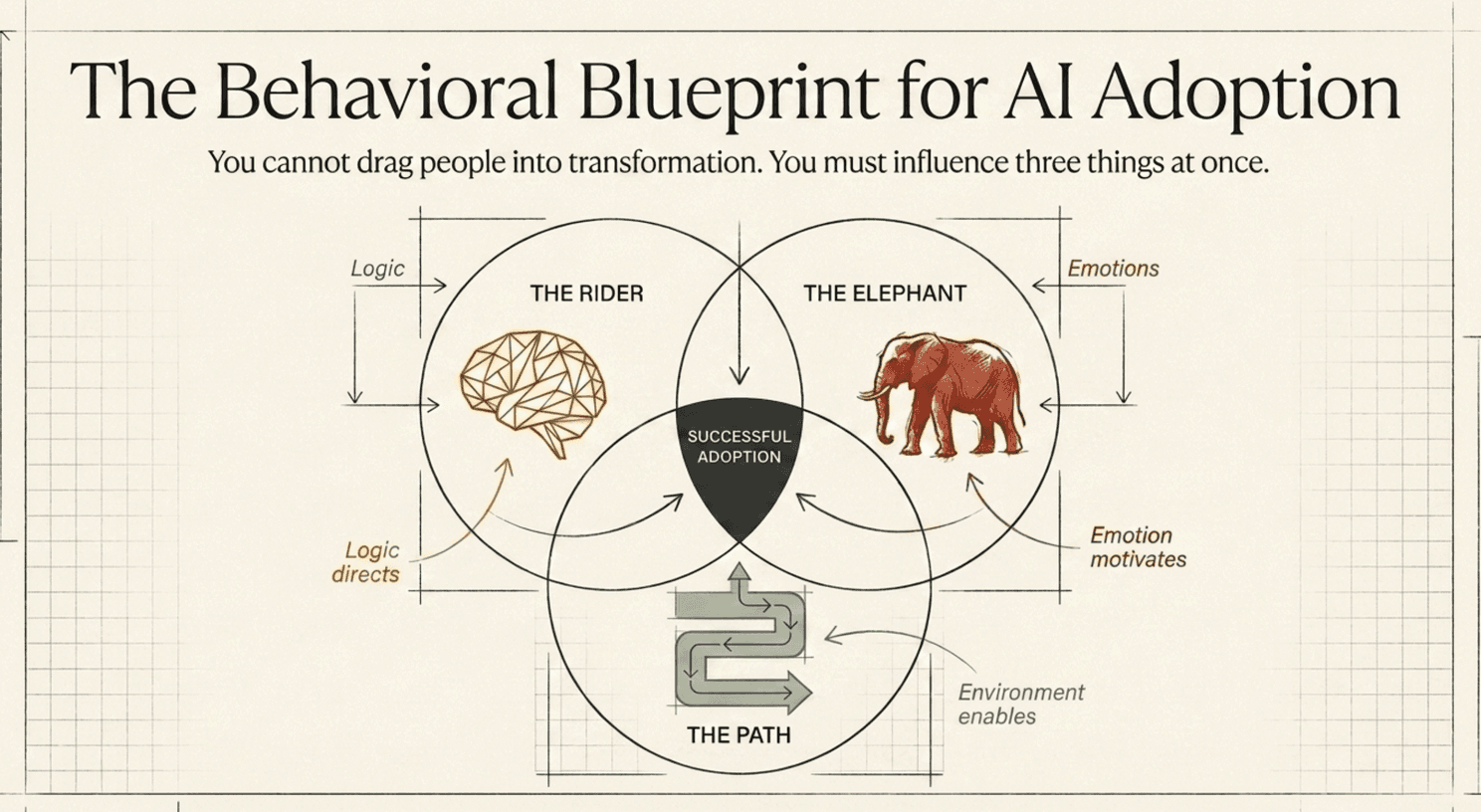

Most insurance executives are familiar with some version of the McKinsey triad: People, Process, Technology. It is useful, but it undersells the human dimension by listing it first and then moving on.

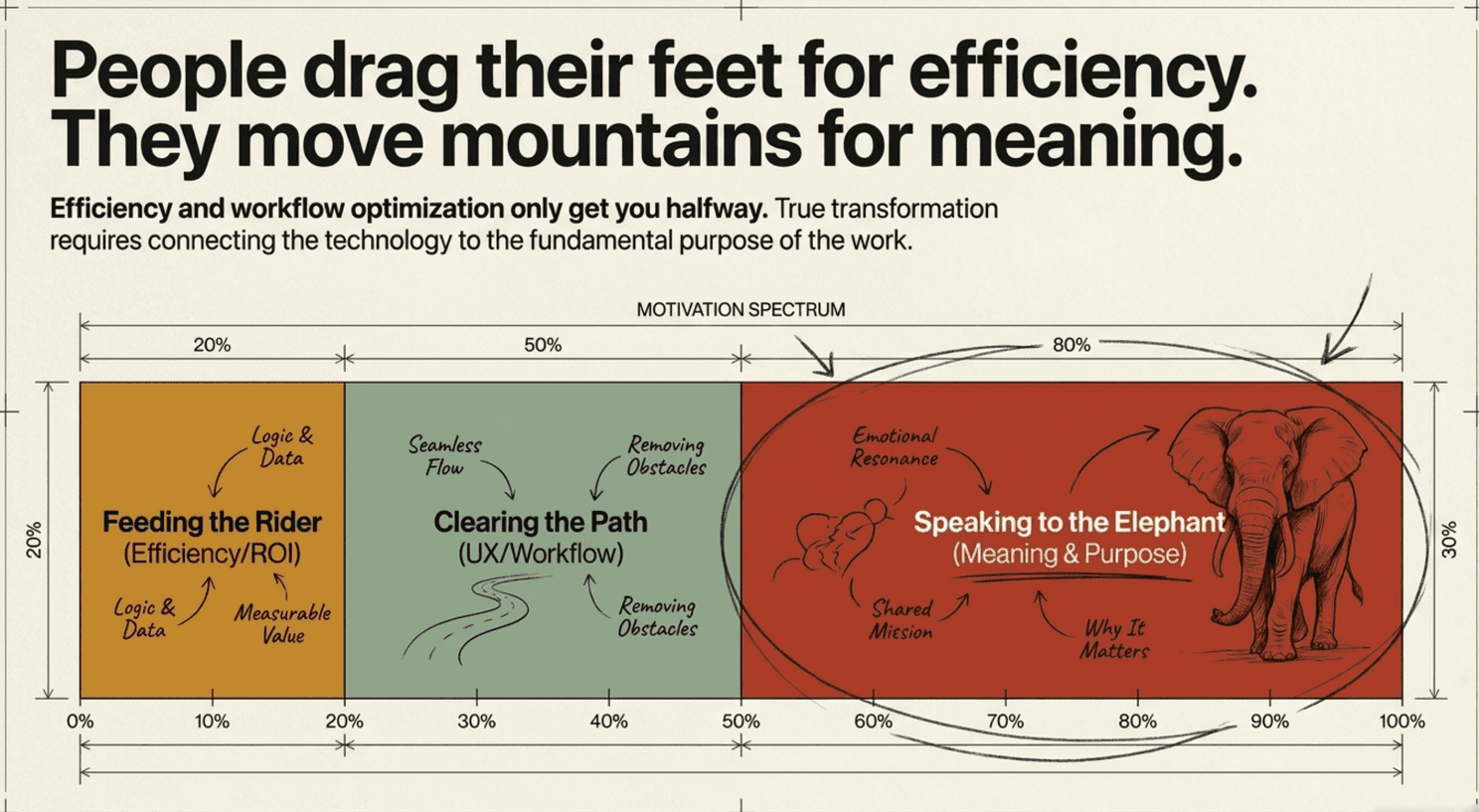

A better frame comes from the behavioral psychologists Chip and Dan Heath, in their book Switch. Any effort to change how people behave, they argue, is really an attempt to influence three things at once — what they call the Rider, the Elephant, and the Path [10].

The Rider is the analytical mind. The part that reads data, follows logic, and responds to ROI. Show the Rider a good spreadsheet and the Rider nods.

The Elephant is the emotional mind. The part that has been doing the same work for fifteen years and has heard many promises about tools that will "make your job easier." The Elephant is skeptical, tired, and — importantly — much larger than the Rider. You cannot drag the Elephant. You have to motivate it.

The Path is the environment. The workflow. The actual sequence of steps a human being takes, every day, to do their job. A motivated Rider on a willing Elephant will still fail if the path requires seventeen extra clicks, a second login, and a format nobody else uses.

Most AI projects do not fail because the technology was bad. They fail because nobody thought hard enough about the Elephant and the Path.

It's hard to argue with numbers

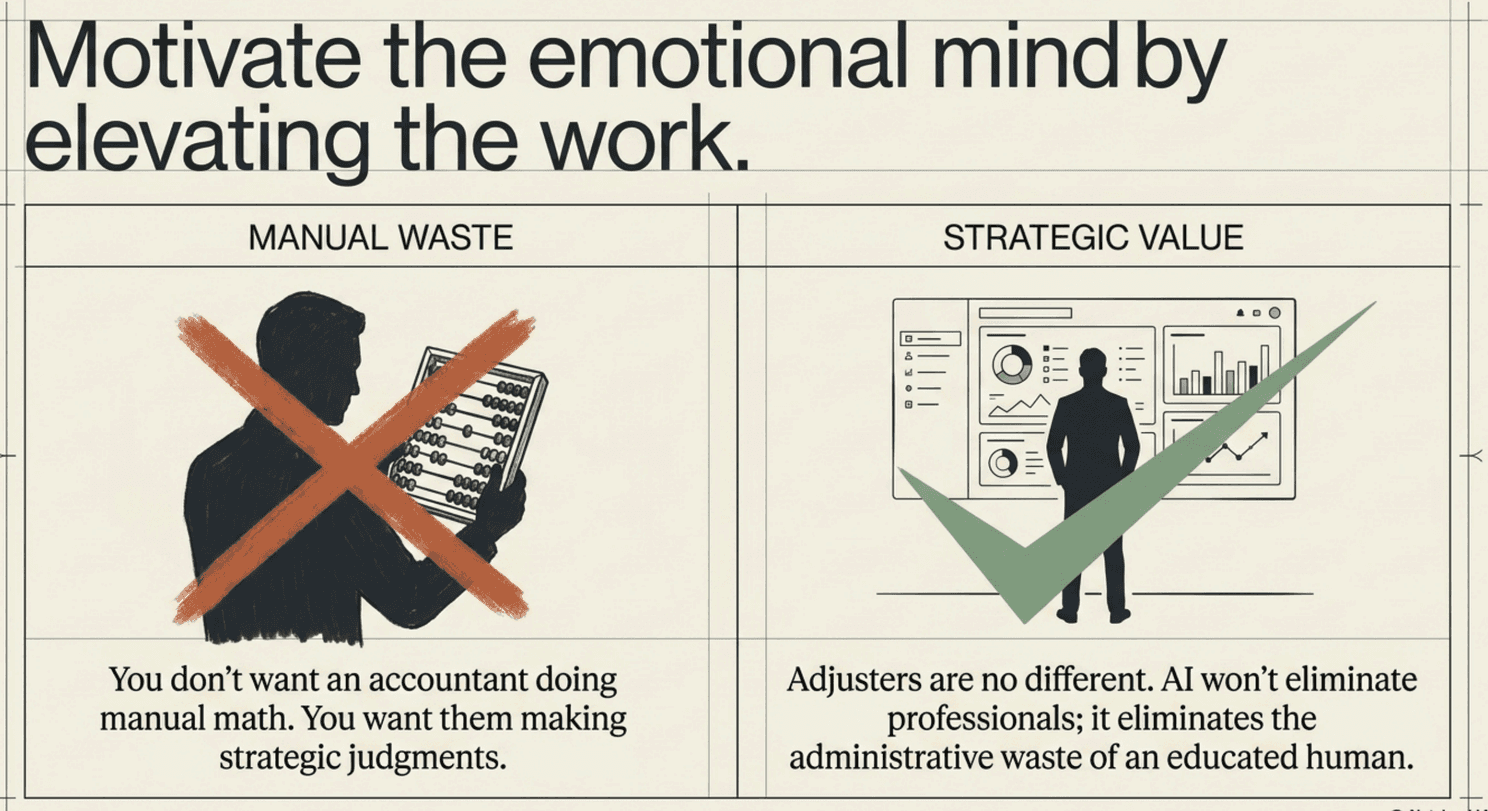

Feeding the Rider

It is still worth feeding the Rider, because without the business case, none of the rest matters. The case for AI in litigated claims is no longer in serious dispute.

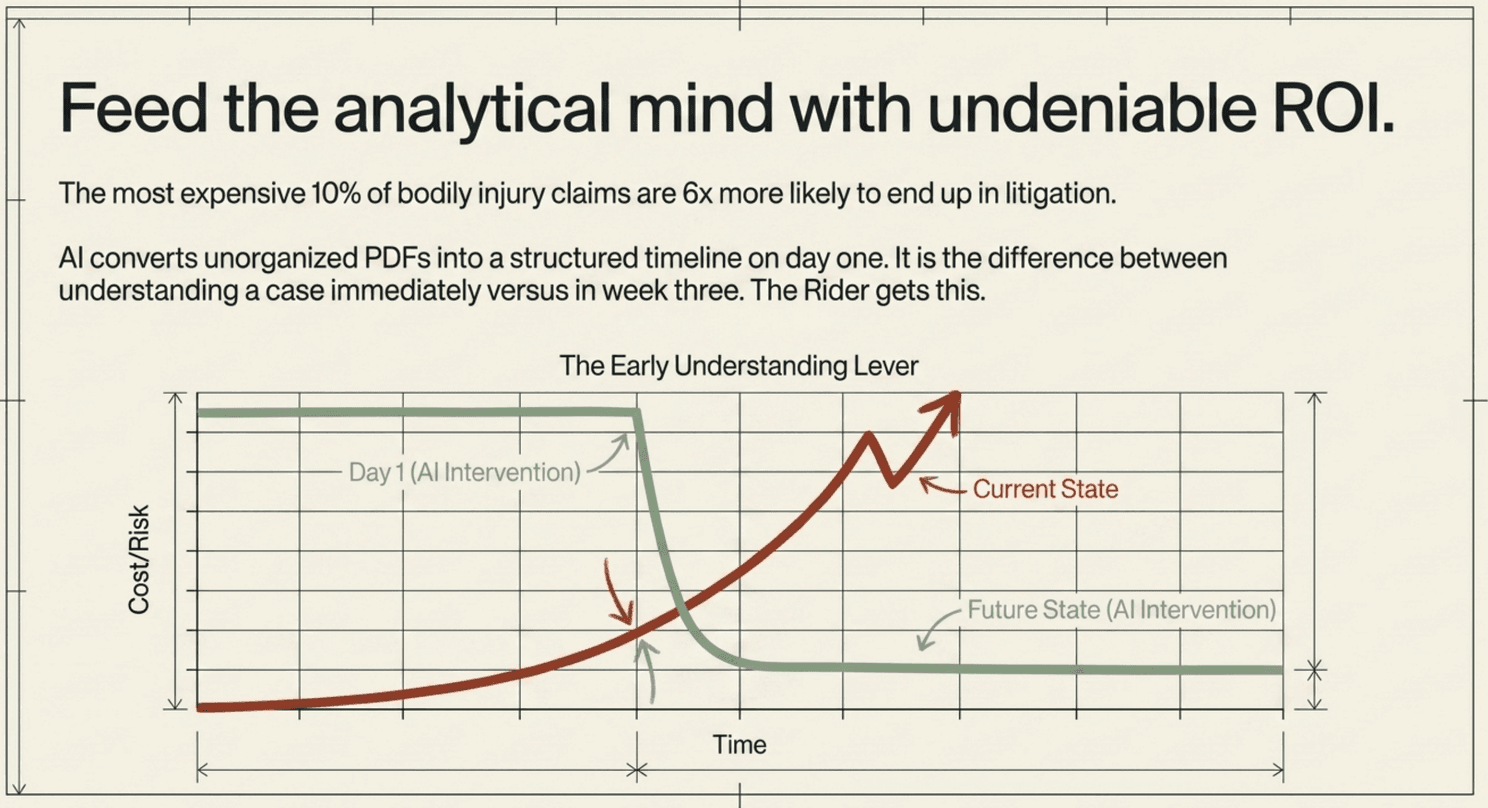

An adjuster or attorney opening a new litigated file today is typically looking at a folder of unorganized PDFs: police report, medical records from four providers, demand letter, photos, witness statements, and sometimes video. Reading carefully and extracting what matters takes hours on a simple file and a full day on a complex one. Every hour between the moment the file opens and the moment someone understands it is time the case sits still — and cases, like most problems, do not improve by sitting still.

AI does the reading. Documents are classified and organized automatically. Medical records become a structured timeline, provider by provider, with gaps flagged and pre-existing conditions surfaced. The demand letter gets compared against the record for consistency. By the time the adjuster opens the file in the morning, a first draft of the case already exists.

That is not a minor efficiency gain. It is the difference between understanding a case on day one and understanding it in week three. Given that the most expensive 10% of bodily injury claims are six times more likely to end up in litigation [11], early understanding is the single largest lever a defense operation has over its own outcomes.

The Rider, shown the numbers, will generally sign the contract. The trouble starts at the next meeting.

Speaking to the Elephant

At every AI rollout I have watched in this industry, there is a moment in a conference room when a senior leader says some version of: "This is great. The team is going to love it." The team, at that same moment, is probably down the hall, wondering whether they are about to be automated into early retirement.

That fear is worth taking seriously. It is also, in this industry, more misplaced than almost any other.

Consider the historical evidence first. Research published in the Quarterly Journal of Economics by MIT's David Autor and his co-authors found that roughly sixty percent of the jobs Americans hold today did not exist in 1940 — implying that more than eighty-five percent of employment growth over the last eighty years has come from technology-driven creation of new occupational categories [12]. Goldman Sachs's 2025 work on the labor-market impact of generative AI leans heavily on the same finding to argue that the AI transition will produce frictional unemployment for a few years, not permanent displacement; their estimate for the eventual U.S. unemployment bump is half a percentage point [13]. Predictions that technology will eliminate work, as Goldman's authors note in their characteristic understatement, have a long history but a poor track record.

Now consider the specific situation of insurance defense. This industry does not have a problem of too many people doing work that AI could do. It has the opposite problem: not enough people are willing to do the work, and a workforce that is rapidly retiring without an obvious replacement. The U.S. insurance industry is projected to lose roughly 400,000 workers to attrition by 2026 [14], and only 4% of millennials are considering insurance careers [15]. On the defense law-firm side, the Claims and Litigation Management Alliance's most recent task-force survey found that 90% of insurance defense firms describe recruitment as harder than it was five years ago, and 60% are turning down work due to capacity issues [16]. Mid-level associates have become so scarce that managing partners describe finding them as "winning the lottery" [16].

Whatever you are worried about, AI is unlikely to be the thing that displaces your team. The thing displacing your team is already retirement, and the question is: who will do the work they leave behind? Forty percent of an adjuster's time is currently spent reading records and writing summaries, which is the part of the job no one was lining up to do anyway. The hours an associate spends drafting first-pass discovery responses are not the hours that drew them to law school. AI will not eliminate claims professionals. It will change what the job is — and the change, properly handled, is overwhelmingly in the direction of work that human beings actually want to do.

There is a recruiting argument hidden inside this. The kinds of professionals firms are struggling to attract — younger lawyers, second-career adjusters, the technically curious, the ambitious — generally do not want a job that consists primarily of administrative paperwork. They want to make decisions, use judgment, feel that their day mattered. A firm that adopts AI well can credibly offer them work that emphasizes strategy over summarising, complex cases over commodity ones, outcomes over hours. PwC reaches the same conclusion: firms that present themselves as technology-forward are the most attractive to the candidates the industry most needs [17]. AI is also, by extension, a compensation story. Fewer write-downs, higher rates justified by demonstrable outcomes, hybrid and outcome-linked fees unlocking margins that hourly billing has compressed for a decade — the economics point toward a profession that is more interesting to do and potentially more lucrative for the people doing it.

Leaders communicating any of this to their teams should be honest rather than reassuring. Don't promise that nothing will change. Things will change. What you can truthfully say is that the ones who embrace the change will be more capable, more valued, and more useful to their clients than the ones who spend another decade doing administrative tasks a machine can now do in seconds. The Elephant responds to honesty. It is remarkably good at detecting the other kin

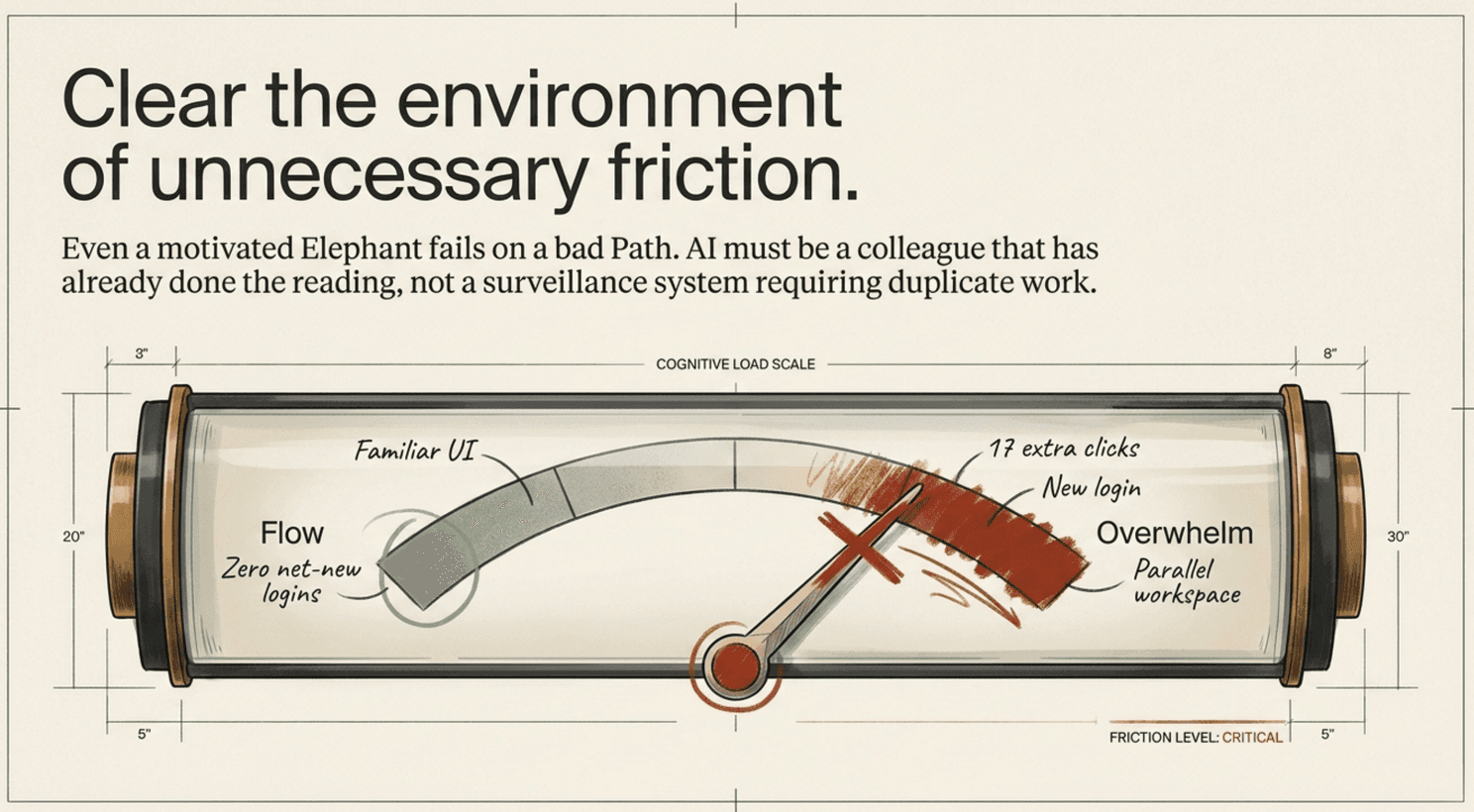

Clearing the Path

Even a motivated Elephant cannot move through a badly designed environment. Enterprise software in this industry has traditionally been sold on features. Marketing teams compete on capability lists. Procurement teams award contracts to whoever checks the most boxes. And then the thing arrives on the desk of an adjuster who is already managing two hundred files and is now being asked to learn a new interface, remember a new password, and produce outputs in a format their attorney panel, their carrier, and their own QA team have never seen before.

The right path is the opposite. The most useful frame I have found is this: think of AI as the smartest, most diligent assistant you have ever had — the one that has already read every document, indexed every fact, drafted the chronology, flagged the inconsistencies, and laid out the strategic options before you walked into the room. It worked through the night without complaint. It does not get tired, does not have a bad day, does not miss the footnote on page forty-seven of the medical records that changes everything.

But — and the "but" is the entire game — it is still an assistant. The judgment is yours. The relationships are yours. The trial instinct, the read on a witness, the credibility call on a particular jury pool — these are the things that distinguish a great defense lawyer from a good one, and no machine will be making them in any timeframe that matters to your career. AI can give you a complete first draft of the case. It cannot decide what kind of case you want to make. It can show you the expected settlement range under five different strategies. It cannot tell you which client relationship to protect when the carrier and the policyholder disagree. The point of the technology, properly understood, is not to replace human judgment but to ensure the human is exercising judgment on a complete picture rather than a fragmentary one.

Designed this way, the path stops feeling like an obstacle course. Outputs look like the status reports, coverage memos, and reserve justifications attorneys already write — except the system now generates them from the work itself. Familiar before new. One shared workspace rather than a parallel one. AI as the colleague that has already done the reading, not the surveillance system waiting to catch someone in an error

The Promise

There is a larger argument for all of this, and it is the one I would leave insurance defense leaders with.

Insurance, at its core, is a promise. You pay your premiums, you manage your risks, and if something terrible happens you will not face it alone. The vast majority of claims professionals, defense attorneys, and carrier executives I have met got into this work because they believe in that promise. Most, asked privately, will admit that the current system is not keeping it as well as it should.

The genuinely painful feature of the present moment is that legitimate claimants — people who were actually hurt, who have real losses, who deserve what they paid for — are being processed through the same slow, adversarial, document-buried system as the people gaming it. The system cannot tell them apart fast enough. The claim mill and the grieving widow get the same response time. That is not right, and it is, more than any individual verdict, what is damaging the industry's standing with the public and its juries.

This is what AI can actually fix. Not by replacing judgment — by accelerating it. By helping an operation separate the files that deserve every resource from the ones that need to be contested hard and early. The legitimate claimant gets a resolution faster. The system abuser gets a fight. That is what a well-functioning claims operation looks like. It is, for the first time, actually buildable.

If you are a managing partner trying to win the Elephant's trust for your AI program, this is the argument worth making. Not efficiency metrics. Not cost reduction. The fulfillment of what this industry was built to do. People will move mountains for meaning. They will drag their feet for efficiency.

Friends or foes? It is still the wrong question. AI is a tool. The organizations that use it to better serve their policyholders, recruit and retain the next generation of talent, and protect the integrity of the system will win the coming decade — and they will win it by a wider margin than most of their competitors yet appreciate. The ones who use it purely to cut costs, without considering the human system around it, will produce worse outcomes, more litigation, and shrinking firms — and they will deserve all three.

You can still choose which one you are going to be. For the moment.

Notes

[1] John P. Kotter and subsequent McKinsey & Company research, widely cited in Journal of Continuing Education in Nursing and elsewhere: roughly 70% of change-management efforts fail to meet their intended goals. See "70% Failure Rate: An Imperative for Better Change Management," PubMed, 2019. https://pubmed.ncbi.nlm.nih.gov/30942888/

[2] Bain & Company, "The 12 Keys to Transformation," 2024: 88% of business transformations fall short of their original ambitions. https://www.bain.com/insights/the-12-keys-to-transformation/

[3] MIT Project NANDA research on enterprise AI deployments, 2025: approximately 5% of corporate AI projects deliver measurable ROI.

[4] McKinsey & Company, "The state of AI in 2025: Agents, innovation, and transformation." High-performing organisations are nearly 3x as likely as peers to have fundamentally redesigned individual workflows around AI; the largest barrier to scaling is now leadership inertia rather than employee resistance. https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai

[5] Boston Consulting Group, "AI Adoption in 2024: 74% of Companies Struggle to Achieve and Scale Value." Approximately 70% of challenges in AI projects stem from people and process, not technical issues. https://www.bcg.com/

[6] Stanford Digital Economy Lab, "The Enterprise AI Playbook: Lessons from 51 Successful Deployments," Pereira, Graylin, and Brynjolfsson, 2026. Successful firms invest as much as $10 in process redesign, reskilling, and organisational transformation for every $1 of tangible technology investment. https://digitaleconomy.stanford.edu/

[7] Sedgwick, "The rise of claim severity and complexity," February 2024. https://www.sedgwick.com/blog/the-rise-of-claim-severity-and-complexity/

[8] Swiss Re Institute, "Litigation costs driving claims inflation – indexing liability loss trends," September 2024. https://www.swissre.com/

[9] Marathon Strategies, "Corporate Verdicts Go Thermonuclear" report, 2025: nuclear verdicts (over $10 million) totaled $31.3 billion in 2024 across 135 cases.

[10] Chip Heath and Dan Heath, Switch: How to Change Things When Change Is Hard (Crown Business, 2010). The Rider/Elephant/Path framing borrows from Jonathan Haidt's earlier elephant-and-rider metaphor in The Happiness Hypothesis.

[11] Insurance Thought Leadership, "Claims Litigation: a Better Outcome?" January 2022. https://insurancethoughtleadership.com/claims-litigation-a-better-outcome

[12] David Autor, Caroline Chin, Anna Salomons, and Bryan Seegmiller, "New Frontiers: The Origins and Content of New Work, 1940–2018," Quarterly Journal of Economics 139, no. 3 (August 2024). https://news.mit.edu/2024/most-work-is-new-work-us-census-data-shows-0401

[13] Joseph Briggs and Sarah Dong, Goldman Sachs Research, "How Will AI Affect the Global Workforce?" August 2025. https://www.goldmansachs.com/insights/articles/how-will-ai-affect-the-global-workforce

[14] U.S. Bureau of Labor Statistics projections cited by RSM US, "Skills gap in insurance industry's aging workforce," 2023. https://rsmus.com/insights/industries/insurance/skills-gap-in-insurance-industrys-aging-workforce-is-a-growing-concern.html

[15] Jonus Group, "Navigating the Talent Shortage in the Insurance Industry," October 2025. https://www.jonusgroup.com/

[16] Claims and Litigation Management Alliance, Defense Counsel Study and Litigation Management Task Force survey, October 2025: 90% of defense firms describe recruitment as harder than five years ago; 60% are turning down work due to capacity. https://www.theclm.org/Magazine/articles/overwhelmed-and-understaffed/3332

[17] PwC, "On the front lines: How insurers can win the war for talent." https://www.pwc.com/us/en/industries/financial-services/library/insurance-war-for-talent.html