Introduction

Defense teams are drowning in volume. A single claims professional can carry dozens to hundreds of open files simultaneously — and every day spent manually reviewing documents is a day where a quietly escalating claim goes unnoticed.

The stakes are real. U.S. commercial casualty insurance losses reached $143 billion in 2023, and commercial auto liability claim severity rose 93.5% from 2015 to 2024 — more than double the rate of general inflation. In that environment, misclassifying a single high-exposure claim doesn't just sting. It can produce reserve shortfalls, adverse verdicts, and margin erosion across an entire portfolio.

AI claims triage and severity scoring is the automated process of evaluating incoming claims against learned criteria to determine complexity, potential cost, and the appropriate handling pathway. This guide covers how it works, what drives severity scores, where defense teams most commonly get it wrong, and why the technology has become a operational necessity for any defense team managing meaningful claim volume.

Key Takeaways

- AI triage evaluates structured and unstructured claim data simultaneously at intake — no manual sorting required

- Severity scoring assigns each claim a tier (low/medium/high) so the right resources reach the right claims immediately

- Triage is continuous — models rescore claims as new information (attorney involvement, surgery referrals, depositions) enters the file

- "Jumper claims" that appear routine at FNOL but escalate undetected are the core threat AI triage is designed to catch

- Historical case benchmarking lets defense teams anticipate outcomes instead of estimating blind

What Is AI Claims Triage and Severity Scoring?

AI claims triage is the automated process of evaluating incoming claims against learned criteria to determine complexity, potential cost, and appropriate handling pathway. It replaces or augments the manual judgment a claims professional would otherwise apply at first notice of loss (FNOL).

Severity scoring is the specific output of that process: a numerical score or categorical tier (low, medium, high) assigned to each claim based on signals in the file, which then guides routing decisions, reserve setting, and intervention priority.

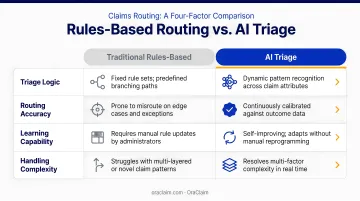

How It Differs from Rules-Based Routing

Traditional claims routing applies fixed logic: if injury type = fracture, route to senior adjuster. This works for obvious cases but misses the combinations that drive cost.

AI-based triage learns from thousands of resolved claims and detects subtle signal combinations that no ruleset would anticipate — a soft-tissue claim with a specific treatment pattern and prior claim history, for example, that historically resolves at three times the expected cost.

Side by side, the gap is significant:

| Traditional Rules-Based | AI Triage |

|---|---|

| Fixed criteria, manually updated | Learns from historical outcomes |

| Evaluates claims once at FNOL | Rescores continuously as file evolves |

| Misses signal combinations | Detects multi-factor patterns |

| Cannot read unstructured text | NLP extracts meaning from notes, records, correspondence |

Why Defense Teams Need AI Claims Triage

The Volume and Asymmetry Problem

Managing a large claims portfolio manually is unsustainable. With commercial auto liability loss and defense cost containment ratios reaching approximately 86% in 2024 — the highest in five years — the margin for inefficiency is gone.

The harder problem is competitive asymmetry. Generative AI use in the legal sector nearly doubled from 14% in 2024 to 26% in 2025, and 45% of law firm respondents either used it or planned to make it central to their workflow within a year. Plaintiff firms have been among the fastest adopters, using AI to evaluate claim value and litigation trajectory before defense teams have finished their initial review.

This is precisely what OraClaim's founders, Mark Tepper and Andy Anderson, observed through years of litigating and managing high-exposure claims. Despite the defense side having financial resources, plaintiff lawyers were leveraging technology faster, creating an information gap that directly affected settlement leverage. That observation drove the platform's design.

The Jumper Claim Problem

The most expensive claims aren't always the ones that look expensive at FNOL. A slip-and-fall. A soft-tissue auto claim. A minor premises incident. These files enter the queue looking manageable, then accumulate:

- Attorney representation

- MRI and surgical referrals

- Psychological injury claims

- Prior claim history that surfaces late

- Jurisdictional venue risk that wasn't flagged

By the time the complexity is visible, cost-containment windows close. The IRC found that fraud and buildup added $5.6B to $7.7B in excess auto injury payments in a single year, much of it embedded in claims that didn't initially appear problematic.

Without continuous AI rescoring, these cases slip through until intervention is no longer practical.

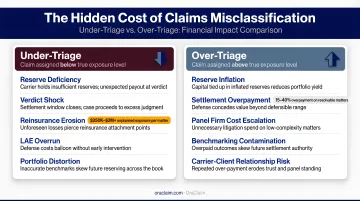

The Cost of Misclassification

Getting severity wrong in either direction is expensive:

- Under-triage: High-exposure claims don't get early intervention, reserves fall short, and outcomes deteriorate

- Over-triage: Senior specialists spend time on routine files, capacity is wasted, and margins erode

Both errors compound over a portfolio. McKinsey has estimated that claims transformation can reduce loss adjustment expenses by 25% to 30% and reduce total claims costs by 6% to 7%. Accurate triage is the mechanism that makes that reduction possible.

How AI Claims Triage and Severity Scoring Works

At a high level: a claim enters the system at FNOL, all available data is ingested, the AI evaluates it against learned patterns, assigns a severity score with supporting rationale, routes the claim, and then continues rescoring as the file evolves.

Step 1: Claim Intake and Data Extraction

At FNOL, the AI ingests everything — structured fields (claim type, date of loss, jurisdiction, policy limits, reported injury) and unstructured documents (medical records, adjuster notes, demand packages, incident reports, prior pleadings, correspondence).

NLP is what makes the unstructured side possible. Rather than requiring a human to read and summarize each document, NLP extracts facts, classifies document types, surfaces key dates and injuries, and flags contradictions automatically.

OraClaim's platform, for example, classifies every document, extracts every fact, and produces citation-linked fact summaries and anomaly reports as outputs. It integrates directly with practice management systems like Clio, iManage, and NetDocuments to eliminate manual file transfers.

Step 2: Severity Scoring

The AI model evaluates extracted data against patterns learned from resolved historical claims. It does not apply a single rule: it identifies combinations of signals that historically predicted high cost, prolonged litigation, or early resolution, then generates a score that reflects those patterns.

High-scoring claims are immediately flagged for intervention. Low-scoring claims move toward expedited or straight-through processing.

Score interpretability matters. A severity score is only useful if the claims professional understands why the claim scored high. Effective systems surface the reasoning: "High score driven by attorney involvement + MRI referral + prior claim history."

OraClaim's exposure analysis surfaces specific drivers, not just a number:

- Causation strength and comparative fault evidence

- Medical specials trajectory and lien exposure

- Prior claim history and attorney representation status

- Punitive damages risk indicators

Step 3: Routing, Action, and Continuous Rescoring

The claim routes to the appropriate resource with an accompanying rationale. Senior specialist, standard adjuster, or automated resolution — the routing decision has documented justification.

This isn't a one-time event. As new documents enter the file — deposition transcripts, surgery referrals, attorney representation notices, expert reports — the AI automatically re-runs its analysis and issues exposure-change alerts to assigned attorneys, adjusters, and claims managers. Reserve adjustments happen before they become surprises.

Key Signals That Shape Severity Scores

Injury and Loss Severity Indicators

AI triage models detect injury signals in medical records and adjuster notes that human reviewers might not flag at FNOL:

- Surgical procedures (especially spinal, orthopedic, or neurological)

- Chronic pain diagnoses and long-term disability claims

- Psychological injury overlays (PTSD, anxiety, depression)

- Treatment escalation patterns — gaps followed by sudden intensity

- Pre-existing condition documentation inconsistencies

- Causation gaps between the loss event and reported injuries

OraClaim's medical chronology module specifically flags treatment gaps, prior accidents, comorbidities, missed appointments, and inconsistencies between subjective complaints and objective findings — all of which affect both causation arguments and damages exposure.

Legal and Litigation Signals

Attorney representation is one of the strongest severity predictors in defense claims. A WCRI study of nearly one million workers' compensation claims found that attorney involvement increased indemnity payments by $7,700 to $12,400, increased lost-time days by 284%, and inflated expense payments by 200%.

Beyond representation itself, AI models trained on defense portfolios detect early linguistic indicators — specific phrasing in claim narratives, unusual documentation requests — that often precede formal attorney involvement.

Jurisdictional venue risk is equally significant. The U.S. Chamber Institute for Legal Reform analyzed 1,288 nuclear verdicts from 2013 to 2022, finding a $21.1 million median and $88.9 million mean award. California and Florida each produced nearly 200 nuclear verdicts in that period. OraClaim's automated benchmarking tags every claim by jurisdiction, venue, and judge, enabling defense teams to calibrate reserves and strategy based on venue-specific outcome history.

Claim Characteristics and Historical Benchmarking

Additional signals that drive severity escalation:

- Reporting delays and timeline inconsistencies

- Prior claim history for the same claimant

- Contradictions between reported damages and documentation

- Unusual claim patterns relative to the loss event

Historical benchmarking adds the deepest layer of context. OraClaim automatically tags each claim across dozens of dimensions — case type, jurisdiction, venue, judge, plaintiff counsel, plaintiff expert, alleged injuries, and treatment patterns — then benchmarks it against the organization's historical closed cases.

Outputs include similar-case settlement and verdict ranges, plaintiff-counsel-specific outcome histories, and judge-specific motion-grant rates. Reserve-setting shifts from gut-level estimation to decisions grounded in closed-case data.

Common Misconceptions and When to Proceed with Caution

Misconception: Triage Is a One-Time FNOL Decision

The most damaging claims are precisely those that look clean at intake. Effective AI triage rescores claims continuously — daily, as new information enters the file — turning triage from a snapshot into a live process. Teams that configure triage only at FNOL and never revisit it are solving half the problem.

Misconception: AI Replaces Experienced Adjusters and Attorneys

AI triage is a decision-support tool. Complex commercial liability claims, large-loss negotiations, and litigation strategy still require human expertise. What AI does is clear the volume — handling pattern detection, routing, and continuous monitoring — so that experienced professionals concentrate on cases that genuinely need them.

OraClaim's work product is always produced as a first draft for attorney review, never as final legal advice. The attorney reviews, revises, and finalizes every output before it leaves the firm.

Misconception: Severity Scores Are a Black Box

Well-designed AI triage systems provide clear rationale for every score. Defense teams should treat unexplained scores as a disqualifying red flag when evaluating any AI triage tool. The NAIC's Model Bulletin on AI Systems, adopted in December 2023, specifically identifies lack of transparency as an AI risk and calls for governance frameworks that include validation and auditability.

When to Proceed with Caution

AI triage performs poorly when underlying data is fragmented, siloed, or inconsistent. Deloitte has noted that insurer data is often siloed by function, system, and platform, and that legacy system incompatibility hinders scaling data for value.

Two situations call for extra scrutiny before deploying AI triage:

- Fragmented or legacy data: Prioritize data standardization first. OraClaim's Historical Case File Structuring module ingests unstructured PDFs, scanned files, and email archives, converting them into structured, searchable institutional knowledge for organizations with fragmented records.

- Highly novel claim types: Newly emerging mass tort categories may require human-led evaluation until enough resolved-case data exists for the model to learn from.

Frequently Asked Questions

What is the difference between AI claims triage and traditional manual triage?

Manual triage relies on a claims professional's judgment based on limited FNOL information, applied once. AI triage continuously evaluates all structured and unstructured claim data against patterns learned from thousands of resolved cases, rescoring claims as new information enters the file rather than treating intake as a final determination.

How does AI assign a severity score to a claim?

The model identifies signals across the full claim file — including injury type, attorney involvement, documentation patterns, jurisdictional factors, and treatment trajectories. These signals are compared against outcomes from historically similar claims to generate a score reflecting predicted cost and complexity.

Can AI triage tools read unstructured data like adjuster notes and medical records?

Yes. Natural language processing (NLP) enables AI triage systems to extract meaningful signals from free-text documents, including adjuster narratives, medical records, and attorney correspondence — content that rules-based systems cannot parse at all.

What types of claims are best suited for AI triage?

High-volume, standardized claim types — auto liability, general liability, workers' compensation — benefit most from AI triage. Highly novel or legally complex claims still require human-led evaluation, supported by AI-generated insights rather than AI-generated decisions.

Does AI triage replace claims adjusters or defense attorneys?

No. AI triage handles volume, pattern detection, and routing so that adjusters and attorneys concentrate their expertise on complex, high-exposure claims that genuinely require human judgment. All AI-generated outputs serve as starting points for professional review.

How do defense teams measure whether AI claims triage is working?

Key indicators include fewer unexpected claim escalations, improved reserve accuracy, faster time-to-intervention on high-severity claims, and shorter overall cycle times. Carriers and TPAs that have deployed AI triage consistently report measurable gains in both routing accuracy and claims resolution speed.

Conclusion

AI claims triage and severity scoring transforms a manual, intermittent, subjective process into one that is continuous, objective, and data-driven. Defense teams that implement it accurately stop reactive case management before it erodes outcomes — allocating the right resources at the right time, intervening early on high-exposure claims, and maintaining reserve accuracy throughout the claim lifecycle.

The real value is focus: experienced defense professionals applying their judgment to claims that actually need it, with complete information in hand, before the intervention window closes. Plaintiff firms adopted AI-assisted case evaluation early. OraClaim was purpose-built for the defense side — giving claims professionals and defense counsel the triage intelligence, exposure analysis, and benchmarking to match that advantage and defend every claim more effectively.