Introduction

Defense teams make the same procurement mistake repeatedly: they evaluate claims data analytics solutions on licensing cost alone, sign the contract, and discover the real costs buried in implementation hours, attorney time on document review, and fragmented data systems months later — when claim volumes are already overwhelming their capacity.

That calculation error is expensive. Investors have committed more than $250M to AI startups serving plaintiff-side lawyers, and defense experts have been direct: defendants and insurers risk falling behind the plaintiff's bar on litigation AI. Staying on manual processes while adversaries accelerate is a compounding disadvantage — one that grows with every claim cycle.

This article breaks down the true total cost of ownership (TCO) for purpose-built AI claims analytics platforms versus manual or generic analytics approaches — covering acquisition, operational, and personnel costs alongside the hidden variables that sticker-price comparisons routinely miss.

Key Takeaways

- Both approaches carry real costs, but the cheaper-looking option is rarely cheaper over time.

- True TCO spans acquisition, implementation, personnel, compliance, integration, and poor-outcome financial impact.

- Manual and generic tools hide costs in document review hours, data silos, and missed case patterns.

- Purpose-built platforms require upfront investment but reduce per-claim labor costs and scale without proportional headcount increases.

- The right choice depends on claim volume, team size, and whether you're optimizing for budget optics or long-term margin health.

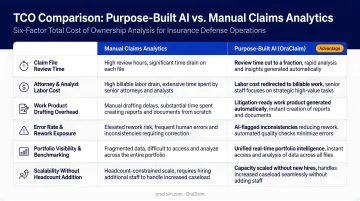

Purpose-Built AI vs. Manual/Generic: Quick Comparison

The six factors below capture where purpose-built AI and manual/generic approaches diverge most sharply on total cost of ownership.

| Factor | Purpose-Built AI Platform | Manual/Generic Approach |

|---|---|---|

| Upfront Cost | Defined licensing/subscription fee | Appears low-cost; internal resourcing costs emerge quickly |

| Implementation | Pre-configured for claims workflows | Heavy configuration, training, and often custom development |

| Time-to-Value | Compressed — built for claims data structures | Delayed — generic tools need significant adaptation |

| Scalability | Adds capacity without proportional headcount | Headcount scales linearly with claim volume |

| Outcome Quality | Systematic pattern identification, benchmarking | Inconsistent review; human error affects case strategy |

| Compliance/Security | Built for legal and insurance data sensitivity | Generic tools not designed for privilege or regulatory requirements |

The gap widens at scale — the sections below break down each factor with real cost implications.

What Is a Purpose-Built Claims Data Analytics Platform?

A purpose-built claims analytics platform is software designed from the ground up for the specific data types, workflows, and decision-support needs of defense attorneys, claims managers, and insurance carriers — not a general-purpose BI tool adapted for legal use.

Core Capabilities

The distinction matters operationally. A purpose-built platform delivers:

- Automated document ingestion and review — processes claim files, medical records, demand packages, statements, and expert reports without manual sorting

- Structured case benchmarking — compares open matters against historical outcomes across jurisdiction, plaintiff counsel, judge, and fact pattern

- Pattern identification — surfaces exposure drivers, causation gaps, treatment inconsistencies, and contradictions before they become reserve surprises

- Portfolio-level intelligence — connects claim data to financial metrics so claims executives and managing partners see margin, reserves, and loss assessment in one view

Because these platforms eliminate non-billable document review and surface critical facts automatically, defense teams handle larger claim volumes without proportional increases in headcount. Thomson Reuters research found that AI could save professionals up to 12 hours per week within five years, a figure that translates directly into labor cost savings in high-volume defense operations.

Where It Fits in the Defense Workflow

Purpose-built analytics delivers the clearest advantage in:

- Insurance carriers running high-volume claims portfolios that need systematic reserve discipline and panel-firm benchmarking

- Defense law firms managing complex litigation across multiple lines of coverage, where institutional knowledge typically lives in people's heads rather than structured systems

- TPAs and self-insured corporations handling claims across multiple lines and needing unified portfolio visibility

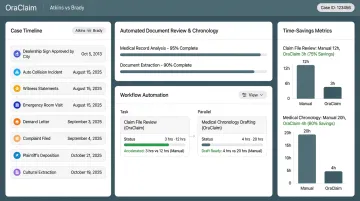

OraClaim's claims intelligence platform was built specifically for this workflow. It delivers litigation-ready work product automatically, structures and benchmarks past cases to surface patterns and anticipate outcomes, and connects operational data with revenue and cost insights so defense teams can see efficiency, margin, and portfolio health in a single view. The platform cuts total claim-file review time by half or more and reduces manual benchmarking effort by over 80%.

What Is a Manual or Generic Analytics Approach?

Manual or generic analytics describes the combination of spreadsheet tracking, basic reporting tools, and general-purpose BI software that many defense organizations currently use to manage claim data and inform case strategy. This typically includes disconnected document management systems, email threads, and siloed databases that don't share data.

The Operational Burden

The real cost of this model is labor. Attorneys and claims professionals are manually reviewing unstructured documents, building ad hoc reports, and carrying institutional knowledge in their heads rather than in a structured system. That creates two distinct risks:

- Every new claim requires human review time that doesn't shrink as volume grows

- When an experienced adjuster or senior attorney leaves, their benchmarking knowledge leaves with them

Data fragmentation compounds both problems. When claim history, outcome data, and financial metrics live in separate systems, organizations lose the ability to benchmark cases systematically or measure portfolio health. Decisions that should rest on integrated data end up made on instinct.

ACORD's 2025 Insurance Digital Maturity Study found that only 25% of the world's largest insurance carriers had truly digitalized the value chain — meaning the majority are still operating with significant manual process exposure.

Where Manual Approaches Persist

Manual and generic approaches work for:

- Smaller defense practices with genuinely low claim volumes

- Organizations in early stages of digital adoption

- Teams using a phased rollout before committing to a dedicated platform

Each of those conditions is temporary or bounded. Once claim volume climbs, the cost ceiling scales poorly. Attorney and adjuster hours consumed by tasks a platform would automate grow directly with claim count — and that hidden TCO exposure adds up fast. Before deciding to stay manual, organizations should model the 3-year cost of that choice explicitly.

How to Calculate TCO for Claims Data Analytics Solutions

The standard TCO formula — Acquisition Costs + [(Operational Costs + Resource Costs) × Years of Ownership] — applies here, but each category has claims-specific line items that are routinely overlooked during vendor evaluation.

Acquisition Costs

Include every cost to reach active use:

- Platform licensing or subscription fee

- Implementation and onboarding

- Initial training for attorneys, adjusters, and claims staff

- Data migration from legacy systems

- Integration development to connect with existing practice management or document management platforms (Clio, iManage, NetDocuments, and similar)

Purpose-built platforms with pre-built integrations compress this category significantly. Generic tools often require custom development to connect with claims-specific data structures — a cost that doesn't appear in the initial quote.

Operational Costs

Ongoing costs that accumulate across the ownership period:

- Annual subscription or maintenance fees

- Security patching and compliance updates

- Data governance and audit trail requirements specific to legal and insurance data

- Storage and usage scaling as claim volume grows

- IT resources required to maintain integrations with evolving practice management systems

For generic BI tools not built for legal data sensitivity, compliance becomes an additional line item. Tools purpose-built for the defense ecosystem treat encryption, authentication, and privilege preservation as baseline requirements — already baked into the platform, not sold as upgrades.

Personnel and Resource Costs

This is the most underestimated category. Calculate the fully loaded cost of every hour spent on tasks an analytics platform should handle: document review, report generation, case benchmarking, and portfolio reporting.

Start with the hourly rates:

- The BLS reports the median annual wage for claims adjusters at $76,790, with a median hourly rate of $36.92

- NALP reports the median first-year associate base salary at $200,000 — before benefits, overhead, and partner supervision time

- Multiply those rates by hours consumed annually in manual document review and benchmarking

OraClaim automates the specific tasks that consume this time. Claim file review that traditionally takes hours completes in minutes. Medical chronology drafting drops from 15–60+ hours per file to under 60 minutes for a first draft. Deposition prep drops from 4–20 hours per witness to minutes.

At scale across a full claims portfolio, the labor cost differential between a manual model and an AI-assisted model typically exceeds the platform subscription cost within the first year.

The Outcome Cost Variable

General TCO frameworks miss this entirely. Poor case benchmarking, inconsistent document review, and missed exposure patterns all affect settlement values, reserve accuracy, and litigation costs.

The financial stakes are real: Fitch reported that other liability-occurrence lines had reserve deficiencies averaging 7% of segment earned premiums from 2018 to 2022. Those deficiencies trace directly to the kind of inconsistent benchmarking and missed exposure signals that better analytics prevent. Assign even a rough estimate to this variable in your TCO model. Ignoring it systematically understates the true cost of manual or generic approaches.

Which Approach Has Lower TCO? Situational Recommendations

The decision depends on five factors: claim volume, team size, integration complexity, current margin pressure, and the degree to which plaintiff-side technology adoption is already creating competitive disadvantage.

Choose a purpose-built AI platform if:

- Your organization handles significant claim volumes and is hitting capacity constraints without wanting to add headcount

- You need to benchmark cases systematically and your current process relies on institutional knowledge held by individuals

- Plaintiff-side AI tools are already accelerating against you — investors have committed more than $250M to that side of the market, and that gap widens each year

- Your current manual benchmarking, report generation, and document review costs are measurable and significant when multiplied across annual claim volume

Choose a manual or phased approach if:

- Claim volumes are genuinely low and the labor cost of manual review is proportionately small

- You're in a proof-of-concept phase before committing to a platform

- Integration complexity with legacy systems requires a staged rollout

Either way, model the 3-year TCO of staying manual before committing to that path. Non-billable review hours and fragmented data carry costs that don't show up in a single claim — but multiply fast across a full portfolio. That number usually changes the conversation.

Conclusion

TCO for claims data analytics is a whole-operation calculation — one that extends well beyond subscription fees. The full picture includes:

- Attorney and adjuster time consumed by manual review

- Outcome variance from unstructured, incomplete claim intelligence

- Compliance and privilege exposure from fragmented data workflows

- The compounding cost of falling behind as plaintiff-side technology accelerates

Organizations that run the full TCO math — accounting for personnel costs, outcome variables, and the cost of scale — routinely find that purpose-built analytics platforms are cheaper than the manual status quo. The difference shows up in loss adjustment expense, matter-level margins, and settlement outcomes. That's where the real comparison lives.

Frequently Asked Questions

Is a higher or lower total cost of ownership better when comparing claims data analytics solutions?

Lower TCO is generally preferable, but the goal is accurate measurement. A solution that appears lower-cost upfront often carries higher hidden costs in personnel time, poor outcomes, and lost scalability. The best value is the solution with the lowest true TCO relative to the outcomes it delivers.

How is total cost of ownership calculated when comparing claims data analytics solutions?

TCO equals acquisition costs (licensing, implementation, training, integration) plus the annual sum of operational and personnel costs, multiplied by years of ownership. For claims analytics, the calculation should also account for the financial impact of claim outcomes influenced by analytics quality — including reserve accuracy and settlement exposure.

What are the hidden costs of relying on manual claims data review?

The primary hidden costs are non-billable attorney and adjuster hours consumed by document review, data fragmentation that prevents systematic benchmarking, key-person dependency when institutional knowledge isn't structured, and the compounding cost of case decisions made without access to integrated portfolio data.

How long does it typically take to see ROI from a purpose-built claims analytics platform?

ROI timelines vary by organization size and claim volume, but purpose-built platforms reduce document review time and surface usable insight early in adoption. When evaluating vendors, request specific time-to-value benchmarks and compare them against your current per-claim labor cost.

Does a purpose-built claims analytics platform always cost more upfront than a generic solution?

Not necessarily. Purpose-built platforms carry defined licensing costs, but generic or manual alternatives accrue costs in configuration, customization, integration development, and ongoing maintenance that frequently exceed the cost of a purpose-built solution within the first 12–18 months.

How does AI specifically reduce TCO in claims data analytics?

AI reduces TCO by replacing manual document review, structuring unstructured claim data automatically, and surfacing insights that would otherwise require dedicated analyst time. The result is machine capacity substituting for labor cost at a fixed subscription price that doesn't scale with claim volume.