Introduction

Defense teams and claims professionals are under pressure from two directions at once. Claim volumes are climbing. Meanwhile, plaintiff firms are moving faster than ever — using technology to build stronger cases, identify high-value targets, and push for larger settlements before defense teams have finished their initial file review.

Analysts at Carrier Management warn that plaintiff lawyers will likely adopt AI faster than defense attorneys and insurers because the incentive structures simply differ. That asymmetry compounds every week it goes unaddressed.

Predictive analytics and AI-powered claims analysis are the practical response. This is working infrastructure — tools that help defense-side teams triage faster, detect litigation risk earlier, set more accurate reserves, and make better strategic decisions when it counts.

This article explains what predictive analytics means in the claims context, why it changes the economics of defense work, how the underlying process works step by step, and how platforms like OraClaim are putting these capabilities directly into defense teams' hands.

Key Takeaways

- Predictive analytics uses AI and historical claims data to forecast outcomes — including severity, litigation probability, and settlement ranges — before a claim develops.

- Defense teams gain early identification of high-risk claims, enabling strategic intervention at FNOL rather than months later.

- AI structures unstructured claims data and surfaces patterns that manual review consistently misses at scale.

- More accurate reserves, stronger defense strategies, faster resolutions, and better margins — all without growing the team.

What Is Predictive Analytics in Insurance Claims?

Predictive analytics in claims management means using AI and machine learning models — trained on historical claims data — to forecast future outcomes. That includes claim severity, litigation probability, fraud likelihood, and expected settlement ranges. Rather than tracking what a claim has done, it tells you what a claim is likely to do.

This is a meaningful shift from traditional claims management software, which records and organizes information reactively. Traditional systems tell you what happened. Predictive analytics gives you a forward-looking view from the moment a claim is filed.

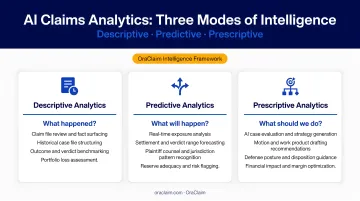

In practice, AI-powered claims analysis operates across three modes:

- Descriptive — organizes and structures what has already happened in a claim

- Predictive — forecasts likely outcomes based on comparable historical patterns

- Prescriptive — recommends specific actions based on those forecasts

Modern platforms increasingly combine all three, moving from raw data ingestion through to specific strategy recommendations in a single workflow. For defense teams, the classification matters in practice: descriptive-only analytics leaves exposure forecasting and strategic guidance entirely off the table.

The infrastructure supporting all three modes is already in broad deployment. LexisNexis Risk Solutions reported that virtual claims handling jumped from less than 15% of the market before COVID-19 to over 60% by early 2021, with 55% of consumers citing faster settlement as a direct result. The infrastructure for data-driven claims workflows exists. The question is who deploys it most effectively.

Why Predictive Analytics Changes the Economics of Defense Claims

The Core Problem: Volume Without Structure

Claims professionals are managing growing portfolios where the majority of intelligence lives in unstructured documents — medical records, attorney correspondence, incident reports, deposition transcripts. Industry sources estimate 80% of insurance data exists in everyday correspondence, not in structured fields. Manual review can't apply uniform rigor across every file at that scale.

Sedgwick alone handles over 8 million claims annually. That volume makes prioritization a survival skill, not a preference.

Triage and Severity Scoring

Predictive models score incoming claims by projected severity and complexity from the point of first notice of loss. Instead of every claim entering a generic queue, claims are immediately sorted: which files need senior adjuster attention, which need litigation counsel engaged now, and which can follow a streamlined workflow.

McKinsey reported that claims-domain AI deployments have produced a 30% improvement in routing accuracy and a 23-day reduction in complex liability assessment time. That's the difference between catching a developing exposure early and discovering it at mediation.

Litigation Risk Detection

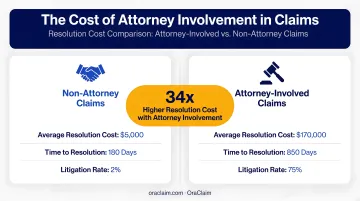

Attorney-involved claims cost dramatically more. Claims Journal, citing Sedgwick and Milliman data, reported that commercial auto claims with an attorney cost 34 times more on average to resolve than claims without one. That single statistic reframes litigation-risk detection as one of the highest-value functions a claims AI can perform.

Predictive models flag early signals of litigation potential: attorney involvement patterns, jurisdiction trends, claim characteristics that correlate with escalation. Defense teams get time to intervene — proactively engaging litigation counsel, adjusting reserves, or pursuing early resolution before the cost curve bends upward.

Reserve Accuracy

U.S. P&C insurers added $16 billion to reserves in 2024 after underestimating past liability claims, according to Swiss Re. Reserve inaccuracy isn't a rounding error — it's a material financial risk.

AI-driven outcome prediction addresses this by comparing a new claim against thousands of structurally similar resolved cases, generating data-backed value ranges rather than individual adjuster estimates. OraClaim's automated benchmarking module auto-tags each claim across dozens of dimensions to identify true comparables and surface defensible reserve recommendations:

- Case type, jurisdiction, and judge

- Plaintiff counsel and alleged injuries

- Treatment patterns and policy limits

Fraud Signal Identification

Insurance fraud costs at least $308.6 billion annually and occurs in roughly 10% of property-casualty losses, according to the Coalition Against Insurance Fraud. AI models flag anomalies that manual review at high volume routinely misses: inconsistencies in claim timing, provider patterns, conflicting statements, and documentation gaps.

OraClaim's claim file review specifically surfaces contradictions, timeline gaps, treatment inconsistencies, and unverified details before they become reserve surprises or trial-day discoveries. These flags appear early, when intervention still changes outcomes.

How AI-Powered Claims Analysis Works: Step by Step

This isn't a theoretical framework. It reflects how AI operates in real claims environments to move from raw data to actionable defense strategy.

Step 1 — Ingest and Structure Claims Data

AI begins by ingesting everything available on a claim: intake forms, medical records, accident reports, attorney correspondence, litigation history, prior claim files. It structures all of this into a usable format regardless of how disorganized the source documents are.

OraClaim handles the full range of document types:

- ER reports, hospital records, specialist notes, and imaging reports

- Police and incident reports, witness statements, and demand packages

- Prior pleadings, expert reports, and attorney correspondence

The system automatically classifies every document, extracts key facts, and produces chronological summaries with normalized provider names, dates, diagnoses, treatments, and outcomes.

The critical mistake many teams make: feeding AI only clean or structured data. The majority of claims intelligence lives in unstructured documents. That's where the value is — and where manual review consistently falls short.

Step 2 — Triage and Severity Scoring

The AI assigns a risk and severity score to each incoming claim based on comparable historical cases, enabling immediate prioritization across an entire portfolio. Complex claims route to senior adjusters or litigation counsel faster. Low-complexity claims move through streamlined workflows without consuming senior capacity unnecessarily.

OraClaim's exposure analysis surfaces exposure drivers at this stage : causation strength, medical specials trajectory, comparative fault evidence, lien exposure, and punitive damages risk. Adjusters get a substantive picture of a claim's potential from day one.

Step 3 — Pattern Recognition and Risk Signal Detection

Machine learning models identify patterns across a claim's characteristics that correlate with known high-cost outcomes. Claims that appear routine at FNOL but share characteristics with historically escalating cases get flagged early — before the trajectory becomes apparent through normal progression.

OraClaim's automated benchmarking auto-tags each claim across dozens of dimensions, then surfaces closest comparables from historical closed-case data. The more historical data the system has access to, the more precise the risk signals become. That precision directly narrows reserve uncertainty and reduces late-stage surprises.

Step 4 — Outcome and Litigation Probability Prediction

The AI generates probabilistic forecasts: estimated claim value ranges, litigation likelihood, projected settlement windows, and anticipated legal cost exposure — all tied to comparable case outcomes.

OraClaim produces full case evaluations that cover:

- Liability assessment and comparative fault analysis

- Damages exposure and special damages calculations

- Reserve recommendations and settlement value ranges

- Trial value ranges and jury verdict comparables

These outputs directly inform defense strategy: whether to settle early, assign litigation counsel proactively, or escalate for closer reserve management.

Step 5 — Strategy Refinement and Continuous Learning

As each claim resolves, outcome data feeds back into the model, refining the benchmarks used for future comparisons. Historical case file structuring converts years of closed files (PDFs, scanned records, email archives) into structured institutional knowledge that improves every subsequent prediction.

Teams that skip this loop let their analytics stagnate. As claim patterns evolve : jurisdiction trends shift, plaintiff firm tactics change, medical cost inflation accelerates. A system without a feedback cycle loses accuracy over time. One that learns from every resolved claim gets sharper on reserve ranges, settlement timing, and litigation risk with each case that closes.

Predictive Analytics in Action: A Claims Walkthrough

Consider a moderate-severity auto liability claim that lands in a claims manager's queue. Soft tissue injury, no prior claims history, minimal documentation at FNOL. On the surface, it looks routine — a candidate for standard processing.

Manual review would likely treat it as such. But the AI flags it differently.

The platform compares this claim against historical cases with the same attorney representation pattern in the same jurisdiction. Those comparables show an elevated litigation rate and settlement value well above what the initial presentation suggests. The system issues an escalation alert within days of FNOL — not months later when the claim has already developed its own momentum.

Acting on that early signal, the defense team moves quickly:

- Engages litigation counsel proactively, before the claim gains momentum

- Sets reserves at a more defensible level based on comparable outcomes

- Pursues early resolution, avoiding the cost spike the claim's trajectory suggested

The exposure that looked manageable on day one stays manageable.

What this illustrates: predictive analytics doesn't replace experienced judgment. It gives experienced professionals better information earlier, at the point when that information actually changes the outcome.

How OraClaim Brings Predictive Analytics to Defense Teams

OraClaim is a claims intelligence platform built specifically for the defense side of the docket — not a general-purpose insurance tool, and not plaintiff intake software. Co-founders Mark Tepper and Andy Anderson both came out of the defense ecosystem: Mark litigating claims and managing risk for enterprise companies and insurers, Andy analyzing risk for insurers and managing high-exposure claims. They built OraClaim because they lived the problem firsthand — overwhelming claim volumes, manual processes, unstructured data, and a plaintiff bar gaining technological advantages faster than defense teams could respond.

The platform's AI automatically structures and benchmarks past cases to identify patterns, anticipate outcomes, and refine strategies — while eliminating the non-billable document review that drains defense team capacity. It delivers litigation-ready work product across the full defense workflow:

- Claim file reviews and key fact surfacing

- Case evaluations and medical chronologies (15–60+ hours reduced to under 60 minutes)

- Deposition outlines (4–20 hours per witness reduced to minutes)

- Motion drafts and custom work product trained on firm style

OraClaim also connects operational claims data with revenue and cost insights, giving defense organizations visibility into efficiency, margin, and portfolio health.

Claims VPs and managing partners can see total cost of risk by line of business, panel-firm cost benchmarks, reserve adequacy by cohort, and matter-level profitability. The focus is on how the entire claims operation performs, not just individual claim decisions.

The platform operates as a closed, access-restricted system designed to preserve attorney-client privilege and attorney work-product protection, with encryption, role-based authentication, and data protection protocols throughout.

Frequently Asked Questions

What is predictive analytics in insurance claims?

Predictive analytics in claims uses AI and machine learning models trained on historical claims data to forecast outcomes — including severity, litigation risk, and settlement ranges. Defense teams get actionable outcome projections from the moment a claim is filed, not just a record of what has already occurred.

How does AI help with claims triage and prioritization?

AI scores incoming claims for risk and severity at FNOL, enabling claims managers to immediately identify which cases need senior resources versus streamlined handling. McKinsey has reported a 30% improvement in routing accuracy from claims-domain AI deployments — without requiring manual review of every file.

Can predictive analytics identify litigation risk before a claim escalates?

Yes. AI flags early signals including attorney involvement patterns, jurisdiction trends, and claim characteristics that correlate with high-cost outcomes. Given that attorney-involved commercial auto claims have been reported to cost 34 times more on average to resolve, early detection allows defense teams to intervene before costs compound and settlement leverage shifts.

What data does AI use to analyze insurance claims?

Both structured data (claim forms, reserve history, policy data) and unstructured data (medical records, attorney correspondence, incident reports) are used. Processing unstructured sources is where AI delivers its clearest edge: roughly 80% of claims intelligence lives in documents, not structured fields.

How does predictive analytics help set more accurate claim reserves?

AI compares a new claim against thousands of structurally similar resolved cases to generate an outcome range, replacing individual adjuster estimation with data-driven benchmarking. This reduces both over-reserving and under-reserving — a meaningful safeguard given that U.S. P&C insurers added $16 billion in reserve additions in 2024 alone.

How is AI-powered claims analysis different from traditional claims management software?

Traditional claims software records and tracks what has happened. Predictive AI forecasts what is likely to happen and recommends what to do next. For defense teams, that difference means entering negotiations, mediations, and depositions with data-backed exposure estimates rather than best guesses.