Introduction

Insurance exposure sits at the center of every coverage decision, every reserve calculation, and every claims outcome. Yet many defense lawyers and claims professionals treat it as an underwriting concept — something actuaries worry about, not litigators.

That framing is costly. Without a structured framework for reading exposure signals across a portfolio, defense teams react to high-value claims instead of anticipating them.

Plaintiff firms have recognized this gap. As OraClaim's co-founders Mark Tepper and Andy Anderson observed firsthand while litigating and managing risk on the defense side, plaintiff lawyers are adopting technology faster, and the information asymmetry that creates is already showing up in case outcomes.

Closing that gap starts with understanding the fundamentals. This guide breaks down what insurance exposure actually means, how it's measured and priced, and how defense teams can turn exposure analysis into a proactive strategic tool.

Key Takeaways

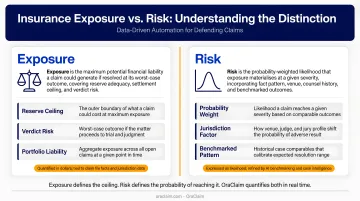

- Exposure = vulnerability to financial loss; risk = probability that loss materializes. The two are related but not interchangeable.

- Four loss exposure types: personal, property, liability, and net income — each demands a different defense approach

- Inaccurate exposure data at underwriting creates flawed baselines for reserves, settlements, and coverage disputes

- Analyze exposure at the portfolio level to anticipate litigation trajectory — not just react to escalating claims

What Is Insurance Exposure and Why Does It Matter?

Exposure vs. Risk: A Critical Distinction

The NAIC defines exposure as "the risk of possible loss" — but operationally, exposure and risk function as two separate concepts that demand separate treatment.

Exposure is the quantified vulnerability of an asset, operation, or individual to potential financial loss. It exists regardless of probability. A commercial warehouse has fire exposure simply because it contains physical assets and ignition sources. Risk is the probability that exposure produces an actual loss — shaped by construction type, suppression systems, occupancy, and operating practices.

Conflating the two creates compounding problems:

- Clients end up underinsured because exposure wasn't quantified at adequate limits

- Reserves get set based on probability assumptions, not actual loss potential

- Claims resources get misprioritized toward likelihood rather than magnitude

Munich Re reported in 2023 that underinsurance can leave policyholders receiving only a fraction of actual repair or replacement costs — a direct consequence of exposure being measured at inception against outdated or inaccurate valuations.

Why Defense Teams Need This Framework

Insurance contracts are structured around exposure. Every major contract element — limits, deductibles, exclusions, and reinsurance arrangements — is calibrated to exposures identified at policy inception. When exposure is misjudged at underwriting, that error carries through every claims decision made on that file.

Claims professionals who understand how exposure was originally assessed can identify problems before they become expensive:

- Coverage disputes surface where original exposure was misclassified or underquantified

- Reserve inadequacy emerges when limits were set against inaccurate valuations

- Claims misprioritization follows when severity potential wasn't mapped at file opening

The 4 Types of Loss Exposures Explained

Personal Loss Exposure

Covers mortality, disability, and loss of earning capacity for individuals. Defense relevance: workers' compensation, personal injury, and life/disability claims. Key assessment factors include age, occupation, health history, and dependency relationships — all of which directly affect damages calculations in litigation.

Property Loss Exposure

Covers direct and indirect losses to physical assets:

- Direct losses — immediate physical damage valued at replacement or repair cost (fire, flood, theft)

- Indirect losses — business interruption, extra expense, and lost rents; often the larger financial exposure in commercial claims and a persistent source of coverage disputes

Liability Loss Exposure

The most litigation-intensive category for defense teams. Covers legal responsibility for bodily injury, property damage, or personal injury caused to third parties.

Swiss Re reported in 2024 that U.S. liability claims increased 57% over the prior decade, with 27 court cases in 2023 producing awards above $100M. A separate analysis by Triple-I and CAS found that legal system abuse contributed $231.6B to $281.2B in increased liability insurance losses from 2014 to 2024.

Exposure assessment for liability must account for:

- Contract obligations and applicable industry regulations

- Jurisdiction — venue can materially shift verdict exposure

- Historical claim patterns in comparable operations

Net Income Loss Exposure

Financial losses from either reduced revenue or increased expenses following an insured event. Frequently underestimated at policy inception, which leads directly to reserve challenges during claims handling. Business interruption and contingent business interruption claims are the primary defense battleground here.

Pure Risk vs. Speculative Risk

Cutting across all four exposure types is a distinction that routinely surfaces in coverage disputes: pure risk involves only two outcomes — loss or no loss — and is generally insurable. Speculative risk involves three outcomes — loss, gain, or break-even — and is generally not insurable. When coverage applicability is disputed, this distinction often determines whether the policy was designed to respond at all.

How Exposure Is Measured and Priced

The Exposure Basis

Every policy type uses a specific metric — the exposure basis — to quantify exposure. According to IRMI, an exposure base is "a variable used to measure the extent of risk," with examples including payroll, receipts, sales, square footage, and man-hours.

The CAS identifies three criteria for a sound exposure basis: it should accurately measure exposure to loss, be easy for the insurer to determine, and be difficult for the insured to manipulate.

Common exposure bases by line of business:

- General liability — revenue, payroll, or square footage

- Workers' compensation — payroll or employee count

- Commercial property — building value, square footage, or construction type

- Commercial auto — vehicle count or car-months

- Cyber — revenue, IT security controls, or data volume

From Exposure to Premium

Once exposure is measured, pricing follows a consistent formula. The CAS Basic Ratemaking framework is direct: claim frequency (claims per exposure unit) multiplied by claim severity (average loss dollars per claim) produces the pure loss cost, which is the foundation of the premium before risk, expense, and profit loads are added.

When exposure data is inaccurate at underwriting, every downstream calculation is built on a flawed baseline. Common sources of error include:

- Wrong building classification or construction type

- Understated payroll or employee headcount

- Outdated revenue figures that no longer reflect operations

For the defense side, that means reserves and settlement valuations are anchored to numbers that don't reflect actual exposure.

Exposure Analysis in Claims: Surfacing Risk Patterns Across the Portfolio

The Limits of Single-File Review

Defense teams handling high claim volumes cannot identify systemic exposure patterns by reviewing files one at a time. The patterns that predict severity — specific plaintiff counsel, particular jurisdictions, recurring injury profiles — only become visible at portfolio scale.

Claims costs represent approximately 80% of an insurer's total costs, according to McKinsey, which also estimates that optimizing claims processes can reduce loss adjustment expenses by 25–30% and indemnity spend by 3–5 percentage points. The lever is data — but most of the data that matters is unstructured.

The Unstructured Data Problem

Meaningful exposure analysis requires inputs across multiple dimensions:

- FNOL data and policy/coverage terms

- Adjuster notes and reserve history

- Settlement and payment history

- Litigation timelines and motion practice outcomes

- Medical records, deposition summaries, and expert reports

Adjuster narrative notes, medical records, and deposition transcripts often contain the most critical exposure signals. They're also the hardest to process at scale.

Datos Insights noted in 2023 that repetitive manual extraction and classification of data from insurance documents remains standard practice across the industry. That bottleneck directly limits how quickly defense teams can identify emerging exposure patterns.

Reducing Claims Leakage Through Benchmarking

Claims leakage occurs when settlements exceed what exposure analysis would support — driven by inconsistent valuation of similar claims, missed subrogation opportunities, or inadequate reserves. Structured exposure benchmarking reduces leakage by surfacing outliers against a defensible historical baseline.

OraClaim's automated benchmarking module addresses this directly: the platform auto-tags each claim across dozens of dimensions — jurisdiction, plaintiff counsel, injury type, treatment pattern, reserve history, motion outcomes — and benchmarks every new claim against comparable closed files. The system surfaces settlement and verdict ranges for similar fact patterns, flags under-reserved and over-reserved cohorts, and reduces manual benchmarking effort by 80% or more — replacing informal valuations and disconnected spreadsheet comparisons with a defensible, data-driven baseline.

Key outputs from the benchmarking module include:

- Settlement and verdict ranges for comparable fact patterns

- Identification of under-reserved and over-reserved claim cohorts

- Reserve adequacy alerts triggered by new document intake

- Plaintiff counsel and jurisdiction performance benchmarks

Exposure Pattern Recognition and Fraud Detection

The same portfolio-level data that drives benchmarking also functions as an early fraud detection mechanism. The Coalition Against Insurance Fraud estimates that fraud occurs in approximately 10% of property-casualty losses and costs American consumers at least $308.6B annually.

Repeated claim incidents, unusual timing patterns, and inconsistencies between reported facts and historical exposure data for similar risks are early indicators of inflated or fraudulent claims. When defense teams can benchmark incoming claims against historical data at scale, these anomalies surface systematically rather than by chance.

OraClaim's AI processes unstructured claim file materials — medical records, recorded statements, prior pleadings, deposition transcripts, expert reports — and automatically surfaces contradictions, treatment inconsistencies, causation gaps, and unverified details. The platform re-runs exposure analysis each time new documents enter the file and issues alerts to assigned attorneys, adjusters, and claims managers when material changes occur.

Managing Exposure Aggregation and Building a Defense-Ready Strategy

What Aggregation Risk Looks Like in Practice

Swiss Re defines accumulation risk as "the potential loss exposure of one event spreading to multiple lines of business in an insurer's portfolio." For defense teams, this is the scenario where a single catastrophic event — a product recall, a natural disaster, a workplace incident pattern — generates correlated claim volume that overwhelms standard capacity.

Swiss Re sigma 1/2025 reported global insured natural-catastrophe losses of $137B in 2024. Swiss Re's April 2025 U.S. P&C outlook flagged reserve adequacy as a key unknown for future profitability, with downside risk specifically from underestimating past liability claims. Aggregation is a material, present-tense risk.

Monitoring Aggregation Across the Portfolio

Defense teams need visibility into where exposure is concentrating:

- Track exposure concentration by claim type, jurisdiction, and coverage line

- Flag when a single loss event is generating multiple related claims

- Stress-test reserves against correlated loss scenarios, not just individual file estimates

OraClaim's portfolio management module provides dashboards that roll up real-time exposure by line of business, jurisdiction, plaintiff-counsel concentration, reserve adequacy, and claim aging — flagging outlier cohorts before they become reserve shortfalls.

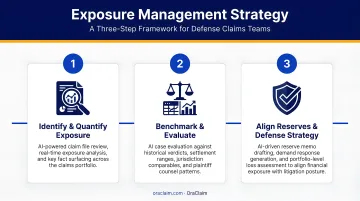

Three Practical Steps to Strengthen Exposure Management

- Establish a consistent exposure classification system across all incoming claims — without a shared taxonomy, portfolio-level analysis produces noise instead of signal

- Benchmark new claims against historical comparables with similar exposure profiles to set realistic, defensible reserve ranges before litigation pressure distorts valuation

- Review high-concentration exposure areas on a set cadence, not only when a major claim arrives — teams that wait for escalation lose the preparation window

When a cluster of claims shares common characteristics — same defendant, overlapping coverage, similar fact patterns — defense teams can coordinate discovery, align strategy across files, and enter negotiations with a clearer picture of total exposure. That coordination is only possible when the data is organized before the pressure arrives.

Frequently Asked Questions

What are the 4 types of loss exposures?

Personal, property, liability, and net income. Personal covers mortality and disability; property covers physical asset damage and indirect losses like business interruption; liability covers legal responsibility to third parties; net income covers financial losses from revenue reduction or increased expenses after an insured event. Each type shapes damages calculations, reserve requirements, and coverage dispute risks differently — distinctions that matter at every stage of claims defense.

What is the 80% rule in insurance?

The coinsurance provision requires that property be insured to at least 80% of its replacement cost value for the insurer to pay claims in full. Coverage below that threshold results in proportional loss payment: recovery equals the loss multiplied by the ratio of insurance purchased to insurance required. This is a recurring dispute in commercial property claims defense, especially where property values have risen since the policy was written.

What are the 3 D's of insurance claims?

Deny, Delay, and Defend: the three primary insurer responses to a claim. Deny contests coverage or liability outright; Delay postpones resolution pending investigation; Defend accepts the claim's validity but contests damages or fights it in litigation. Recognizing which response is in play helps defense teams anticipate where friction with carrier instructions is most likely to surface.

What is the difference between exposure and risk in insurance?

Exposure is the vulnerability or potential for loss — what could go wrong and how much it could cost. Risk is the probability that loss will actually occur. A building has fire exposure by virtue of existing; the risk depends on construction, suppression systems, and occupancy. Both must be assessed separately to price coverage accurately and set appropriate reserves.

How is exposure used to calculate insurance premiums?

Insurers follow a three-step process to build a premium from exposure data:

- Divide historical claim counts by exposure units to calculate claim frequency

- Multiply frequency by average claim severity to produce a pure loss cost

- Add risk, expense, and profit loads to arrive at the final premium

When the exposure basis is inaccurate — understated payroll, wrong building class, outdated revenue — the pure loss cost is wrong from the start, and every number downstream reflects that error.

How does claims data analysis improve exposure management for defense teams?

Portfolio-level claims analysis gives defense teams several concrete advantages:

- Benchmarks current exposure against historical comparables

- Identifies patterns that predict high-severity outcomes before they escalate

- Surfaces settlement outliers that signal reserve leakage

- Coordinates strategy across related claims with shared exposure characteristics

That shift from reactive file-by-file review to proactive portfolio analysis is where claims data stops being an administrative record and starts driving defense strategy.