AI in insurance claims gets discussed frequently at the industry level, but the real value shows up in operational specifics: how fast a medical record gets reviewed, how reliably a coverage issue gets flagged, how many litigated files a team can actually work through in a given week. According to a 2024 Conning survey reported by Risk & Insurance, 77% of insurance C-suite decision-makers were in some stage of AI adoption — up from 61% just a year prior. The shift is accelerating.

This article covers what AI in claims actually does in practice, where it creates the most operational value for defense teams, and what's at stake for organizations still relying on manual processes.

Key Takeaways

- AI automates document review, claim intake, and pattern recognition — compressing multi-day tasks into minutes

- The two core gains are speed (faster resolution, less manual processing) and accuracy (fewer errors, better fraud detection, more consistent outcomes)

- Claims leakage — paying more than contractually owed — represents 7–14% of total carrier spend, according to EY; AI-driven accuracy directly addresses this

- Defense teams without AI face a widening competitive gap against plaintiff firms already using it

- AI delivers maximum value when applied consistently across the workflow, not selectively on a case-by-case basis

What Is AI in Insurance Claims?

AI in insurance claims applies machine learning, natural language processing, and predictive analytics to automate how claims documents are reviewed, prioritized, processed, and decided upon. It works across unstructured data — no perfectly formatted inputs required.

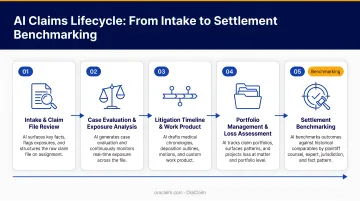

It's applied across the full claims lifecycle:

- First notice of loss and intake — classifying documents and extracting initial facts

- Coverage verification — identifying gaps, inconsistencies, and policy issues early

- Fraud detection — flagging anomalies, reused images, and inconsistent timelines

- Litigated claims review — analyzing demand packages, medical records, and expert reports

- Settlement benchmarking — comparing current claims against historical case outcomes

The practical framing: AI handles volume and pattern detection so professionals can focus on judgment, strategy, and outcomes. OraClaim, built by former litigators and claims professionals, treats this as the baseline — the platform amplifies experienced decision-making rather than attempting to replace it.

Speed: Faster Claims Resolution Through Automated Document Review

The Document Review Problem

Claims handlers on the defense side spend a disproportionate share of their time on low-value document work: reading reports, extracting facts, building summaries before any real analysis begins. Traditionally, non-billable manual document review consumes 40–70% of associate hours per matter. That's time not spent on strategy, negotiation, or the judgment work that actually moves claims toward resolution.

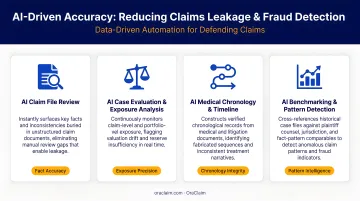

AI eliminates that bottleneck. It ingests unstructured documents — police reports, medical records, demand packages, recorded statements, expert reports — extracts critical facts, and surfaces relevant information in structured, actionable form. Work that previously took days gets done in minutes.

Document types AI handles: police reports · medical records · demand packages · recorded statements · expert reports

What This Looks Like in Practice

The McKinsey/Aviva case study is a well-documented benchmark: after deploying AI across its claims operations with more than 80 integrated models, Aviva reduced the average time to assess liability for complex cases by 23 days, improved claims routing accuracy by 30%, and cut customer complaints by 65%.

Those gains translate directly to the defense side. OraClaim reduces total claim file review time by half or more across first-party, third-party, and complex multi-party files. Medical chronology drafting — typically 15–60+ hours per file — drops to under 60 minutes for a first draft. Deposition outlines that once consumed 4–20 hours per witness are ready in minutes.

KPIs That Improve

- Average time to resolution

- Cost per claim

- Active cases per handler

- Billable-to-non-billable time ratio

When this matters most: High claim volumes, litigated claims with large document packages, and teams handling growing caseloads without proportional headcount growth.

Accuracy: Pattern Recognition and Benchmarking That Reduces Error and Leakage

What Accuracy Actually Means in Claims

Accuracy in claims means identifying coverage issues early, spotting fraud indicators before they become expensive problems, recognizing patterns across historical cases, and reaching decisions consistent with how similar claims were resolved before.

Manual review can't do this at scale. An adjuster working through hundreds of files can't reliably cross-reference each one against years of historical case data, catch subtle timeline inconsistencies, or benchmark every settlement value against comparable outcomes. AI handles all three simultaneously — and does it consistently across every claim in the queue.

The Leakage Problem

EY estimates that financial leakage represents 7–14% of carriers' total spend, with root causes including inaccurate damage evaluations, missed settlement opportunities, and ineffective litigation strategies. P&C insurers spend more than $23 billion annually on defense and cost containment. Leakage compounds those costs further.

AI-driven accuracy addresses leakage directly by:

- Cross-referencing incoming claims against historical case data to identify over- or under-reserving

- Flagging anomalies — reused photos, inconsistent treatment timelines, conflicting statements

- Benchmarking settlement values against comparable outcomes so decisions are defensible and consistent

- Surfacing recovery and subrogation opportunities that manual review misses

Benchmarking Across the Right Variables

OraClaim's automated benchmarking auto-tags each claim on dozens of dimensions — jurisdiction, venue, judge, plaintiff counsel, plaintiff expert, alleged injuries, treatment patterns, reserve range, and mediation outcomes — then produces comparisons against similar historical cases. This reduces manual benchmarking effort by 80%+ and brings consistent, data-supported decision-making to organizations that previously relied on gut feel or ad-hoc external searches.

KPIs That Improve

- Leakage rate — reduced through tighter reserving accuracy and early anomaly detection

- Fraud detection rate — improved by cross-referencing timelines, photos, and statements at intake

- Settlement value consistency — anchored to comparable outcomes rather than individual adjuster judgment

- Subrogation and recovery identification — surfaced systematically instead of caught only when spotted manually

Together, these gains compound: lower leakage, fewer fraudulent payouts, and more recovery dollars recaptured directly improve loss ratios at the portfolio level.

Scale: Handling Higher Volumes Without Proportional Headcount Growth

The Workforce Math Doesn't Work

Claim volumes are rising — driven by natural catastrophe losses ($115.6 billion in U.S. insured losses in 2024, per Triple-I), inflation, and social inflation that added an estimated $231.6–$281.2 billion in liability losses over the past decade. Meanwhile, the Bureau of Labor Statistics projects adjuster employment to decline 5% through 2034.

Deloitte reports that leading P&C insurers average 20% annual attrition, with each departure taking nearly six years of institutional experience out the door — and onboarding a replacement costing $8,000–$10,000 in the first year alone. Scaling with headcount is not a sustainable strategy.

How AI Bridges the Gap

AI automates the repeatable, time-consuming portions of claims handling — document review, initial triage, data extraction, chronology drafting — freeing the same team to handle more cases without sacrificing analytical quality. OraClaim is built specifically for this problem on the defense side. The platform:

- Cuts total claim file review time in half or more

- Reduces case evaluation from 10–40 billable hours to minutes for a first draft

- Generates medical chronologies, deposition outlines, and motion drafts in a fraction of manual time

- Enables profit margin improvements of up to 300% by converting non-billable hours into billable work

When document review no longer consumes 40–70% of associate time per matter, the same team carries a materially larger caseload — without adding a single hire.

KPIs That Move

Firms and carriers using AI to absorb volume typically see improvement across four core metrics:

- Cases handled per professional — more throughput from existing staff

- Overhead cost per case — less non-billable time per matter

- Capacity utilization — fewer bottlenecks during volume spikes

- Time-to-close — faster resolution across the portfolio

What Happens When AI Is Missing

The operational reality for teams still relying on manual processes is a set of compounding disadvantages:

- Inconsistent reserve decisions when two adjusters review the same claim and reach different conclusions — a variance problem that compounds across a portfolio

- Higher error rates on coverage determinations when reviewers are working through high volumes without structured support

- Slower resolution that keeps claims open longer and accumulates unnecessary exposure

- No pattern visibility — without structured historical data, there's nothing to benchmark against and no way to anticipate what a claim is worth

The competitive problem is specific to the defense ecosystem. Carrier Management reported in 2024 that plaintiff lawyers are adopting AI faster than defense attorneys — using it to assess case potential, conduct legal research, and prepare demand packages. Litigation finance firms are using predictive analytics to value cases before filing. Defense organizations navigating these claims with slower workflows and less data face a real structural disadvantage.

That gap is what pushed OraClaim's co-founders to build something different. Mark Tepper litigated claims for enterprise companies and insurers; Andy Anderson managed high-exposure claims for carriers. Both saw the same pattern from opposite sides of the same workflow: the defense side has financial resources but is losing ground because plaintiff firms are moving faster on technology.

Without AI support, the structural consequences are predictable: reactive firefighting instead of proactive strategy, partial audit coverage, and headcount as the only lever for scale. Every one of those conditions drives up loss adjustment expense and compresses defense margin.

How to Get the Most Value from AI in Claims

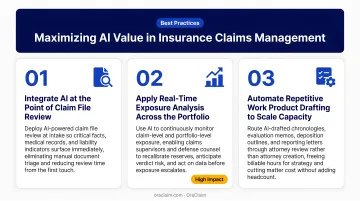

The highest-value AI implementations share three characteristics:

- Apply AI across the full workflow, not just selected cases — coverage across the entire process produces compounding value. Selective use limits pattern recognition and benchmarking accuracy.

- Track measurable outcomes from day one — teams that monitor KPIs (leakage rate, cost per claim, time to resolution, cases per handler) before and after implementation can see exactly where AI moves the needle and where gaps remain.

- Act on the outputs — AI insights deliver value only when they inform strategy, update reserve decisions, and refine benchmarks. Generated and ignored, they add nothing.

Choosing the Right Platform

Putting those characteristics into practice starts with selecting the right platform — and general-purpose AI handles claims documents poorly. Insurance claims involve unique document types (demand packages, IME reports, recorded statements), jurisdiction-specific regulatory contexts, and data structures that generic tools weren't designed for.

When evaluating platforms, defense teams should prioritize:

- Security architecture — encryption, authentication, closed-system design that preserves attorney-client privilege and work-product protection

- Integration with existing practice management and document management systems (Clio, iManage, NetDocuments, and similar)

- AI models trained specifically on claims defense data, not general legal or transactional work

OraClaim was purpose-built for this environment by former litigators and claims professionals who experienced these gaps firsthand. The platform serves defense lawyers, claims professionals, carriers, TPAs, and self-insured corporations through a closed, access-restricted architecture that keeps all Confidential Information subject to applicable privilege protections — and integrates with the practice management and document management systems defense teams already use.

Human Oversight Is Non-Negotiable

AI is most effective as a copilot. It surfaces information, flags patterns, accelerates review, and generates first drafts of work product. Decision-making authority belongs with the experienced professionals who understand context, jurisdiction, and strategy. EY has noted that over-reliance on case evaluation technology without critical thinking can actually increase avoidable litigation. AI augments professional judgment — it doesn't substitute for it.

Conclusion

AI in insurance claims delivers speed and accuracy as concrete operational outcomes — faster document review, more consistent decisions, higher case throughput, and better identification of recovery and defense opportunities. Those gains build on each other: benchmarking sharpens as more cases are processed, exposure estimates tighten as portfolio history deepens, and work product quality improves as the system trains on the firm's own patterns.

The claims organizations gaining durable advantage are those treating AI as an ongoing operational practice, not a pilot or an experiment. On the defense side, the urgency is real: plaintiff firms and litigation finance operations are already using technology to build informational advantages. Defense teams that close that gap now accumulate a structural edge — better-prepared files, sharper reserve decisions, and more consistent outcomes across the portfolio. The window to build that advantage is open now, not indefinitely.

Frequently Asked Questions

Do insurance companies use AI for claims?

Yes. The NAIC's 2023 AI Model Bulletin confirms that AI is used across the insurance lifecycle, including claim administration and fraud detection. A 2024 Conning survey found 65% of companies were piloting large language models specifically for claims.

How does AI improve accuracy in insurance claims?

AI cross-references incoming claims against historical case data to flag inconsistencies and fraud indicators that manual review misses at scale. It then benchmarks decisions against past outcomes, producing more consistent results across adjusters and handlers.

What types of insurance claims benefit most from AI?

High-volume routine claims benefit from automated triage and processing. Complex litigated claims benefit most from AI's ability to analyze large document sets, summarize demand packages, flag inconsistencies, and benchmark against historical outcomes — exactly the environment where manual review breaks down.

How does AI specifically help defense lawyers and claims professionals?

AI eliminates the non-billable document review burden that consumes 40–70% of associate hours per matter, surfaces critical facts faster, and enables teams to identify patterns across historical cases — producing stronger strategy, faster preparation, and more capacity without sacrificing quality.

What are the risks of using AI in insurance claims processing?

The primary risks are model bias from unrepresentative training data, data security requirements specific to legal and insurance contexts, and insufficient human oversight before AI outputs drive decisions. Over-reliance on automated evaluation without critical review can also increase avoidable litigation.

Is AI in claims management secure enough for sensitive legal and insurance data?

Organizations should verify industry-standard encryption, strong authentication, and a closed-system architecture that preserves attorney-client privilege and work-product protection. Any platform handling confidential claims data must also prohibit using that data for AI model training — a non-negotiable requirement in legal and insurance contexts.