Future of Claims

What the Defense Bar Can Learn About How Data Changes An Industry

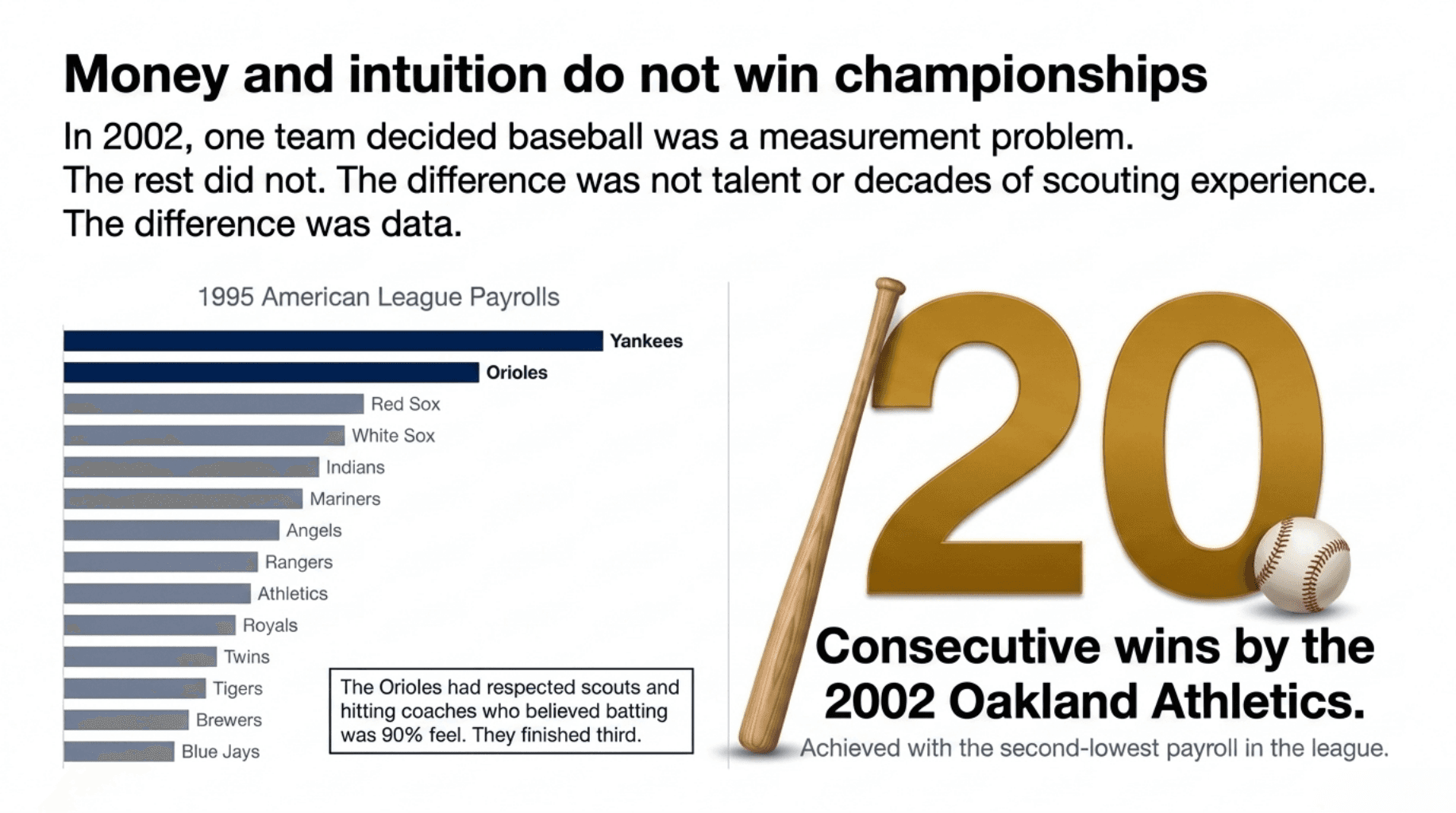

The 1995 Baltimore Orioles spent more on payroll than any team in the American League except the Yankees and Red Sox. Their general manager, a former minor-league catcher named Roland Hemond, was widely respected. Their scouts had decades of experience. Their hitting coach told a young reporter that batting was "ten percent science and ninety percent feel." The Orioles finished third in their division.

Moneyball is the data story that everyone knows

Seven years later, the Oakland Athletics, with the second-lowest payroll in the league, won twenty consecutive games and made the playoffs for the fourth straight year. The difference was not money, talent, or experience. The difference was that one team had decided baseball was a measurement problem and the other had not.

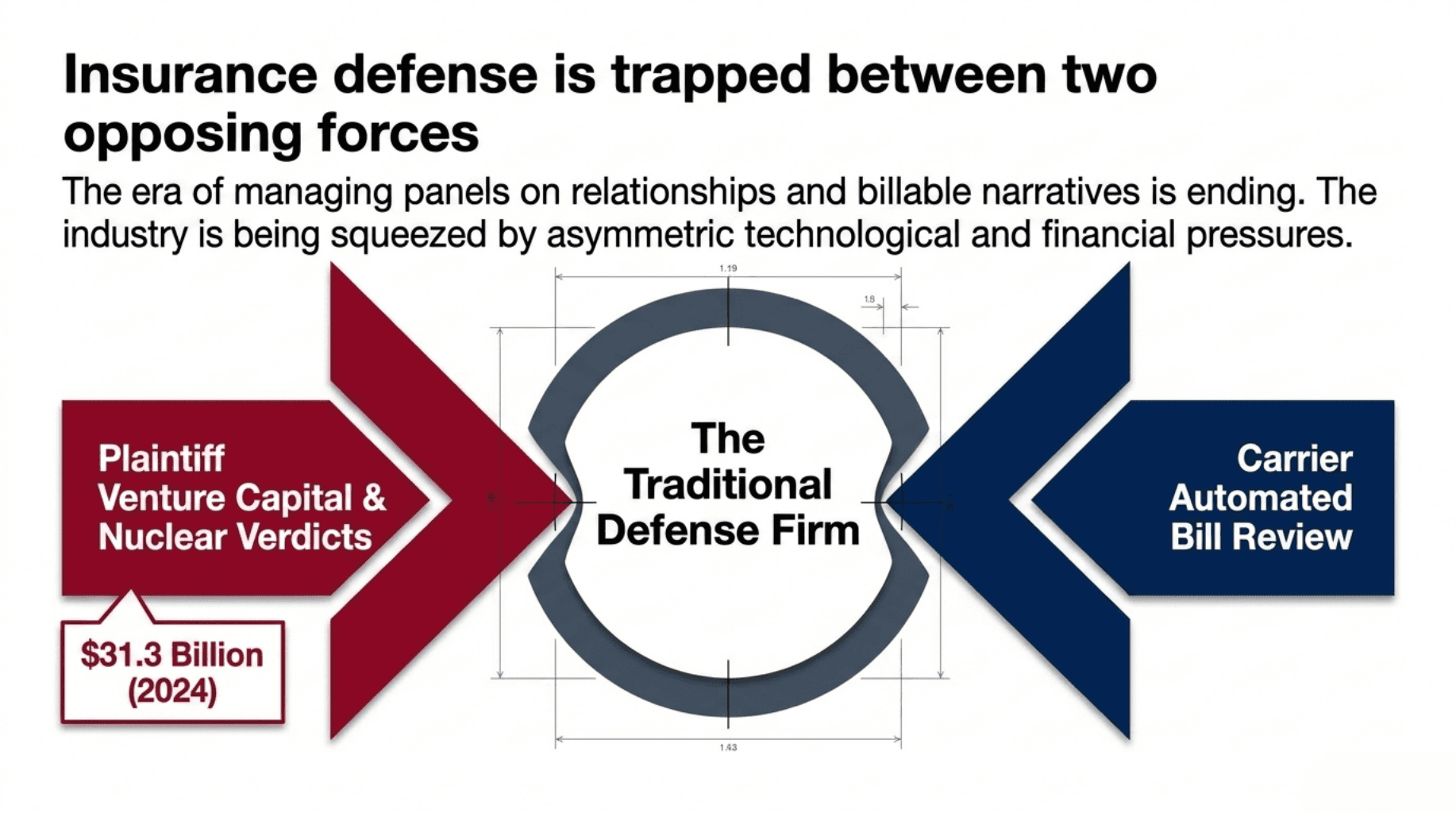

Insurance defense is now somewhere between those two seasons. The plaintiff bar has discovered venture capital, nuclear verdicts climbed to $31.3 billion in 2024,[1] and carriers are running automated bill review against panels they used to manage on relationships. The pincer movement squeezing defense firms has been covered in earlier issues of this newsletter, as has the eighty-five percent of total claim cost that sits in indemnity rather than in legal spend. What this essay is about is different. It is about the pattern itself.

Insurance defense is in the midst of a major squeeze

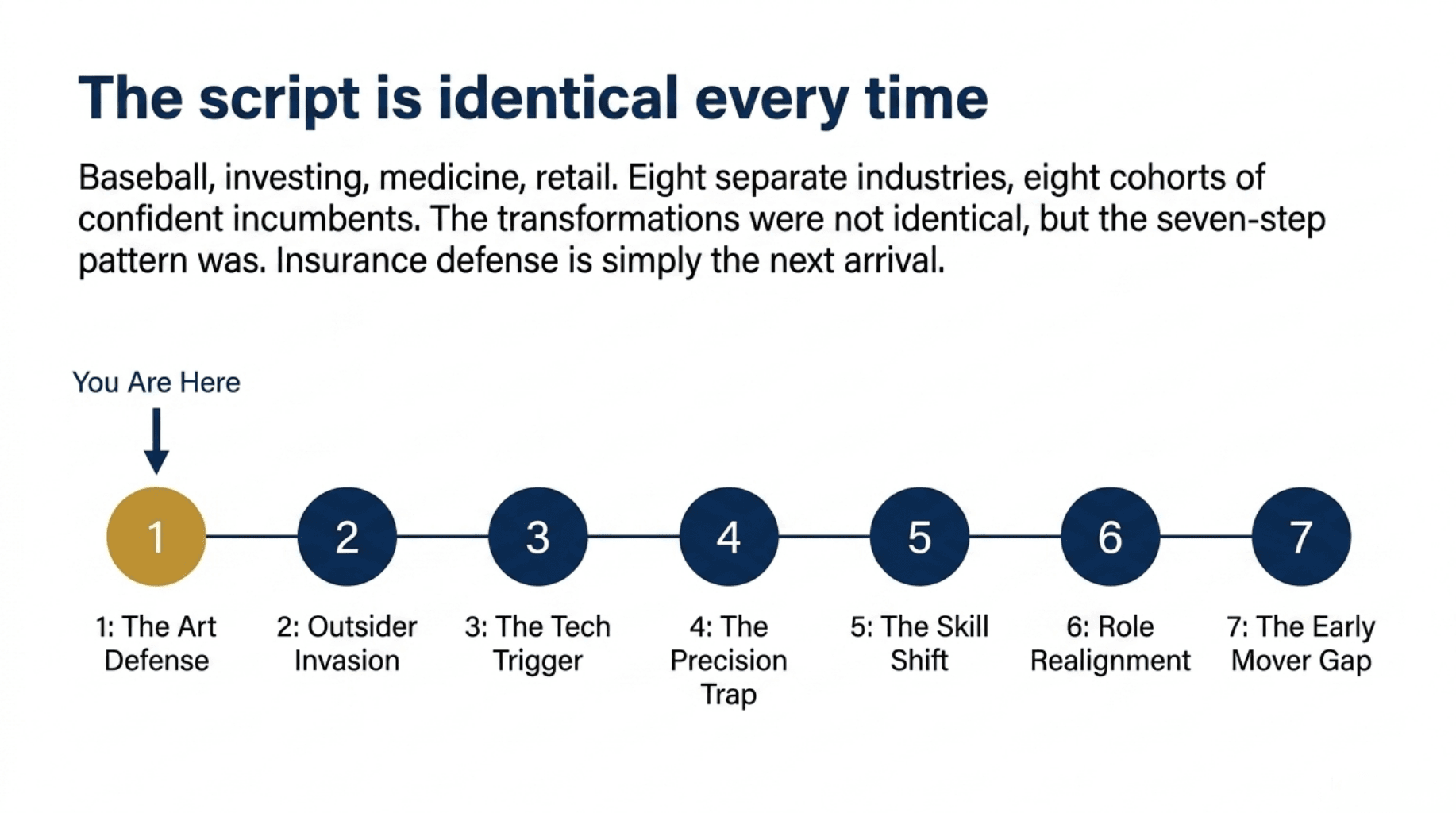

The same data-driven transformation has now played out in baseball, basketball, investing, medicine, retail, manufacturing, media, and advertising. Eight separate industries, eight separate cohorts of confident incumbents. The transformations were not identical, but the script was. Seven things happen, in roughly the same order, every time. Insurance defense is not the first industry to walk through this door, and the previous eight have left useful instructions.

The same 7 things happen every time

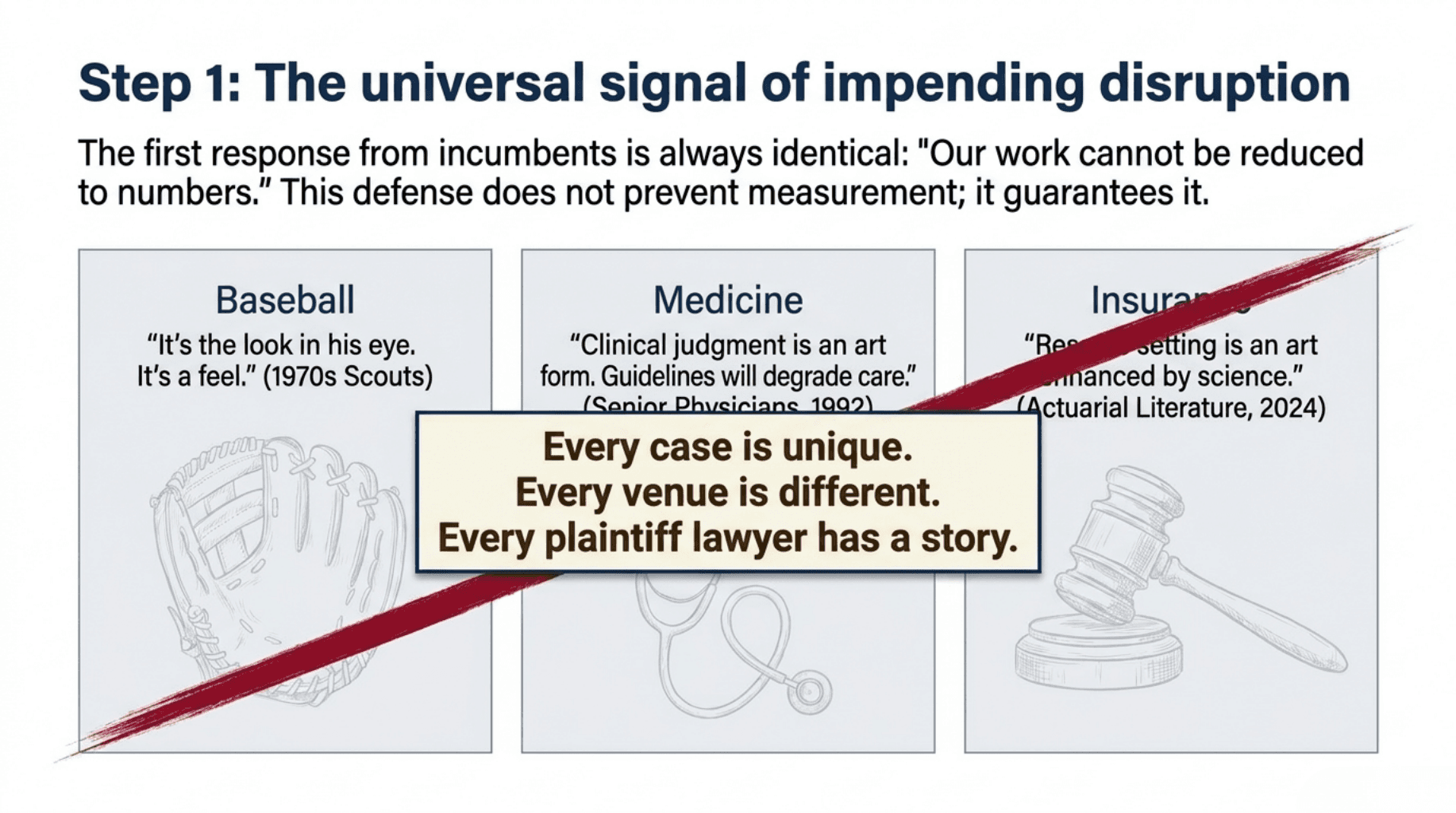

1. The Incumbents Insist Their Work Is More Art Than Science

In every case, the first response from the people inside the industry is the same. The work, they explain, cannot be reduced to numbers. It depends on feel, judgment, and the kind of intuition that only comes from years in the chair.

Baseball scouts spent the 1970s arguing that statistics could not capture what made a hitter great. The five tools, the look in his eye, the way he carried himself in the on-deck circle. None of it was on the back of a baseball card. Bill James spent two decades pointing out that on-base percentage predicted runs and batting average did not, and was largely ignored.

Senior physicians, in the early years of evidence-based medicine, used almost identical language. Clinical judgment, they said, was an art form developed over decades. Cookbook medicine, by which they meant guidelines built from randomized trials, would degrade care.[2] Reserve setting in insurance is, even today, described in the actuarial literature as "art enhanced by science."[3] That phrasing is generous. It is mostly art.

The defense bar's version of this argument should be familiar. Every case is unique. Every venue is different. Every plaintiff lawyer has a story. The judgment of a senior litigator about whether to settle or try, what to reserve, which motion to file first, is the product of thirty years in courtrooms and cannot be reduced to a model. Each of these statements is true. Each of them was also true of pitching, of internal medicine, and of stock-picking.

The "art not science" defense is the universal first response of an industry about to be measured. It is also, in retrospect, the most reliable signal that the measurement is about to happen anyway.

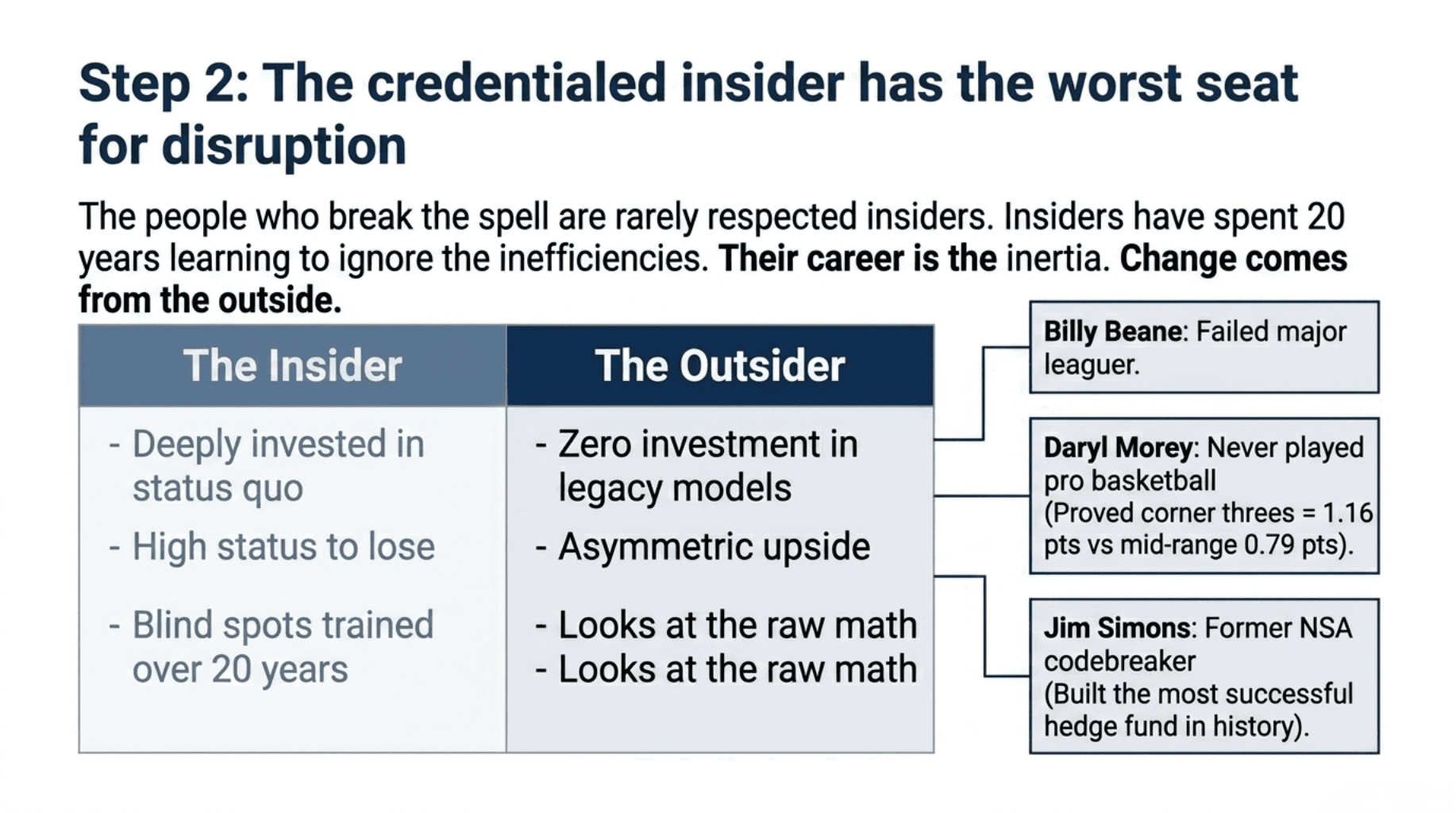

2. The Change Comes From Outsiders, Not From the Best Practitioners

The next thing that happens, with striking consistency, is that the people who break the spell are not the most credentialed insiders. They are outsiders, and that is not an accident.

Billy Beane was a failed major leaguer who had been told his whole career that he had the body of a Hall of Famer and the swing of a journeyman, which turned out to be exactly the right preparation for distrusting scout judgment. Daryl Morey, who calculated that mid-range jumpers were worth 0.79 points per attempt against 1.16 for corner threes,[4] had never played professional basketball. Jim Simons, who built the most successful hedge fund in history, was a former NSA codebreaker and Stony Brook math department chair who explicitly refused to hire MBAs.[5]

Its hard to see the system is broken when you are inside the system

The pattern is not a coincidence. Outsiders have three structural advantages the credentialed insider lacks. They are not personally invested in the existing way of working, which means they do not have to admit they were wrong about it. They have less status to lose if they fail and more to gain if they succeed, which changes the expected value of the bet. And, most importantly, they have not spent twenty years learning to see the industry the way the industry sees itself, which means they can still notice things the insiders have trained themselves to ignore.

This is the uncomfortable implication for the defense bar. The people who will rewire how defense work gets done are unlikely to be the most respected partners at the most respected firms. They will be operators, technologists, and insurance executives. Some of them will come from the carrier side. Some of them will come from outside the industry altogether. The credentialed insider will have the worst seat for the disruption, because the credentialed insider's career is the inertia.

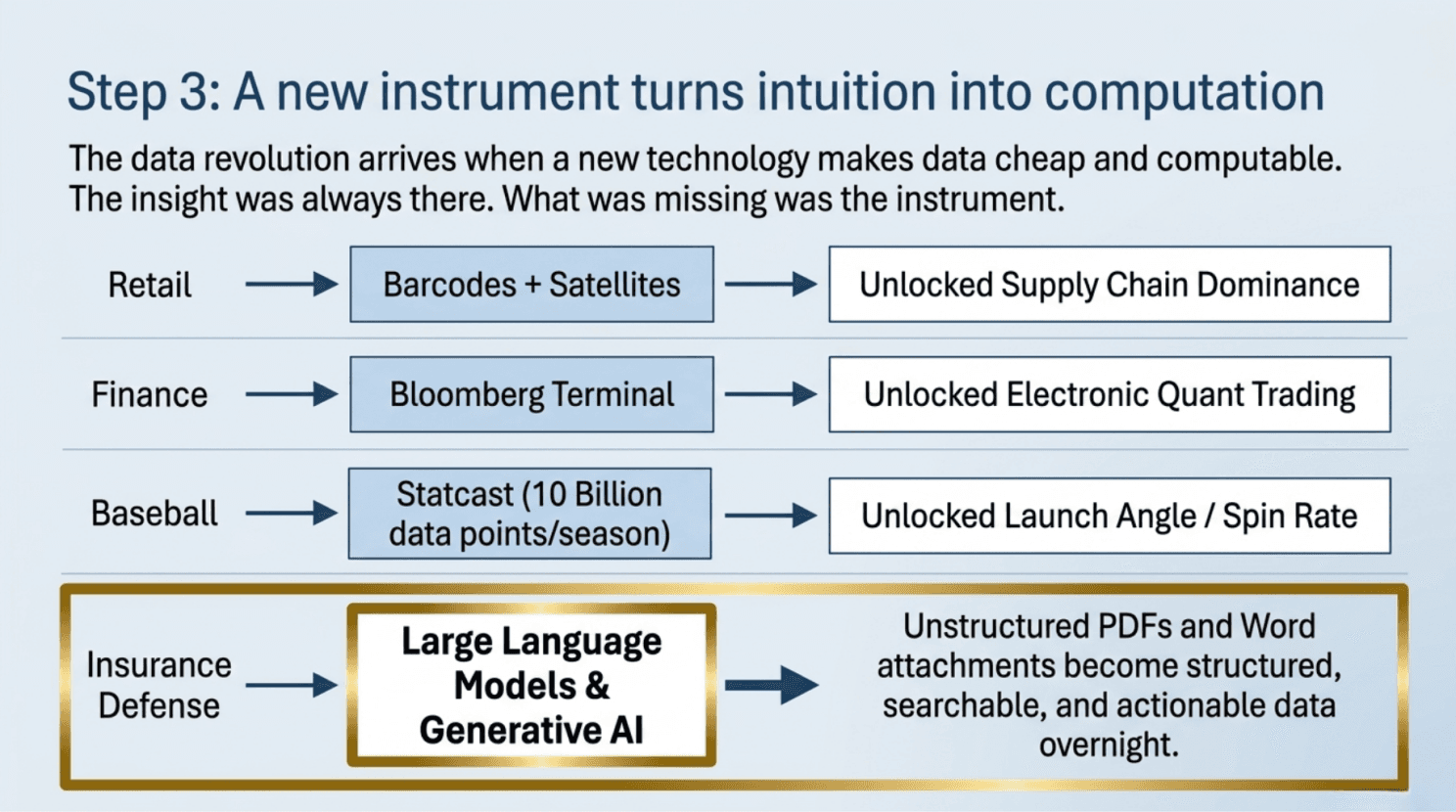

3. There Is Usually a Technology Trigger That Made the Data Possible

The data revolution rarely arrives because someone decides to be more rigorous. It arrives because a new technology suddenly makes data cheap, available, or computable for the first time. The insight was almost always there. What was missing was the instrument.

Baseball's transformation was not really Bill James. It was video. Video review, then pitch-tracking cameras, then high-frequency sensors that could capture spin rate and launch angle on every pitch. The 2002 Athletics had access to data that the 1985 Athletics, with the same intellectual framework, simply could not have collected. Statcast, the league's tracking system, now captures more than ten billion data points per season.[6]

The real impact of AI is how it unlocks the data

The same is true of finance. The Bloomberg Terminal arrived on Wall Street trading floors in the early 1980s and made real-time pricing data available to anyone willing to pay for it. Electronic trading then turned that data into action. Quantitative funds existed in concept before either; they became viable in practice because the cost of inputs collapsed.

Retail's transformation came from the barcode. Walmart's 1.7% distribution cost against Kmart's 3.5% and Sears' 5%[7] was the dividend of having installed point-of-sale scanners across thousands of stores and connected them to the largest private satellite network in America. Blockbuster lost to Netflix because the internet made it possible to know what every customer was watching, on every device, at every moment, which created a recommendation engine no retail footprint could compete with.

The technology trigger for insurance defense is the one we are sitting in the middle of. Until very recently, the data needed to govern litigated claims was scattered across PDF discovery files, attorney status reports in Word attachments, billing entries in LEDES files that nobody read, and the cognitive load of an adjuster trying to track three hundred matters at once. Large language models have changed this. The unstructured text in a claim file is now structured, searchable, and analyzable in a way it was not eighteen months ago. The instrument has arrived. The data has been there all along.

4. They Are Measuring Something. It Is Not the Thing That Matters

This is the most useful part of the pattern, because it offers a diagnostic the reader can apply to their own industry tonight.

The incumbents that ultimately lose did not lose because they failed to measure anything. They lost because they measured the wrong things, with great precision, for a long time. Detroit measured unit cost while Toyota measured cycle time and defect rate. Sears measured catalog circulation while Walmart measured turns per square foot. Blockbuster measured store throughput and late fees while Netflix measured churn and lifetime viewer value. Madison Avenue measured creative awards while Google measured cost per conversion.

You can't effectively manage what you don't measure

In every case, the incumbent metric was real. It was tracked. It was discussed in meetings. It was used to set bonuses. And it had, sometime in the previous decade, stopped being the metric that determined who won.

The same trap is set for the casualty insurance industry. As argued in previous issues, approximately eighty-five percent of total claim cost in litigated matters sits in indemnity. The remaining fifteen percent sits in allocated loss adjustment expense, where defense fees live. Carriers have spent ten years industrializing the measurement of the fifteen-percent line through automated bill review, panel scorecards, and tightened guidelines. The eighty-five-percent line, where the actual money is, remains governed by adjuster intuition.

This is the most precisely measured wrong number in the casualty business. It is the Detroit unit-cost equivalent, the Blockbuster late-fee equivalent. It is the metric the industry talks about because it is the metric the industry can talk about, not because it is the metric that determines outcomes.

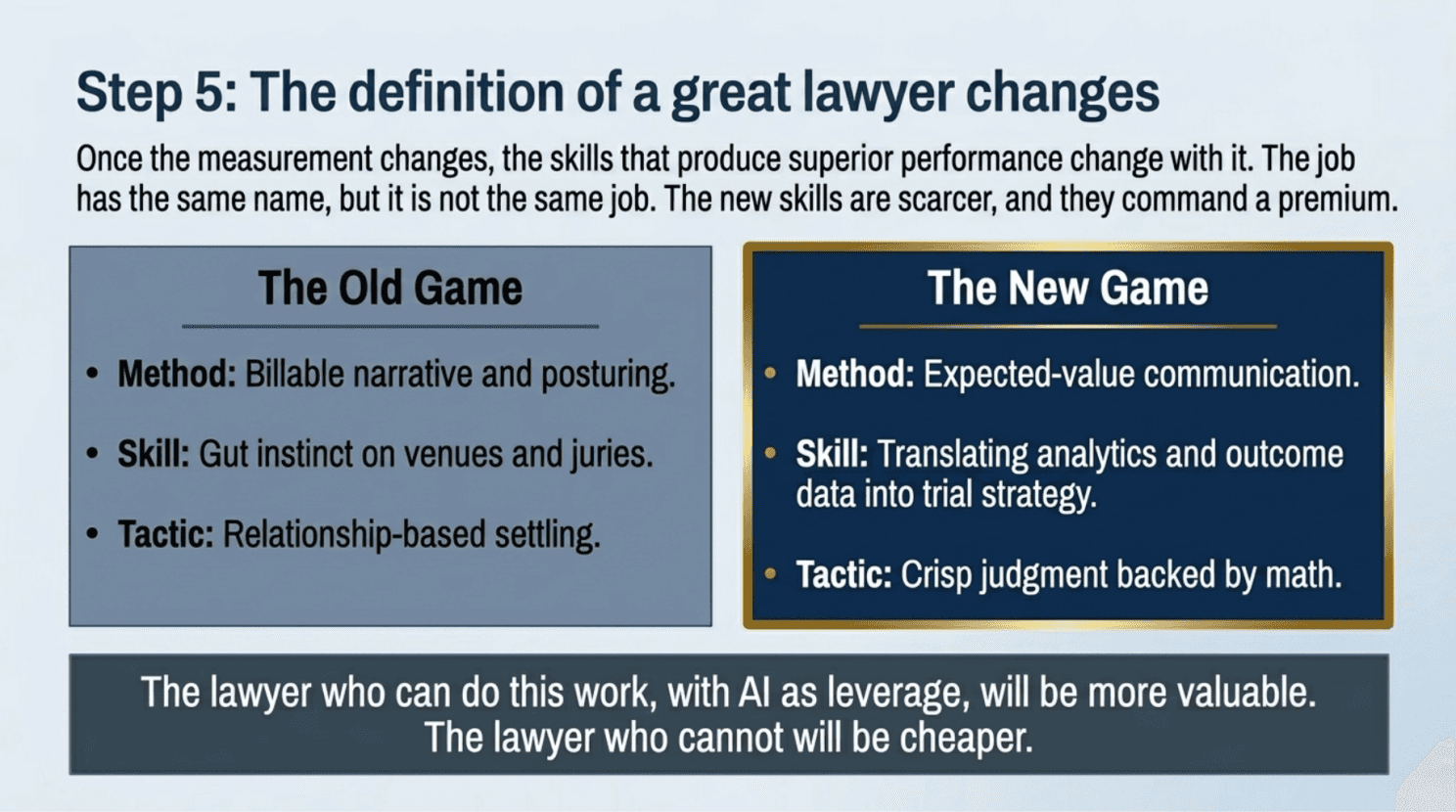

5. The Skills That Matter Shift, and the New Skills Pay More

Once the measurement changes, the skills that produce superior performance change with it. The professionals who get rewarded in the new game are not the same ones who got rewarded in the old one.

The major league hitter of 1985 was a contact hitter who could hit the gap. The major league hitter of 2025 is an analyst who studies the spin rate of his next opposing pitcher and adjusts his swing path to optimize launch angle. The job has the same name. It is not the same job. The hitters who can do the new job are paid extraordinarily; the hitters who cannot are out of the league. The aggregate compensation of major leaguers has gone up, not down, because the new skills are scarcer and the cost of not having them is higher.

Who is going to win the next 10 years?

The same has happened on Wall Street, in a different direction. The stock-picker with a Bloomberg terminal and a thesis has been replaced, at the top of the income distribution, by the quant who can model market microstructure or the risk manager who can read a portfolio. In medicine, the radiologist who can supervise an AI pipeline reads twice as many studies per shift as the one who cannot. The new skill commands a premium because it is the actual constraint on the business.

For defense litigators, the question is which skills will earn the premium in the new game. The answer is not difficult to guess. Crisp judgment about which cases to fight and which to settle, when supported by real outcome data, becomes far more valuable than it was when nobody could check the call. The ability to translate analytics into trial strategy, to read venue data the way the best lawyers used to read juries, to communicate to a carrier client in the language of expected value rather than billable narrative, all of these will pay. The lawyer who can do this work, with AI as the leverage, will be more valuable than the equivalent partner was a generation ago. The lawyer who cannot will be cheaper.

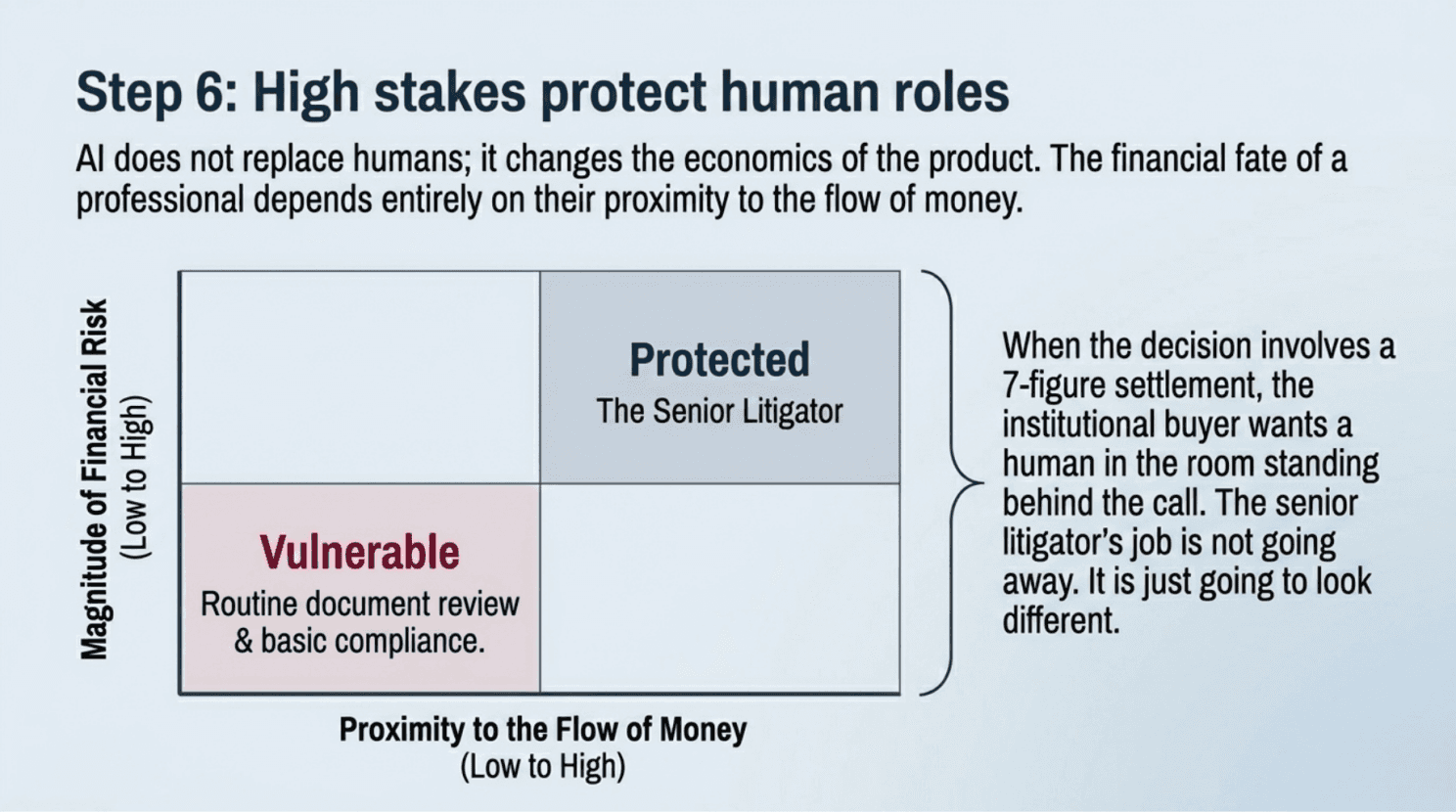

6. Humans Are Not Replaced. Their Role Changes, and the Economics Depend on the Product

This is the most misunderstood part of the pattern, and the place where the conventional AI conversation tends to get it wrong.

Baseball still has scouts. Hospitals still have radiologists. Wall Street still has analysts. Detroit still builds cars. In every industry that has been through this, the people did not disappear. The role changed. The scout went from primary decision-maker to model validator. The radiologist went from interpreter of every scan to supervisor of an algorithmic pipeline. The analyst went from stock-picker to risk manager. The work continued. The work was different.

Defense attorneys are in a safe and needed spot

What changed dramatically, and unevenly, was the number of those roles and what they paid. And here is the part the standard narrative misses. The financial fortunes of the humans in any given industry have very little to do with the nature of the technology and very much to do with the nature of the product being sold.

Three structural variables explain most of it.

The first is whether the product itself can change. In industries where technology just lets you do the same thing more cheaply, the number of jobs typically falls. The cassette tape did not enable a new kind of music; it just made distribution cheaper, and the people who used to press records lost their jobs. But in industries where technology enables a better product, demand often grows and jobs grow with it. Accountants did not disappear when spreadsheets arrived; the spreadsheet made accountants more useful, made more kinds of analysis possible, and the profession expanded. Insurance defense looks more like accounting than like cassette manufacturing. Better-defended cases mean more contested cases, more litigated claims, and more demand for the lawyers who can do the new work well.

The second is the structural protection of the role. Baseball players have a union. Doctors have licensure. Engineers have professional certifications. These structures do not stop transformation, but they slow it and shape who captures the gains. Lawyers, of course, have one of the strongest licensure regimes in the economy. The transformation of legal work will happen within the structure of the bar, not around it.

The third, and the most important for defense lawyers to internalize, is the proximity of the role to the flow of money and the magnitude of the decision. When the decisions involve large sums and meaningful risk, the institutional buyer wants a human in the room, even when the model is excellent. The carrier client paying a seven-figure settlement wants a senior partner explaining, confirming, and standing behind the call. The hospital wants a radiologist signing the report, not the algorithm. The hedge fund LP wants a portfolio manager on the phone. The further the role sits from those high-stakes decisions, the more vulnerable it is. The closer it sits, the more protected. Defense litigators sit very close to those decisions. The senior litigator's role is not going away. The senior litigator's job will look different.

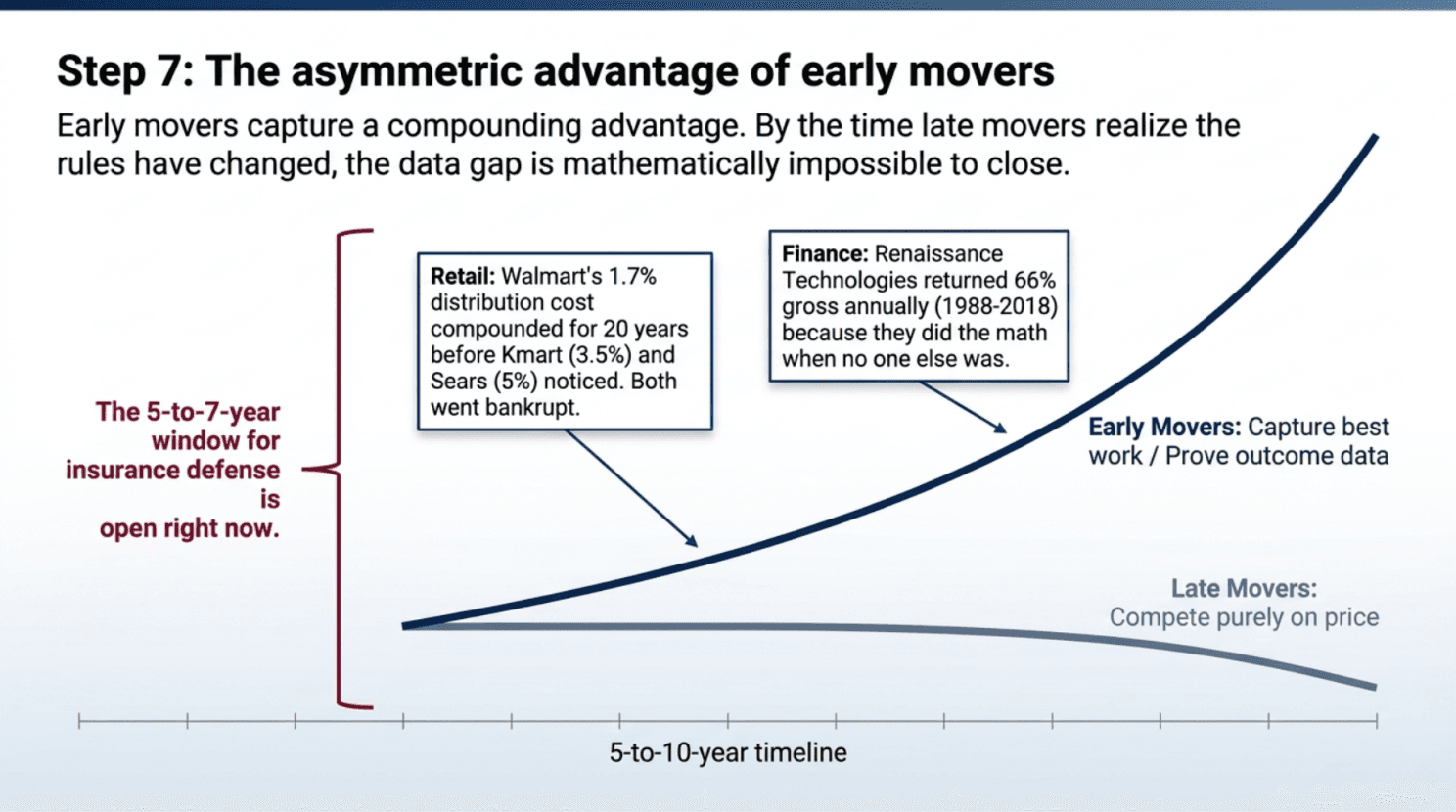

7. The Market Shifts, and the Firms That Move First Pull Away Permanently

The final thing that happens, in every industry, is that the early movers capture an asymmetric advantage that the late movers can never make up.

Walmart's distribution-cost advantage over Sears and Kmart was not a single year's competitive edge. It compounded annually for twenty years before either incumbent caught on. By the time Sears and Kmart understood what was happening, Walmart had built a national supply chain, a satellite network, and a database the others could not buy and could not replicate quickly enough. Kmart filed for bankruptcy in 2002. Sears in 2018.

Netflix's data lead on Blockbuster was an eighteen-month head start on a recommendation engine. Eighteen months turned into the entire customer base. Renaissance Technologies' first decade of returns was when the math was easiest, because nobody else was doing it. The Medallion Fund's edge has narrowed every year since, but the wealth accumulated in those early years is what funded everything that came after.[5]

Can you create a gap to the competition that others can't overcome

This is the part of the pattern that most directly addresses the question of timing. The window for asymmetric returns in insurance defense is open now, and history suggests it will close within five to seven years. The firms that build a real outcome-data capability in that window, that develop the analytics fluency, that can present credible performance data to carrier clients, that build the new skills internally, will compete for the best work for the next generation. The firms that wait will compete on price for what is left.

Once every carrier in a market can run analytics on counsel performance, the question is no longer whether to adopt. The question is what proof you have that your firm is worth selecting. The firms that have been collecting that proof for three years will have it. The firms that started last quarter will not.

What History Suggests

This script has now run eight times. The names of the industries are different, the technologies are different, the players are different, but the structure is identical. Insurance defense is in the early innings of the same game.

The art-not-science defense will be made. The outsiders will arrive. The technology is here. The carriers are already measuring the wrong number, with great precision. The skills that earn the premium will shift. The role of the senior litigator will change but not disappear, because the role sits too close to the money to be automated away. And the firms that move first will pull away from the firms that wait, in a gap that compounds for a decade before the late movers notice it has happened.

The window is open, jump through before it closes

The Yankees still have the largest payroll in baseball. They have not won a World Series since 2009.

Future of Claims Academy

The Future of Claims Academy launched in late May with the first of eleven modules. That session, "How AI Is Changing the Economics of Litigation Defense" with Brian Kennel, is the practical version of the argument this essay makes in the abstract. Ten modules remain, each featuring a practitioner who has been in the room while these decisions get made. The session replay, the full schedule, and registration are at OraClaim.com/Academy. Free to attend.

Notes

[1] TransRe, Social Inflation: Examining the Costs to the Insurance Industry (Nov 2025); Marathon Strategies, Corporate Verdicts Go Thermonuclear (May 2025). https://www.transre.com/wp-content/uploads/2025/11/Social-Inflation-Overview-2025.pdf

[2] Gordon Guyatt et al., "Evidence-Based Medicine: A New Approach to Teaching the Practice of Medicine," JAMA 268, no. 17 (1992). The "cookbook medicine" critique was the predominant response from senior clinicians for roughly a decade after publication.

[3] WTW, "Setting Claim Reserves: Art or Science?" (June 2024). https://www.wtwco.com/en-us/insights/2024/06/setting-claim-reserves-art-or-science

[4] Average points per shot type, 1998 to 2018, from The Hoya, "How Daryl Morey Changed the NBA" (2021): shots at the rim ~1.2; corner threes ~1.16; above-the-break threes ~1.05; mid-range ~0.79.

[5] Gregory Zuckerman, The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution (Portfolio, 2019). Renaissance's Medallion Fund returned approximately 66% gross annually from 1988 through 2018.

[6] Major League Baseball Advanced Media; Samford University Center for Sports Analytics. https://www.samford.edu/sports-analytics/fans/2018/The-Truth-about-Sabermetrics

[7] IndustryWeek, "How Sharing Data Drives Supply Chain Innovation." https://www.industryweek.com/supply-chain/supplier-relationships/article/21960963/how-sharing-data-drives-supply-chain-innovation