Introduction

Defense law firms and claims organizations operate under financial pressure that most other professional services businesses never face. Billing complexity is layered — outside counsel guidelines vary by carrier, invoice formats differ, and a single rejected line item can delay payment on an entire matter. Compliance scrutiny is constant. And insurance carriers increasingly expect demonstrable cost efficiency, not just competent defense.

Against that backdrop, financial management isn't an administrative function. It's a strategic one.

Integrated accounting and billing gets discussed as a software feature, but its real impact is operational — invoice cycle times, partner visibility into matter profitability, and how confidently a firm can walk into a bar audit.

This article explains why that integration matters in practice, what measurable advantages it creates for firms managing high volumes of matters, and what deferred action quietly erodes in realization rates and audit readiness over time.

Key Takeaways

- Integrated accounting and billing connects time tracking, invoicing, trust management, and financial reporting into one system, eliminating manual re-entry and the errors it causes.

- Clio's 2025 Legal Trends Report benchmarks average law firm realization at 88% — meaning 12% of billable work never reaches a client invoice.

- The average law firm lockup (unbilled WIP plus unpaid invoices) sits at 93 days — a cash flow problem that integration directly shortens.

- Trust account errors carry disciplinary consequences; California alone recorded 1,017 attorney trust-account overdraft cases in FY 2024.

- For defense firms managing large claim portfolios, disconnected billing and accounting systems create invisible margin erosion that compounds across every new matter.

What Is Integrated Accounting & Billing?

Integrated accounting and billing is a unified system where every billable activity flows automatically into accounting records, invoices, and financial reports — with no manual re-entry between separate tools. That includes:

- Tracked billable time logged by attorneys and staff

- Client expenses and disbursements recorded at the matter level

- Invoices generated directly from time and cost entries

Most law firms still don't operate this way. Time tracking, invoicing, and accounting run in separate platforms, which means the same data gets entered multiple times by multiple people. Every handoff between systems is a point where entries get missed or miscoded before anyone notices.

Integration removes those handoffs. Billing and accounting become a single connected workflow rather than parallel processes that need to be reconciled against each other at month-end.

The real goal is financial data that's accurate and current at every point in the billing cycle — not just after someone has spent days reconciling spreadsheets.

Key Advantages of Integrated Accounting & Billing

The advantages below are operational and measurable. Each maps directly to outcomes that law firm partners, billing managers, and claims professionals actually track: accuracy, speed, cash flow, compliance, and profitability.

Advantage 1: Eliminating Revenue Leakage and Billing Errors

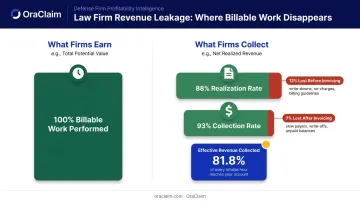

Revenue leakage is one of the most underrecognized profit drains in legal practice. According to Clio's 2025 benchmarks, the average law firm realization rate is 88% — meaning 12% of billable work doesn't make it onto a client invoice. On top of that, the average collection rate is 93%, meaning an additional 7% of what does get billed goes uncollected.

These aren't dramatic failures. They're steady, chronic losses that accumulate across hundreds of matters.

Integration stops leakage at the source. When time tracking connects directly to invoicing and accounting, billable work is captured at the point of activity and enters the invoice cycle automatically. No entry gets lost in the gap between a timekeeper's notes and the billing system.

Why this matters beyond the revenue number:

Billing errors don't just cost money — they generate disputes, trigger write-offs, and create correction work. According to a BigHand survey of 800 senior legal finance professionals, 59% of firms reported increased write-offs in the prior year, with 43% reporting increases of more than 10%. Another 60% expected write-offs to rise further in 2024.

The same research found that 47% of firms cited missing or late time entries and poor-quality timecards as a profitability factor — a process problem, not a personnel one.

KPIs this directly affects:

- Realization rate

- Write-off rate

- Billing turnaround time

- Accounts receivable aging

For defense firms billing across hundreds of simultaneous carrier matters, even a 2–3% realization improvement translates into material recovered revenue — with no additional headcount required.

Advantage 2: Real-Time Financial Visibility Across Matters and Portfolio

Integrated systems provide a single, live view of financial performance — by matter, by attorney, by carrier client, or across the entire portfolio. Finance staff don't need to compile reports manually from multiple disconnected sources. The data is current and queryable at any moment.

Without integration, the alternative is month-end reconciliation: a backward-looking process that tells partners how the firm performed, not how it's performing today.

BigHand's 2024 Annual Law Firm Finance Report found that 76% of law firm finance leaders face increased pressure for financial transparency and detailed reporting — a signal that financial visibility has become a management requirement, not a software preference.

What real-time visibility enables:

- Partners can identify underperforming matters early and adjust staffing or billing approach

- Carrier cost inquiries can be answered with data, not estimates

- Billing backlogs surface through WIP reporting before they become cash flow problems

- Portfolio-level profitability becomes visible — by matter type, by carrier, by practice area

The cash flow dimension is significant. Clio's 2025 report puts the average law firm lockup at 93 days — the combined lag of unbilled work-in-progress and unpaid invoices. Real-time visibility shortens the front end of that cycle by surfacing WIP earlier and giving billing staff the data they need to invoice on a regular cadence rather than waiting for month-end.

KPIs this directly affects:

- Profitability per matter

- Work-in-progress (WIP) value

- Collection rate

- Average days to payment

For defense firms and claims organizations managing large case portfolios, this is where integrated visibility has the most direct impact. The difference between a profitable and unprofitable portfolio is often buried in aggregated data that disconnected systems can't surface cleanly.

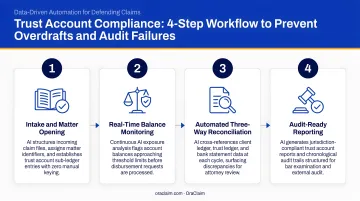

Advantage 3: Trust Account Compliance and Audit Readiness

Trust account management is one of the highest-stakes financial obligations law firms carry. Proper separation of client funds, accurate individual ledgers, and reconciled records aren't optional — they're a regulatory and ethical requirement. Non-compliance can result in disciplinary action, suspension, or disbarment.

The volume of violations makes this concrete. California's FY 2024 discipline report recorded 1,017 attorney trust-account overdraft cases, with 50 cases filed in State Bar Court and 45 resulting in discipline imposed. That's an ongoing compliance problem at significant scale.

How integration creates compliance by design:

Integrated systems enforce trust account rules structurally rather than relying on manual diligence:

- Prevent over-draws before they happen

- Automate three-way reconciliation workflows (bank statement, book balance, and individual client ledger)

- Maintain audit-ready transaction records on demand

- Eliminate the mispostings that occur when trust activity is tracked separately from billing and accounting

State bar rules in most jurisdictions require monthly reconciliation of trust records to the bank statement and quarterly reconciliation of individual client ledger balances. North Carolina's Rule 1.15-3 codifies exactly this structure.

Manual processes can satisfy these requirements — but consistent execution demands discipline, dedicated time, and zero tolerance for human error. Integration removes that dependency entirely.

KPIs this directly affects:

- Trust reconciliation frequency

- Compliance incident rate

- Audit preparation time

- Retainer management accuracy

Firms holding client retainers or managing settlement funds face the most exposure here. The risk compounds with matter volume — at scale, manual trust account management becomes difficult to execute without errors.

What Happens When Integration Is Missing

Disconnected billing and accounting systems don't announce their costs. The damage builds across several failure points:

Invoices go out with missing time entries or incorrect expense allocations. Write-offs increase. Realized revenue falls short of earned revenue — with no single clear moment of failure to catch.

Staff spend days at month-end matching entries across systems — time that produces no revenue and leaves the firm without accurate financial data for most of the billing period.

Trust accounts managed outside an integrated system are harder to reconcile and more likely to fall out of balance. Firms are less prepared for bar audits or carrier inquiries about fund management.

Manual processes that work at low matter volumes break down as the portfolio grows. Administrative costs increase faster than revenue, and the firm's operational model stops holding.

The Clio 2025 report puts a number on this overhead: the average worker spends 4 hours per week reorienting between software applications when operating across disconnected tools. For billing and accounting specifically, that switching cost shows up as delays, errors, and deferred invoices.

Getting the Most Value from Integrated Accounting & Billing

Integration delivers value only when used consistently. Time entries logged at the point of activity, trust transactions processed through the system, and invoices sent on a regular cycle are what turn software into a financial advantage. To get there, firms should:

- Review profitability reports by matter and attorney regularly — not just at year-end, but monthly at minimum

- Use WIP reports proactively to identify billing backlogs before they age into collection problems

- Monitor accounts receivable aging and follow up on overdue invoices on a defined schedule rather than reactively

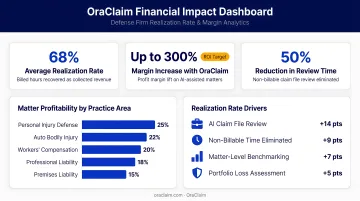

For defense law firms and claims organizations managing large, complex portfolios, platforms like OraClaim extend this financial visibility further. OraClaim's Financial Impact & Margin Analysis module connects operational claims and matter data to revenue, cost, profitability, and margin insights — surfacing metrics that standard billing software doesn't produce:

For Defense Firms

- Realization rate by matter and by partner

- Profitability by carrier client and matter type

- Write-down and write-off drivers

- Impact of AI tool adoption on billable-hour mix and margin

For Claims Organizations

- Defense cost as a percentage of indemnity

- Panel-firm cost benchmarking

- Reserve-vs.-paid trajectory by cohort

- Total cost of risk by line of business

This analytical layer sits alongside existing billing and accounting systems. It doesn't replace them. It adds the portfolio-level visibility that standard platforms can't produce: partner dashboards, carrier-client P&L, and CFO-ready margin reports. Managing partners and claims executives get a direct view of where margin is being made and where it's being lost.

Conclusion

Integrated accounting and billing strengthens a defense firm in three ways that build on each other: it tightens revenue capture, sharpens visibility into financial performance, and keeps compliance consistent across every matter. Each of these becomes more valuable as a firm grows.

None of these advantages arrive with implementation alone. They accumulate over time as billing data builds up, financial patterns emerge, and the firm develops the operational discipline to act on what the system surfaces.

Integration should be treated as an ongoing operational standard, not a one-time technology choice. For defense firms managing high claim volumes under carrier scrutiny, it's one of the most reliable paths to improving profitability without adding headcount.

Firms that establish this foundation early are the ones best positioned to scale — without their administrative costs outpacing revenue growth.

Frequently Asked Questions

. I'll flag this in

<analysis>

<blog_topic>Integrated Accounting & Billing for Law Firms: Why It Matters</blog_topic>

<section_heading>Frequently Asked Questions</section_heading>

<section_type>FAQ</section_type>

<company_name>OraClaim</company_name>

<target_region>US</target_region>

<target_audience>Defense Lawyers, Claims Professionals, Insurance Carriers, Law Firms, Claims Organizations</target_audience>

<inferred_tone>Professional but Approachable</inferred_tone>

</analysis>

<issues_found>

**CRITICAL ISSUES** (2 found):

**Issue #1** [CRITICAL]

- **Category**: FAQ Answer Length Violation

- **Problematic Text**: "Integration enforces compliance structurally — preventing trust account over-draws, automating three-way reconciliation, and maintaining audit-ready records at all times. This removes the reliance on manual processes where errors are harder to catch before they become bar complaints or disciplinary matters."

- **Problem**: This answer is 3 lines, which is at the hard limit. On rendering, the em-dash construction and clause density push this to feel like a wall. However, more importantly, the phrasing "This removes the reliance on manual processes where errors are harder to catch before they become bar complaints or disciplinary matters" is an awkward passive construction burying the key insight at the end. The answer technically passes the line count but violates the directness requirement and uses a punchline em-dash (banned AI pattern).

- **Fix**: Remove em-dash, restructure for directness, keep to 2-3 lines.

**Issue #2** [CRITICAL]

- **Category**: AI Pattern — Punchline Em-Dash (Banned Structural Tic)

- **Problematic Text**: "Integration enforces compliance structurally — preventing trust account over-draws..." and "Each of these compounds quietly — there's rarely a single visible failure point, just chronic margin erosion."

- **Problem**: Two instances of the punchline em-dash pattern in a single section. Per criteria, maximum 1 em-dash per section, and the "punchline em-dash" pattern (building to a dramatic payoff after the dash) is explicitly banned.

- **Fix**: Replace both with restructured phrasing using commas or colons, or split into two sentences.

**IMPORTANT ISSUES** (3 found):

**Issue #3** [IMPORTANT]

- **Category**: AI Pattern — Banned Phrase / Structural Tic

- **Problematic Text**: "Each of these compounds quietly — there's rarely a single visible failure point, just chronic margin erosion."

- **Problem**: "quietly" followed by a punchline em-dash is a textbook AI writing pattern ("quietly revolutionized," "quietly became" — the "quiet" modifier used for dramatic effect). Also contains the punchline em-dash (second instance). The phrase "chronic margin erosion" is also vague promotional-style language.

- **Fix**: Rewrite to be direct and concrete without the theatrical structure.

**Issue #4** [IMPORTANT]

- **Category**: Content Relevance / Company Alignment Mismatch

- **Problematic Text**: The entire FAQ section references trust account management, bar complaints, three-way reconciliation, WIP aging, accounts receivable aging, and trust account ledgers — none of which are OraClaim's product capabilities. OraClaim is an AI claims defense platform, not billing/accounting software.

- **Problem**: This section appears written for a different company's blog entirely. The content does not connect to OraClaim's core offerings (AI claim file review, case evaluation, work product drafting, exposure analysis) and references explicit out-of-scope functions (general legal billing/accounting infrastructure). This is a topic/company alignment issue that cannot be fully resolved with surgical edits — it requires a content strategy decision.

- **Fix**: Flag for human review. As a surgical edit, I will improve the quality of the writing as-is while noting this concern. Full realignment to OraClaim's actual product would require a full rewrite of the FAQ questions and answers.

**Issue #5** [IMPORTANT]

- **Category**: FAQ Answer Verbosity — Borderline Length

- **Problematic Text**: "Core reports include profitability by matter or attorney, work-in-progress (WIP) aging, accounts receivable aging, trust account ledgers, and three-way reconciliation reports. More sophisticated platforms add carrier-client P&L, write-off analysis, and matter-level profitability benchmarks."

- **Problem**: The second sentence ("More sophisticated platforms add...") is vague and comparative without naming which platforms. "More sophisticated platforms" is a hedged, non-committal phrase that weakens the answer. The answer is functional but could be tightened.

- **Fix**: Replace "More sophisticated platforms add" with a more direct construction.

**MINOR ISSUES** (2 found):

**Issue #6** [MINOR]

- **Category**: Hedged Authority / Qualifier

- **Problematic Text**: "The data advantage also compounds as the firm grows, making early adoption more valuable than waiting until matter volume forces the issue."

- **Problem**: "forces the issue" is a slightly informal idiom that doesn't fit the professional tone of the rest of the section. Minor but inconsistent.

- **Fix**: Replace with cleaner phrasing: "until matter volume demands it."

**Issue #7** [MINOR]

- **Category**: Content Alignment Flag (Company Topic Mismatch — for human review)

- **Problematic Text**: Full FAQ section

- **Problem**: The blog topic "Integrated Accounting & Billing for Law Firms" does not align with OraClaim's product (AI claims defense platform). OraClaim explicitly lists "Policy administration, first notice of loss (FNOL) intake, premium billing, claims payment processing" as out of scope. Billing and accounting software for law firms is also out of scope per the company's defined ICP (insurance defense workflow tools, not practice management billing software). This content may be intended as a thought-leadership/informational piece rather than a product page, but the disconnect is notable. Flag for editorial review on strategic intent.

- **Fix**: Human review required to determine if topic realignment is needed. Surgical fixes applied to writing quality only.

</issues_found>

<revised_content>

### What is integrated billing and accounting in legal practice software?

It's a unified system where time tracking, invoicing, trust management, and general ledger accounting operate within a connected platform. Billable activity flows automatically into financial records without manual re-entry between separate tools, eliminating the data gaps that cause billing errors and reconciliation delays.

### How does integrated billing and accounting reduce compliance risk for law firms?

Integration enforces compliance structurally: it prevents trust account over-draws, automates three-way reconciliation, and maintains audit-ready records at all times. Manual processes leave errors undetected until they escalate into bar complaints or disciplinary matters — a unified system closes that gap.

### What are the risks of running separate billing and accounting systems at a law firm?

The main risks are unbilled time, billing errors requiring correction, delayed reconciliation, and trust account discrepancies that grow harder to detect as matter volume increases. None of these announce themselves as single failures. They accumulate in the background, steadily eroding margins until the damage is difficult to reverse.

### How does integrated accounting and billing improve cash flow for law firms?

Integration shortens the billing cycle: time enters the invoice automatically, invoices go out faster, and payment status is visible in real time. This reduces the gap between work performed and payment received — directly addressing the 93-day average lockup most law firms currently carry.

### What financial reports should law firms expect from an integrated billing and accounting system?

Core reports include profitability by matter or attorney, work-in-progress (WIP) aging, accounts receivable aging, trust account ledgers, and three-way reconciliation reports. Advanced platforms extend this further with carrier-client P&L, write-off analysis, and matter-level profitability benchmarks.

### Is integrated billing and accounting worth the investment for smaller law firms?

Yes. The cost of disconnected systems — unbilled time, reconciliation labor, and compliance risk — typically exceeds the cost of a unified solution. The data advantage also compounds as the firm grows, making early adoption more valuable than waiting until matter volume demands it.