Real-time rate exposure monitoring closes that gap. Instead of discovering reserve inadequacy after a verdict or a runaway settlement, defense teams and carriers get a continuous view of how claim severity, frequency, and reserve adequacy are shifting — while there's still time to act.

This guide covers exactly what you need to set it up, the three approaches that work in practice, how to read the signals you'll see, and where most teams go wrong.

Key Takeaways

- Tracks claim severity, frequency, and reserve adequacy before losses turn into verdicts, settlements, or reserve pressure

- Requires clean claims data, defined exposure baselines, and alerts that surface anomalies as files change

- Fits three monitoring models: manual dashboards, rule-based alerts, or AI pattern recognition for larger portfolios

- Depends on knowing portfolio-specific “normal” so real early warnings do not get dismissed as routine variance

- Helps teams reserve more accurately, intervene earlier, and avoid surprise losses that erode margins

What You Need to Monitor Rate Exposure in Real Time

Before a monitoring system produces useful output, three preconditions must exist: clean and structured data, defined exposure baselines, and clear ownership within the claims or legal team. Skip any one of these and monitoring generates noise rather than intelligence.

Data Sources and Inputs Required

The core inputs for meaningful rate exposure monitoring are:

- Claim reserves by line of business: current and historical values, not just aggregate totals

- Litigation stage milestones: complaint filed, discovery open, mediation scheduled, trial setting

- Historical resolution values: settlement amounts, verdict ranges, and dismissal rates by claim type and jurisdiction

- Current caseload composition: claim type mix, venue distribution, and plaintiff counsel concentration

The structural challenge most teams face before they even reach monitoring is data format. According to Accenture, nearly 80% of enterprise data is unstructured, including emails, text documents, legal reports, adjuster notes, and voice recordings. In the claims context, that includes PDF pleadings, demand packages, deposition transcripts, and medical records. None of that material is queryable in its raw form.

Converting unstructured documents into structured, analyzable data is a prerequisite for real-time monitoring, not a later enhancement. OraClaim, for example, ingests medical records, demand letters, prior pleadings, discovery responses, expert reports, and surveillance materials.

It then extracts and classifies key facts into structured fields that can support exposure analysis.

Preconditions and Organizational Setup

Two organizational steps matter before any monitoring system goes live:

Establish a baseline exposure profile. Benchmark historical claim values by type, jurisdiction, and litigation stage. Without this reference point, no deviation can be identified as meaningful. An uptick in reserves looks different when you know that claims of this type, in this venue, at this stage, historically settle in a specific range.

Assign ownership. Someone must be designated to review exposure signals, escalate anomalies, and update reserves. Monitoring without a review protocol produces data that sits unseen. The role can sit with an existing claims leader, as long as that person has a review schedule and clear escalation criteria.

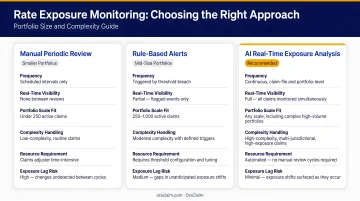

Three Approaches to Real-Time Rate Exposure Monitoring

No single approach fits every organization. The right choice depends on portfolio complexity, available technology, and team capacity. These three approaches span from low-tech manual review to fully automated AI-driven analysis.

Approach 1: Dashboard-Based Manual Monitoring

What it is: A centralized dashboard aggregates claim-level reserve data, open litigation count by stage, and pending settlement values. Reviewers log in on a defined cadence, daily or weekly, to spot deviations from baseline.

How to set it up:

- Build a claims data export or live feed into a reporting tool

- Define the KPIs to track: average reserve per claim, reserve-to-payment ratio, litigation rate by claim type

- Document the threshold at which a deviation triggers escalation

- Assign a named reviewer and a non-negotiable review schedule

Best for: Smaller portfolios or teams just beginning a monitoring program.

The honest trade-off: This approach works with tools you already have and requires no specialized technology. But it depends entirely on reviewer discipline and is blind to anything that happens between review sessions. A claim that spikes on Tuesday morning won't be visible until Friday's review.

Approach 2: Rule-Based Alerting Systems

What it is: Automated rules fire notifications when a claim crosses a defined threshold, such as a reserve exceeding a set dollar amount, an unexpected trial setting, or a jurisdiction-specific litigation rate spike.

How to set it up:

- Audit existing claims data fields to identify which variables most reliably precede exposure escalation

- Define rule logic using your portfolio's actual history rather than industry averages

- Configure notification routing to the appropriate claims handler or defense counsel

- Test rules against historical data before going live to verify that thresholds are calibrated correctly

Best for: Mid-size portfolios with relatively consistent claim profiles.

The honest trade-off: Rule-based systems remove human delay from the notification loop, so they are faster than manual review.

Two failure modes matter most: alert fatigue from miscalibrated thresholds, and missed patterns the team did not anticipate when writing the rules. If the rules do not account for a risk signal, the system will not catch it.

Approach 3: AI-Powered Pattern Recognition and Continuous Monitoring

What it is: AI platforms ingest claims data continuously, including structured fields and unstructured document content, then surface exposure signals that rule-based systems would miss.

Examples include:

- Claims clustering in a venue that historically produces outsized verdicts

- Subtle reserve drift across a claim type before a frequency spike

- Correlations no analyst would catch without reviewing thousands of files

How to set it up:

- Integrate the platform with existing practice management or document management systems

- Ingest and structure historical claim data to establish baseline patterns

- Configure alert sensitivity based on portfolio-specific risk tolerances

- Designate a team member to review flagged anomalies and close the feedback loop

Best for: Carriers or law firms managing high-volume or high-complexity dockets.

The honest trade-off: This is the most comprehensive approach, capable of surfacing non-obvious patterns across large portfolios without manual effort. It also requires initial data onboarding and a calibration period.

OraClaim fits this workflow when defense teams need claim-file and portfolio-level monitoring in one platform. It ingests medical records, demand packages, deposition transcripts, expert reports, surveillance materials, and prior pleadings, then runs continuous exposure analysis across the portfolio and each claim file.

When liability, damages, or reserve adequacy changes materially, alerts go to the assigned attorneys, adjusters, and claims managers.

How to Interpret Your Rate Exposure Data

The risk in real-time exposure data is misreading it. Treating normal claim lifecycle variance as a signal triggers unnecessary intervention; dismissing genuine early warnings as routine noise leads to exactly the outcomes monitoring is designed to prevent.

What Stable Exposure Looks Like

A healthy portfolio shows:

- Reserves tracking within a defined percentage band of historical averages for the same claim type and stage

- Litigation rates consistent with prior periods in the same jurisdiction

- Resolution values falling within expected ranges for the fact patterns involved

No intervention is required during stable periods. Document the period as within normal parameters, continue scheduled monitoring, and use the stability to refine your benchmarks. Stable periods are where good baseline data is built.

Warning Signals: Minor Deviations That Require Attention

Early warning signals rarely arrive as a single dramatic spike. They show up as:

- Reserve creep across multiple claims of the same type, each individually explainable but collectively trending upward

- An uptick in litigation rate in a specific jurisdiction without a corresponding change in claim volume

- Time-to-resolution lengthening beyond historical norms for a specific claim category

One of these signals may be routine. When two or three appear simultaneously in the same segment, that combination indicates emerging exposure pressure.

Actionable response: Flag the affected segment for increased monitoring frequency. Convene a brief review with the responsible claims handler or defense counsel to assess whether a reserve adjustment or strategy change is warranted before the pattern deepens.

Out-of-Spec: Critical Signals Requiring Immediate Response

Critical signals are unmistakable when you know your baselines:

- A sudden reserve spike on a large claim or cluster of claims

- A jurisdiction-specific litigation rate that departs dramatically from historical norms

- A settlement demand that arrives well above reserve, particularly when it follows a litigation milestone you didn't flag in advance

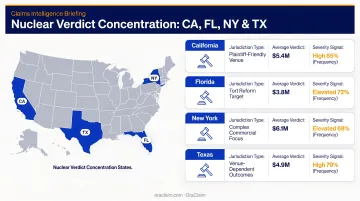

Venue concentration deserves special attention. The U.S. Chamber Institute for Legal Reform found that California, Florida, New York, and Texas accounted for half of all nuclear verdicts from 2013 through 2022, while product liability nuclear verdict median values rose 50%.

Delayed response to any of these compounds the problem. The further a claim travels down a path before a reserve is corrected or a strategy is adjusted, the more constrained the response options become.

Actionable response: Trigger an immediate reserve review and escalate to senior claims management or outside defense counsel. Evaluate whether to pursue early resolution or additional investigation before exposure grows further.

Common Mistakes in Rate Exposure Monitoring

The monitoring system is only as reliable as the decisions made around it. These are the errors that produce false confidence or missed signals.

Monitoring without baselines. Attempting to identify deviations without first establishing what "normal" looks like for a specific portfolio produces constant false alarms or complete blindness. Establish benchmarks before going live, and revisit them at least annually and after any significant portfolio composition change.

Siloing exposure data from legal strategy. Claims handlers and defense counsel often work in separate systems. Reserve signals stay hidden from attorneys making litigation decisions, and counsel insights may not reach claims leadership. OraClaim's portfolio management dashboards address this by rolling up real-time exposure by line of business, jurisdiction, plaintiff-counsel concentration, and reserve adequacy in one shared view.

Alert fatigue from miscalibrated thresholds. When rule-based or AI systems are too sensitive, reviewers start ignoring notifications. Threshold calibration is ongoing, not a one-time setup. Track your signal-to-intervention ratio: if most alerts do not result in action, adjust the thresholds.

Treating monitoring as passive. Teams should use every reviewed and resolved alert to update the system's baseline understanding of the portfolio. Groups that treat exposure monitoring as read-only lose the compounding accuracy improvements that make real-time systems more valuable over time. Close the feedback loop: the data relationship runs in both directions.

Conclusion

Real-time rate exposure monitoring changes how defense teams control claim exposure. Instead of waiting for end-of-cycle reports to show what already happened, teams use live signals to create options before they close.

The competitive advantage compounds over time. As baselines become more refined and signals become more precise, teams intervene earlier, reserve more accurately, and avoid the adverse verdicts and runaway settlements that erode margins. Defense teams and carriers that act on live exposure data are better positioned to protect margins than those still waiting for the quarterly report.

Frequently Asked Questions

What is rate exposure monitoring in the context of insurance claims defense?

Rate exposure monitoring tracks changes in claim severity, frequency, and reserves across a portfolio. Defense teams and carriers use it to spot emerging risk before it turns into larger losses.

How is real-time rate exposure monitoring different from a standard reserve review?

A reserve review is usually periodic and backward-looking, often quarterly or tied to case milestones. Real-time monitoring runs continuously, so teams can spot trends before they limit response options.

What data do you need to start monitoring rate exposure in real time?

Start with structured claims data: reserves, litigation stage, resolution values, claim type, and jurisdiction. You also need a historical baseline and a workflow that flags deviations on a regular basis.

How do you know when a rate exposure signal is a genuine warning versus normal variance?

A single metric moving outside its historical range is often normal variance. A signal becomes meaningful when multiple indicators move together or the deviation persists across several review periods.

Can smaller law firms or claims teams implement real-time rate exposure monitoring without dedicated analytics staff?

Yes. Smaller teams can start with dashboard monitoring, existing data exports, and defined review schedules. Set clear baselines and ownership first, then scale to rule-based or AI-driven monitoring as portfolio complexity grows.

How does AI improve rate exposure monitoring compared to manual or rule-based approaches?

AI can detect patterns across large datasets, such as links between claim type, jurisdiction, and outsized exposure. Unlike manual reviews or static rules, it runs continuously and does not depend on prewritten thresholds.