Introduction

Mid-size MGAs are caught in a genuine operational squeeze. Large enough to attract significant claims volume, but not large enough to absorb it through headcount or enterprise infrastructure — they occupy a position where growth creates pressure faster than capacity can respond.

The numbers make this concrete. According to AM Best, U.S. MGAs produced $89.9 billion in premium in 2024, up 15% year over year — the fourth consecutive year of double-digit growth. Claims volume scales with premium. Teams that were adequately staffed two years ago are now underwater.

The answer isn't simply hiring. This guide walks through a practical approach to building efficient claims volume management from the ground up:

- What to audit first before adding tools or staff

- How to triage and automate for maximum throughput

- Which variables drive — or kill — efficiency at scale

- Where most mid-size MGAs go wrong

The right structure and tools make the difference between a team that's drowning and one that absorbs growth without sacrificing defense quality.

Key Takeaways

- Claims volume growth has outpaced mid-size MGA staffing — headcount alone won't solve this

- Efficient operations start with a baseline workflow audit, then progress to triage, automation, and real-time reporting

- The variables that determine efficiency at scale: claims complexity, staffing ratios, data quality, and carrier reporting obligations

- Treating all claims equally is the single most damaging operational mistake at mid-size MGAs

- AI-powered tools purpose-built for claims professionals can cut claim file review time in half, letting teams handle more volume without adding headcount

Why Claims Volume Becomes a Breaking Point for Mid-Size MGAs

Mid-size MGAs occupy a distinct operational position. Too large to rely on informal person-to-person claims handling, too small to deploy the carrier-grade systems large insurers run. The result: volume grows faster than the infrastructure built to manage it.

Three pressure points converge at mid-size scale:

- Volume outpacing workflows — submission and claims volume grows, but intake processes, assignment logic, and tracking systems don't scale automatically with it

- Carrier scrutiny of delegated authority — AM Best's performance assessment framework explicitly reviews claims-related operations, staffing, data quality, and use of automation as conditions of maintaining delegated authority; poor claims handling performance has strategic consequences

- Technology asymmetry with plaintiff firms — defendants and insurers risk falling behind the plaintiffs' bar in AI adoption, with plaintiff firms expected to move faster on case assessment, research, and demand packages; defense-side teams relying on manual processes face a structural disadvantage

Survey data confirms how widely these pressures register. Gallagher Bassett's 2025 MGA Market Pulse found:

- 58.1% of MGAs outsource at least some claims management — a sign that internal capacity is already stretched

- 40% identify claims and underwriting technical expertise as a major operational challenge

- 22.9% cite legacy IT systems as a primary hindrance to efficiency

Managing claims volume efficiently is a data and structure problem, not a headcount problem. Unstructured claims data, inconsistent documentation, and siloed workflows create compounding inefficiencies that worsen as volume scales. Adding adjuster hours treats the symptom; fixing the underlying architecture treats the cause.

What Mid-Size MGAs Need Before Scaling Claims Operations

Scaling without preparation amplifies existing problems rather than resolving them. Three foundations need to be in place before adding tools or headcount.

Operational Baseline and Documentation

Document the current claims workflow end-to-end: how claims are received, categorized, assigned, tracked, and reported to carriers. This documentation becomes the foundation for every improvement that follows.

Common gaps to identify include:

- Reliance on email chains for claim communication

- Spreadsheets standing in for a real tracking system

- Disconnected systems with no shared data layer

Deploying automation on top of an undocumented workflow guarantees chaotic results. Map the process first.

Data Readiness and System Integration

Claims data must be accessible, structured, and connected across core systems: the claims management platform, document storage, and carrier reporting tools. If data lives in silos or unstructured formats, automation cannot function effectively.

Before committing to any new tools or platforms, assess:

- Where data currently lives and in what format

- Which systems need to share data but currently don't

- What integration points exist or can be built

Carrier Authority and Compliance Requirements

MGAs operating under delegated underwriting authority have specific reporting and compliance obligations. Before scaling, confirm:

- Which claims thresholds require carrier notification or approval

- What bordereaux and reporting formats are required

- Whether current workflows can generate that output reliably at higher volume

Compliance obligations scale with volume. An MGA that struggles to hit reporting requirements at 500 claims per month will face compounding problems at 1,500.

How to Manage Claims Volume Efficiently: A Step-by-Step Approach

Step 1: Audit and Triage Claims by Complexity and Risk

Not all claims warrant the same attention or the same workflow. The first operational step is categorizing the existing and incoming claims portfolio by complexity — separating simple, fast-close claims from those involving litigation exposure, multiple parties, or high reserve potential.

Without triage, adjusters apply the same effort to a minor property claim as to a contested liability matter. That's unsustainable at scale.

An effective triage system uses rule-based routing criteria to automatically direct claims to the appropriate workflow track:

| Triage Dimension | Low Complexity Track | High Complexity Track |

|---|---|---|

| Reserve threshold | Below defined limit | Above defined limit |

| Litigation flag | No attorney involvement | Attorney represented |

| Claim type | Single-party, clear liability | Multi-party, contested liability |

| Line of business | Routine property | Commercial GL, professional liability |

Even a basic triage matrix — built before any automation tool is deployed — dramatically improves throughput. High-complexity claims get the right attention; routine claims close faster.

Step 2: Standardize Claims Intake and FNOL Processing

Inconsistent First Notice of Loss intake is one of the most common sources of downstream delay and data quality problems. When different adjusters collect different information at intake, every subsequent step slows down.

NCCI research on workers' compensation claims found that reporting delays carry real cost consequences: claims costs rose 35% in Week 3 relative to Week 2, and attorney involvement increased from 13% for immediately-reported claims to 32% for claims reported after Week 4. The principle applies beyond workers' comp — late, incomplete intake creates downstream costs.

Standardized intake requires:

- Consistent FNOL forms or intake templates across all channels (email, portal, phone)

- Automatic validation for missing required fields before a claim proceeds

- Multi-channel capture that doesn't create parallel, inconsistent data streams

Every claim should enter the workflow with the same structured information, enabling faster assignment and eliminating the back-and-forth that kills cycle time.

Step 3: Automate Document Review and Claims Data Structuring

Document review is the most time-intensive and least scalable task in claims management. As volume grows, the burden of reading, extracting, and organizing information from medical records, police reports, loss documentation, and legal correspondence grows proportionally — unless it's automated.

AI-powered document processing tools extract critical facts, surface relevant case details, and deliver structured summaries that allow adjusters and defense professionals to act immediately rather than spending hours in manual review. For claims that escalate to defense and litigation, this is the difference between preparation and reaction.

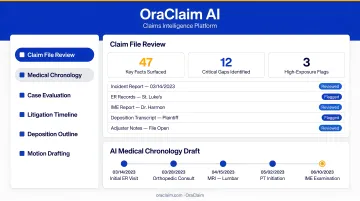

OraClaim is built specifically for this phase. The platform automatically ingests and classifies medical records, police and incident reports, witness statements, expert reports, prior pleadings, demand packages, and correspondence. From that intake, it delivers:

- Structured fact extraction — key dates, injuries, and events organized without manual data entry

- AI-surfaced contradictions, treatment inconsistencies, and liability flags

- Structured summaries and fact-extraction reports that accelerate reserve decisions and defense strategy

For mid-size MGAs, the impact on volume is direct. OraClaim cuts claim file review time in half or more across first-party, third-party, and complex multi-party files. Medical chronology drafting — which typically requires 15–60+ hours per file using paralegals or legal nurse consultants — is reduced to under 60 minutes for a first draft. Teams handle significantly more cases without adding headcount.

Step 4: Connect Operational Data to Performance Reporting

Efficient claims volume management requires real-time visibility into how the operation is performing — not just quarterly reviews.

Core metrics a mid-size MGA should be tracking:

- Average claim cycle time by line of business

- Cost per claim and cost per closed claim

- Reserve adequacy relative to ultimate paid losses

- Litigation rate by LOB and by plaintiff counsel

- Adjuster caseload relative to throughput and closure ratios

These metrics serve a dual purpose: they help the internal team identify bottlenecks early, and they satisfy carrier reporting expectations around portfolio health and delegated authority performance.

In practice, connecting operational data to reporting means integrating claims platform data with a real-time dashboard — enabling managers to spot volume spikes or deteriorating cycle times while they're still manageable. OraClaim's portfolio management view consolidates open and closed claims, reserves, paid and incurred losses, defense costs, and exposure analytics in one place. Drill-down to individual files is available alongside outside-counsel alignment tools that reduce reporting back-and-forth and speed up authority decisions. When managers have this visibility in real time, they stop responding to problems after the fact and start addressing them before they compound.

Key Variables That Determine Claims Efficiency at Scale

Even with the right process structure, several operational variables determine whether efficiency holds as volume grows — or breaks down.

Claims Complexity and Line of Business Mix

Efficiency benchmarks vary significantly by line of business. Workers' compensation average temporary disability duration runs 94 days (median 54 days), per NCCI data. Commercial auto liability posted a 76.8% loss ratio and 12.7% LAE in 2023. General liability and professional lines carry longer tails and higher litigation rates.

As MGAs expand their product mix, claims teams must recalibrate resource allocation by LOB — not apply a single operational standard across all lines. If the portfolio shifts toward more litigation-exposed commercial lines, the same staffing structure produces worse outcomes.

Tracking reserve-to-paid ratios and litigation rates by LOB helps flag when the mix is shifting before it creates a capacity crisis.

Adjuster Caseload and Bandwidth

There is a caseload threshold beyond which adjuster quality and decision speed decline. A 2019 workers' compensation benchmarking study by Rising Medical Solutions found that 53% of frontline staff had indemnity caseloads of 125 or fewer, and organizations in that range generally achieved more favorable closure ratios.

That benchmark is workers' comp specific, but the principle holds across lines: uncapped caseloads produce worse outcomes.

Adjuster bandwidth must be monitored actively — not assumed stable. When volume spikes, triage criteria should automatically shift, routing more routine claims to accelerated or automated tracks to protect adjuster capacity for complex matters.

Data Quality and System Integration

Data quality is a multiplier. Good data accelerates every downstream step — triage, routing, document review, reporting. Poor data creates friction at every stage.

In practical terms, data quality means:

- Complete, consistent FNOL fields on every claim

- Structured rather than free-text documentation

- Clean integration between claims, policy, and reporting systems

- Consistent claimant and policy identifiers across platforms

This is foundational. Automation cannot compensate for structurally poor data — it surfaces those problems faster and at greater scale.

Carrier Reporting and Compliance Burden

Bordereaux reporting, compliance submissions, and carrier-mandated data formats consume significant operational time — time that competes directly with claims handling capacity. As volume grows, manual compliance reporting becomes a serious drag on efficiency. Two factors make this worth prioritizing:

- Automation potential is high: Report generation tied directly to the claims platform can eliminate most manual compilation work

- Impact is immediate: Unlike staffing or system overhauls, automated reporting reduces LAE from day one

It's the most overlooked efficiency lever in most MGA operations — and one of the fastest to implement.

Common Mistakes Mid-Size MGAs Make When Managing Claims Volume

Four operational mistakes account for the majority of avoidable volume problems at mid-size MGAs:

No triage system. Without priority-based routing, adjusters work in arrival order. High-exposure claims get delayed while low-complexity claims consume disproportionate time — the most common and most damaging pattern at volume.

Scaling headcount before fixing process. Hiring additional adjusters into a broken workflow scales the inefficiency. New staff inherit the same bottlenecks and data quality problems. Process comes first; headcount decisions should follow from a clear view of what automation cannot handle.

Waiting until the team is already overwhelmed. Many mid-size MGAs defer technology investment until a backlog is visible. By then, team morale is under pressure and carrier relationships may already be strained. Earlier adoption — when volume feels manageable — creates headroom to absorb future growth without disruption.

Treating litigation preparation as a manual task. For claims that escalate to defense, the preparation phase — reviewing records, organizing documents, surfacing key facts — is where significant time and cost accumulates. Plaintiff firms have automated this work; defense-side teams that haven't fall behind at volume. Investing in litigation-readiness tools matters as much as investing in intake and triage.

Each of these mistakes compounds the others. Fixing triage without addressing preparation workflows, or adopting tools without repairing the underlying process, produces partial gains at best.

Frequently Asked Questions

What is an appropriate claims-to-adjuster ratio for a mid-size MGA?

Ratios vary by line of business, complexity, and litigation rate — there's no single standard. Workers' comp data suggests indemnity caseloads should stay at or below 125 per adjuster, but that benchmark doesn't translate to GL or commercial auto. Tracking caseload relative to cycle time and closure ratios is more useful than any fixed number.

How can mid-size MGAs handle claims volume spikes without hiring?

Triage automation routes routine claims to faster tracks, freeing adjuster capacity for complex matters. AI-assisted document review reduces time per complex claim substantially. Dynamic caseload rebalancing — shifting routing thresholds during spikes — absorbs volume without triggering immediate headcount additions.

How does claims handling performance affect an MGA's carrier relationships?

Carriers monitor MGA loss ratios, cycle times, and claims handling quality as conditions of delegated authority. Poor performance can result in reduced capacity, increased oversight, or partnership termination. Operational efficiency is a strategic priority — not just an internal one.

What's the difference between using a TPA and managing claims in-house for a mid-size MGA?

TPAs offer scale and specialization, but at the cost of direct control over claims data and carrier relationships. In-house management preserves that control — it just requires investment in systems and staff. Many mid-size MGAs split the difference with a hybrid model, routing complex or high-volume claim types to TPAs while managing others internally.

At what point should a mid-size MGA invest in AI-powered claims tools?

Before the operation is overwhelmed. The right trigger is when volume is growing steadily and manual processes are beginning to create delays or inconsistencies — not after a backlog has formed. Waiting for a crisis increases the cost and disruption of adoption, and risks damaging carrier and customer relationships in the process.